AlpInvest's Atom Splits the Difference: Inside the $7 Billion Bet on Single Companies

Carlyle AlpInvest just closed its second dedicated single-asset continuation vehicle fund at a $1.7 billion hard cap.

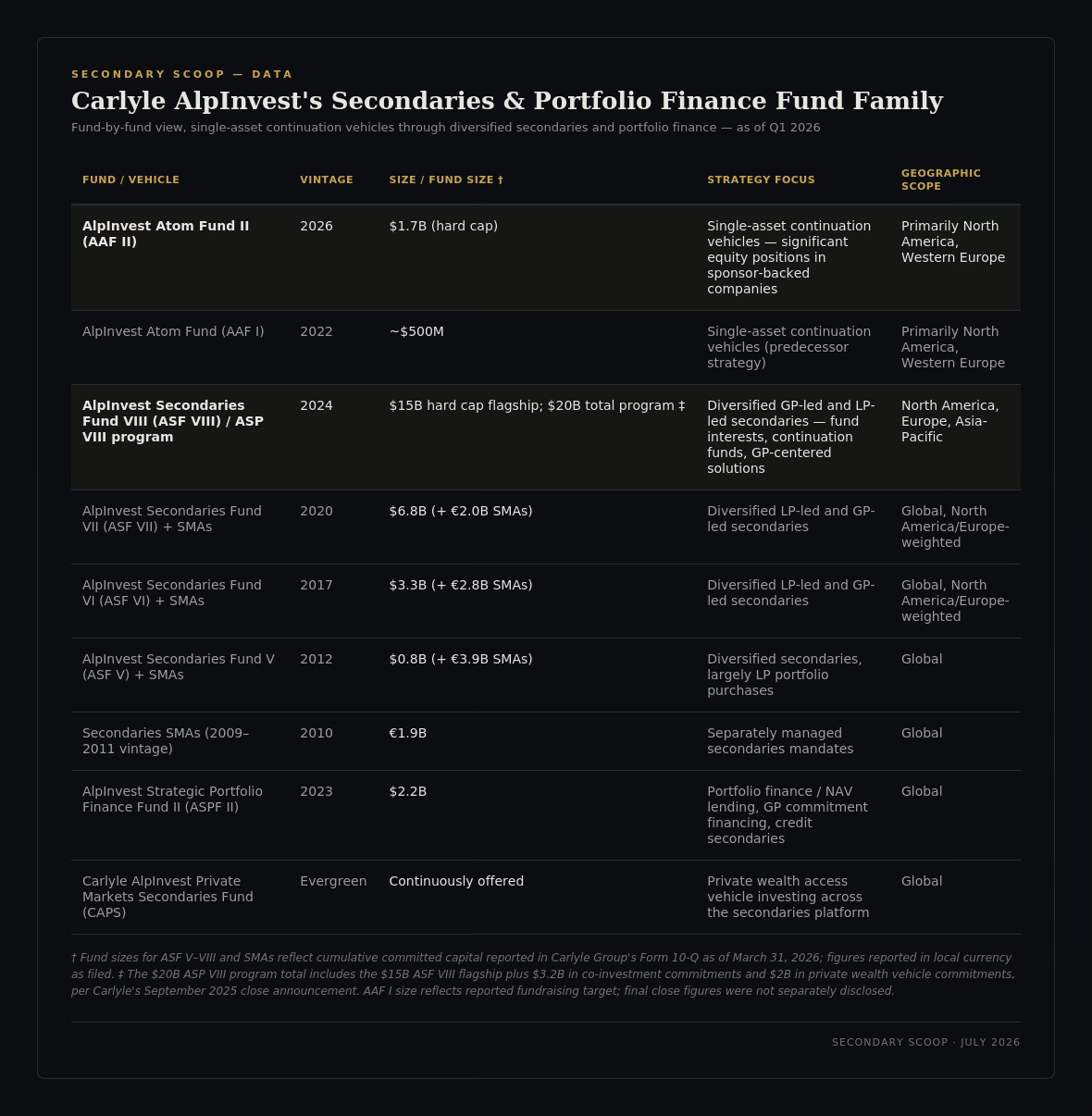

Carlyle AlpInvest announced on July 15 the final close of AlpInvest Atom Fund II (”AAF II”), its second fund dedicated exclusively to single-asset continuation vehicle (”SACV”) transactions.1 The fund closed at its $1.7 billion hard cap, above an original $1 billion target, and, combined with the firm’s evergreen secondaries vehicles and related sidecars, brings AlpInvest’s total dedicated SACV investment capacity to $7 billion for the current investment period.1

On its own, that’s a fundraising story: a sequel fund more than tripling its predecessor’s size, backed by institutional capital from 26 countries spanning pensions, sovereign wealth funds, insurers, banks, endowments, and family offices.1 But the more interesting story is what AAF II confirms about how AlpInvest has chosen to organize its entire secondaries business, and what that organization says about where the broader market is heading.

