Bain & Company’s Private Equity Midyear Report 2026 arrives with a headline message about dealmaking stagnation and AI disruption. Buried inside, however, is a short passage that deserves more attention from the secondaries market: continuation vehicles, the report states, are “becoming harder to execute as LP scrutiny intensifies.”

That sentence, from one of the most widely read institutional research firms in private equity, lands at a significant moment. GP-led secondaries volume reached $115 billion in 2025, according to Jefferies — up 53% year-over-year, with continuation vehicles representing 89% of that activity. The market has spent the better part of three years arguing that CVs have matured from an opportunistic tool into a structural feature of the private equity ecosystem. Bain’s midyear read suggests that structural case now faces a real test.

The mechanics of the friction

The report identifies the core tension clearly. A four-year stretch of record-low distributions has left LPs across the institutional landscape starved for cash. The implied capital cycle for the buyout industry now sits at approximately seven years — well above historical norms. Roughly one in five LPs, per an April 2026 ILPA poll cited in the report, are actively reducing their buyout allocations due to liquidity pressure or lower return expectations.

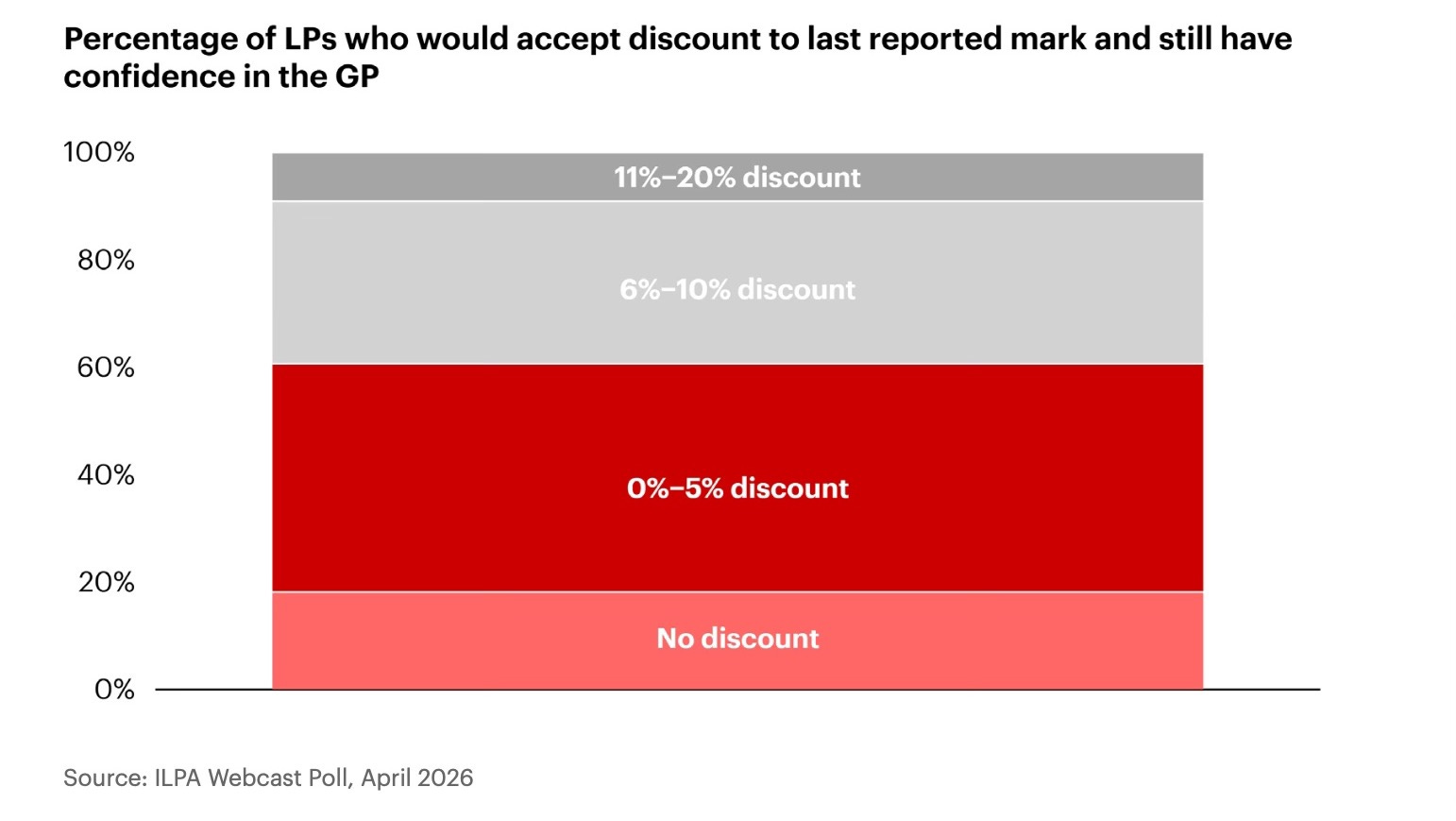

That creates an obvious appetite for liquidity solutions. The complication is that the same distribution drought has made LPs acutely sensitive to the price at which liquidity arrives. The report cites a separate ILPA poll finding that the majority of LPs begin losing confidence in a GP once an exit discount to last reported mark exceeds 5%. For GPs running continuation vehicle processes, this is a narrow corridor to navigate: LPs need liquidity, but not at a price that calls their portfolio marks into question.

The result is a self-reinforcing tension. GPs are reluctant to bring assets to market at discounts that would undermine LP confidence in their valuation discipline. LPs, meanwhile, are increasingly skeptical of marks on assets that were underwritten before the pandemic and have since weathered inflation, rate hikes, trade disruption, and now AI-driven uncertainty. The longer an asset sits — and Bain’s data shows that a majority of buyout NAV in North America and Western Europe comes from assets acquired in 2021 or earlier — the more that skepticism compounds.

A harder market for second-tier assets

