On May 20, EQT gathered investors and analysts in London for its annual Value Creation Day — a 122-slide presentation covering everything from AI infrastructure to Asian buyouts. Buried in the endnotes and performance slides, almost without fanfare, were the first investor-facing financial disclosures for what will become EQT's Secondaries & Solutions segment. The H1 2026 report on July 17 will be the first time those numbers appear in a consolidated earnings release. This is the preview.

The Performance Baseline

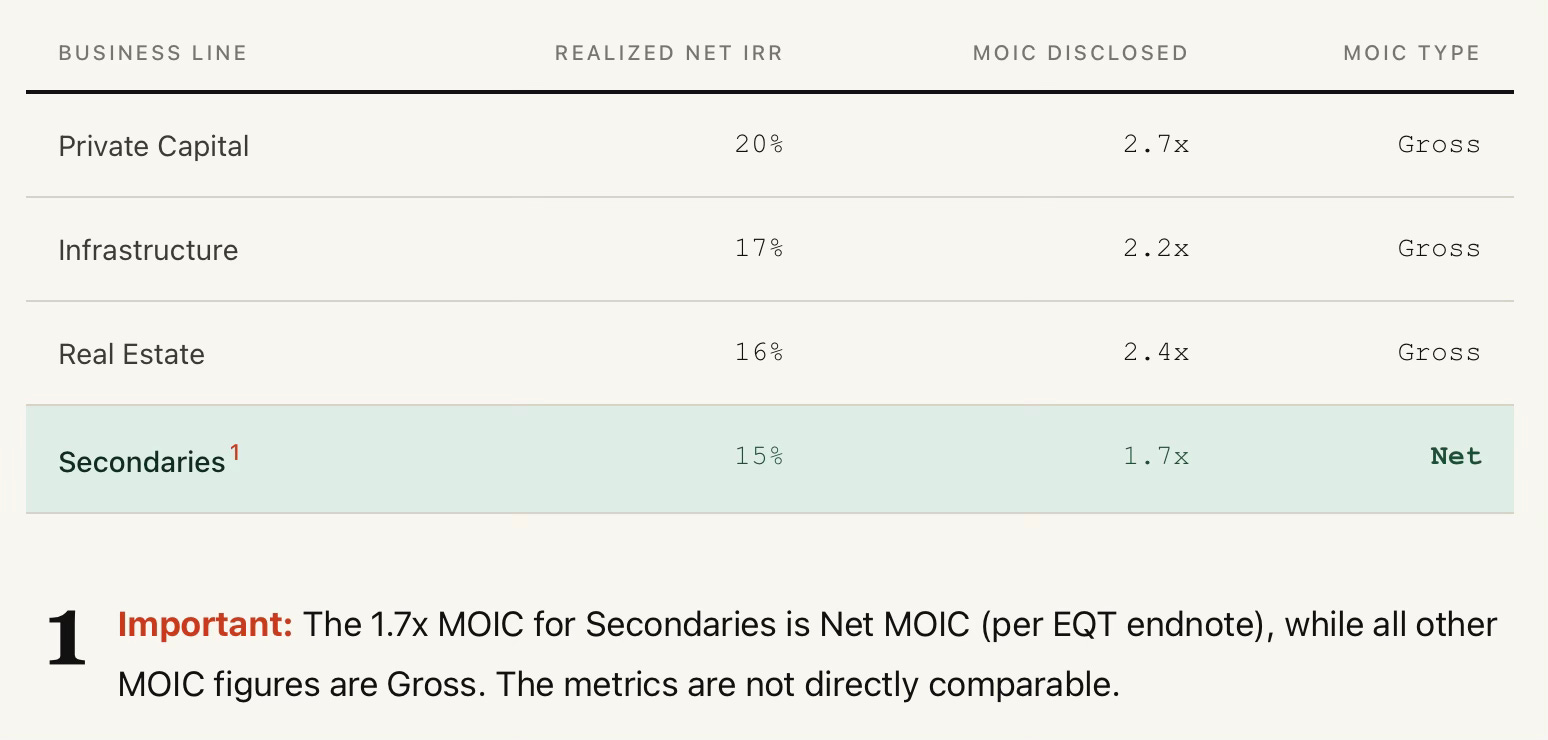

EQT now presents four business lines with their own realized return metrics: Private Capital, Infrastructure, Real Estate, and Secondaries. For Secondaries — Coller Capital’s track record — the deck shows a 15% realized Net IRR and a 1.7x realized MOIC. Both are competitive numbers for a top-tier dedicated secondaries manager.

Although, the other three business lines show Gross MOIC. The endnote confirms that the 1.7x for Secondaries is actually Net MOIC. To put it in perspective: if Coller's MOIC were restated on a gross basis — as EQT reports for its other three strategies — the number would be higher than 1.7x. How much higher depends on the fee and carry structure, but the direction is clear. The Secondaries segment may be closer to its peers than the slide suggests.