From $500 Million to $1.7 Billion in Four Years

AlpInvest’s first single-asset vehicle, Atom Fund I, launched in late 2022 targeting $500 million, a modest, almost experimental allocation at the time, arriving as the firm was navigating a co-head transition and beginning to rebrand parts of its secondaries platform. AAF II’s $1.7 billion close represents more than a threefold increase in roughly four years, a trajectory that echoes, and arguably outpaces, the doubling the firm’s flagship commingled secondaries fund achieved over the same period.

That parallel is the editorial hook here. AlpInvest isn’t simply raising more capital across its existing secondaries sleeve; it has built a second, structurally distinct vehicle purely for single-company exposure, and that vehicle is now scaling at a faster clip than the diversified flagship. Single-asset CVs were, for years, executed opportunistically out of multi-strategy secondaries pools. A dedicated, repeat, hard-capped fund line is a different signal: it tells GPs that AlpInvest can underwrite and lead the largest, most concentrated continuation deals with capital that was raised specifically for that purpose, not capital being stretched across a diversified secondaries mandate.

“What sets Carlyle AlpInvest apart in this market is not just the dedicated capital, but the platform behind it.”— Julian Rampelmann, Partner, Head of Single-Asset Secondaries and Deputy Head of Secondaries and Portfolio Finance, Carlyle AlpInvest

The Architecture Behind the Announcement

To understand where AAF II sits, it helps to see the full stack. AlpInvest’s Secondaries & Portfolio Finance strategy is now the largest single business line within the platform’s total $106.9 billion in assets under management as of March 31, 2026, ahead of both co-investments and primary fund investments.2 That is itself a notable shift for a firm whose roots and brand were built on primary fund commitments.

WHERE THE $48 BILLION COMES FROM

Carlyle discloses AUM across three platform-wide buckets: Secondaries & Portfolio Finance, Co-Investments, and Primary & Other. As of Q1 2026, that split was roughly $48 billion in Secondaries & Portfolio Finance, $24 billion in Co-Investments, and $35 billion in Primary & Other, against $106.9 billion in total AlpInvest AUM.2 Secondaries & Portfolio Finance has grown from a distinctly minority sleeve a decade ago to the platform’s single largest strategy, the clearest quantitative marker of the same shift AAF II illustrates qualitatively.

Reading the Deal, Not Just the Release

The single-asset category deserves scrutiny on its own terms, separate from AlpInvest’s specific fund. Single-asset continuation vehicles concentrate risk on one sponsor’s conviction about one company, which is precisely why dedicated capital pools, rather than allocations carved out of diversified funds, have become the industry’s preferred underwriting structure. A diversified secondaries fund sizing single-asset exposure as one line item among dozens faces a different portfolio construction problem than a fund built to concentrate capital in a handful of the highest-conviction, largest-check transactions in the market.

AlpInvest frames the SACV strategy as a natural extension of sponsor relationships built over 25 years and roughly $7 billion committed across 31 transactions in the strategy since 2018.1That track record matters for a market where SACV pricing and structuring still varies significantly by lead investor sophistication, and where the largest transactions increasingly require a lead that can write the full check rather than syndicate it down.

Editorial note on sourcing: Figures on AAF II and the firm’s $7 billion SACV capacity are drawn from Carlyle AlpInvest’s July 15, 2026 press release. AUM segmentation and individual fund sizes for ASF V through ASF VIII and ASPF II are cross-referenced against Carlyle Group Inc.’s Form 10-Q for the quarter ended March 31, 2026, filed with the SEC — not restated from secondary press coverage. As this announcement originates directly from Carlyle AlpInvest, readers should weigh the framing of its own track record and market positioning accordingly.

Sources: [1] Carlyle AlpInvest press release, July 15, 2026. [2] Carlyle Group Inc. Form 10-Q, quarter ended March 31, 2026, and Q1 2026 earnings supplement, filed with the U.S. Securities and Exchange Commission.