Bain is careful to note that the secondary market is not broken. High-quality assets with strong strategic value continue to clear, and at strong prices. The friction is concentrated in what the report calls “a second tier of assets” — older or more challenged positions where buyers cannot get comfortable with proposed marks given uncertainty about future performance.

This has direct implications for the CV market. The continuation vehicle as a product was built, in part, on the premise that it allows GPs to ring-fence their best assets and offer LPs a clean choice: roll or exit at fair value. That logic holds for genuinely premium assets. For the broader portfolio of aging positions — the 2018–2021 vintages that have been through years of disruption without producing distributions — executing a CV process that satisfies LP price expectations is becoming structurally harder.

The MSCI data in the report offers some counterweight. More than 75% of buyout assets are still exiting above their next-to-last quarterly mark, broadly consistent with historical patterns. The relationship between marks and realized exit values has, so far, held up better than LP perception might suggest. But perception matters in fundraising, and LP confidence in GP marks is an input to every CV negotiation.

Our Secondaries’ read

The Bain report does not cover secondaries market volumes or fundraising — for that, the Jefferies and Evercore annual reviews remain the primary sources. What it adds is a granular picture of the LP behavior dynamics feeding into secondary deal flow: the distribution drought, the valuation sensitivity, the mounting pressure on aging portfolios.

The 5% markdown tolerance threshold from the ILPA poll is the most operationally specific data point in the report for secondaries practitioners. It quantifies, with survey evidence, the pricing band within which GP-led processes must operate to preserve LP relationships. As CV volume scales and the asset quality distribution widens — from flagship single-asset processes to older, more challenged fund restructurings — that 5% ceiling will be tested with increasing frequency.

Bain’s warning on CV execution difficulty is not a prediction of market reversal. It is a calibration: the easy part of the GP-led boom, when any high-quality asset could clear a CV process with LP support, may be giving way to a more selective, more negotiated, and more LP-scrutinized market. That is, ultimately, a sign of a maturing asset class — but maturation has friction costs, and 2026 is where those costs are beginning to show up.

Sources: Bain & Company, Private Equity Midyear Report 2026. ILPA Webcast Poll, April 2026. MSCI Private Capital Solutions. Jefferies Global Secondary Market Review, January 2026.

| A guest post by

|