The Financial Projections

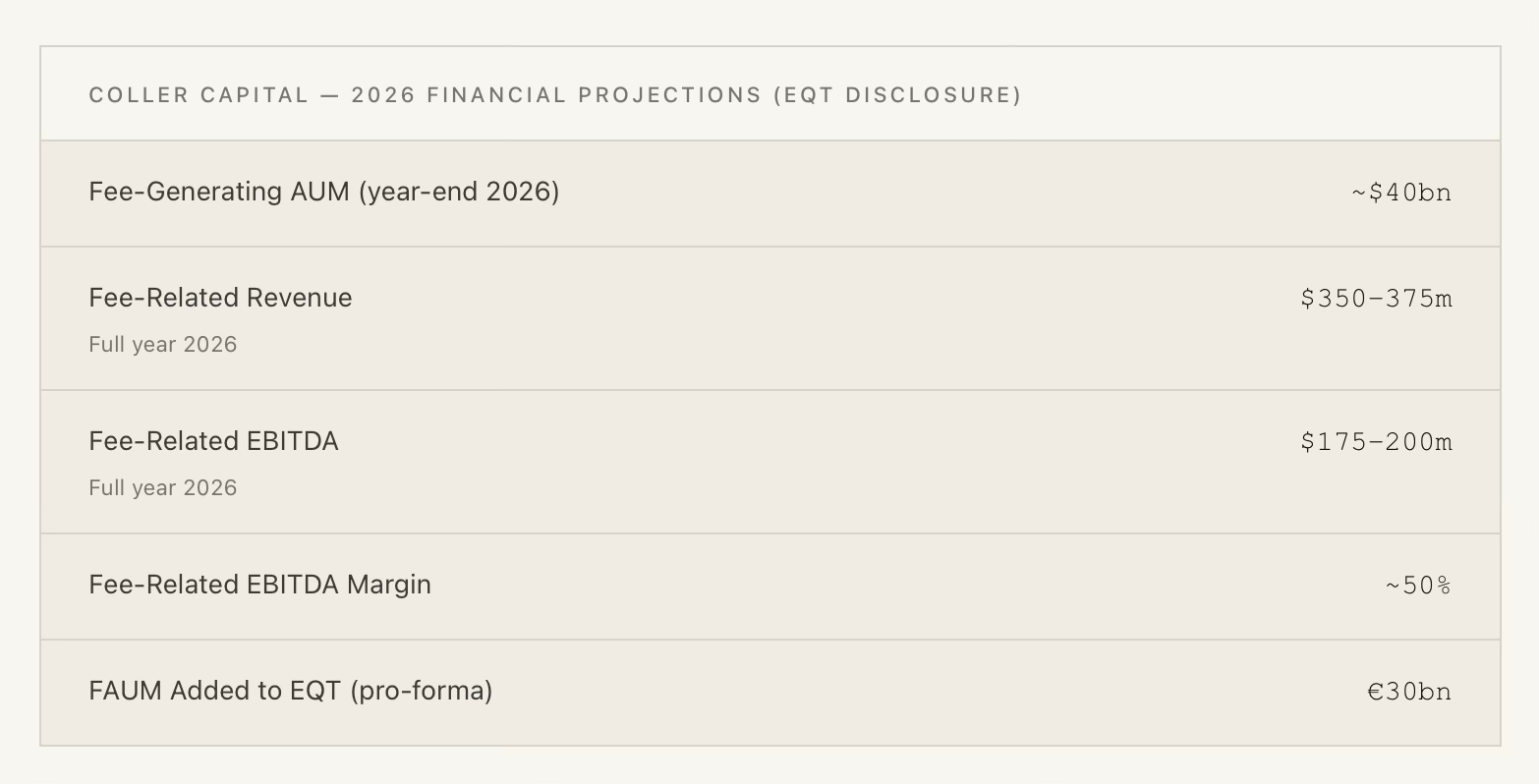

Beyond performance, the Value Creation Day endnotes contain something more forward-looking: EQT’s own projections for what Coller Capital will contribute financially in 2026. These figures were disclosed as part of the transaction rationale at announcement in January, but their appearance in a capital markets day presentation — in the context of a firm talking to shareholders — gives them a different weight.

A ~50% fee-related EBITDA margin is notable even by alternative asset management standards. For context, the listed alternatives managers that most investors use as a reference point — StepStone, Hamilton Lane, Partners Group — typically report FRE margins in the 35–45% range. A 50% margin on a dedicated secondaries platform reflects the relatively lean operating model of a focused fund manager: Coller does not run a large direct investment team, does not require operational resources to manage portfolio companies, and benefits from the scale of managing large pools of capital with a relatively small professional headcount.

The $40bn fee-generating AUM figure is also important to contextualize. Coller’s total AUM at close is approximately $49bn — the gap between total AUM and fee-generating AUM reflects assets in older, winding-down funds that are past their fee-earning periods. The $40bn figure is the commercially relevant number: it is the base on which management fees are calculated and against which any new fundraising adds directly to fee revenue.

AI is a generational opportunity for Real Assets, Private Capital and Secondaries — our platform is built to capture it at scale.

— EQT VALUE CREATION DAY 2026, CLOSING STRATEGIC SUMMARY

What the July 17 Report Will Tell Us

EQT’s H1 2026 half-year report — scheduled for July 17 — will be the first earnings release in which Coller Capital’s financials appear as a consolidated segment, assuming the transaction closes on its expected mid-to-late Q3 2026 timeline. There is a real possibility that the close happens after the H1 reporting date, in which case Coller will not yet be consolidated but EQT may provide a pro-forma view. Either way, July 17 is the first moment at which the secondaries strategy shifts from a transaction story to a business performance story.

The questions that report needs to answer — and that the Value Creation Day data now allows us to benchmark against — are straightforward. Is Coller’s fee-generating AUM on track to reach $40bn by year-end? Are revenues running at the $350–375m pace? And critically: how is the integration being structured — does Coller operate as a standalone segment with its own reporting, or does EQT fold it into a broader solutions-oriented line that makes segment-level performance harder to parse?

For secondaries market watchers, the integration of Coller into EQT is not just a consolidation story. It is the first test of whether a dedicated secondaries platform can maintain its performance edge inside a large, multi-strategy manager — a question the industry has not yet had to answer at this scale. The $3.2bn acquisition price implies a high bar. The 50% EBITDA margin tells you Coller is a structurally excellent business.

| A guest post by

|