Born in America: How the U.S. Built, and Still Runs, the Secondaries Market

The world's largest single secondaries fund was raised in Paris. But the market itself, its dominant transaction volume, and most of its largest franchises are unmistakably American.

Ahead of the Fourth of July: the world's largest single secondaries fund was raised in Paris. But the market itself, its dominant transaction volume, and most of its largest franchises are unmistakably American. What follows is the case for the U.S. as the center of gravity in private capital secondaries, and the one Parisian exception that proves the rule.

A market with a birth certificate

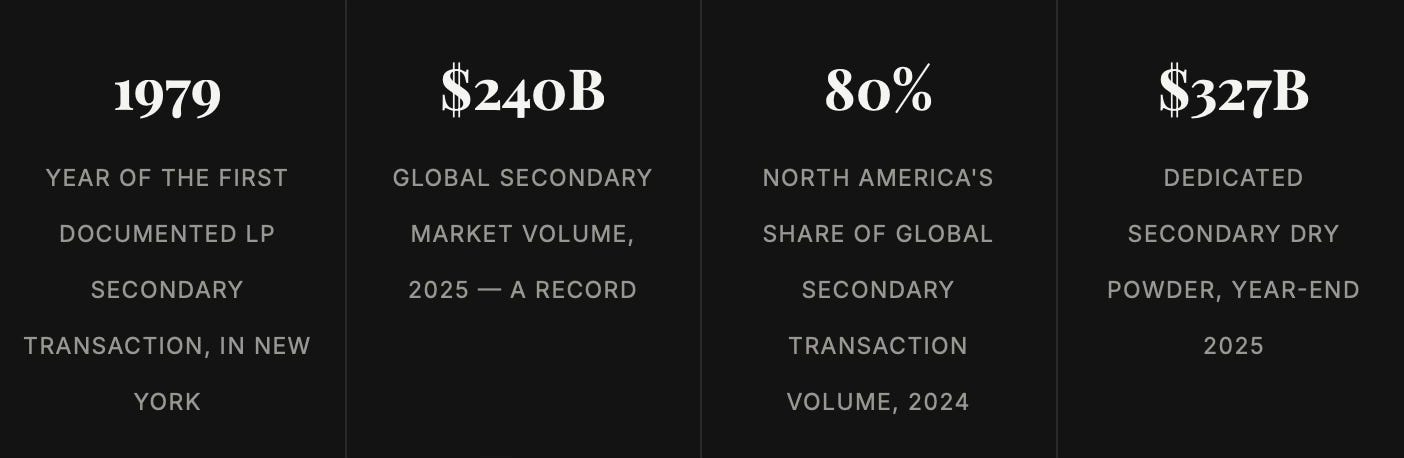

Most corners of private markets claim gradual, contested origins. Secondaries has an actual founding moment. In 1979, a financier named Dayton Carr (who died in 2020 at age 78) bought IBM’s limited partnership interests in a handful of venture capital funds, widely credited as the first LP secondary transaction on record. Three years later, Carr formalized the trade into a business, launching the Venture Capital Fund of America (VCFA) in 1982 with $6 million, the first fund dedicated entirely to buying up other people’s fund stakes.

In 1979, a financier named Dayton Carr bought IBM’s limited partnership interests in a handful of venture capital funds, widely credited as the first LP secondary transaction on record.

At the time, there was no market to speak of. An LP that needed liquidity from a locked-up venture or buyout fund had essentially nowhere to go. VCFA created the counterparty that didn’t previously exist.

The rest of the 1980s filled out the founding roster, and this is where the U.S. story picks up its one durable rival: Pantheon launched one of the first dedicated secondary vehicles, Pantheon International Participations, out of London in 1988, and Coller Capitalwas founded in London a year later, in 1989. The same year, on the other side of the Atlantic, Landmark Partners was founded in Connecticut by Stanley Alfeld, John Griner, and Brent Nicklas, a firm that would go on to become one of the longest-running secondaries franchises in the industry before Ares acquired it in 2021.

So the honest version of the origin story is transatlantic from year one. What happened over the following four decades is what turned this into an American-led market: scale.

From back-office niche to portfolio management tool

For two decades, secondaries stayed a workaround, a market for distressed sellers, defaulting LPs, and funds nobody wanted to talk about. Annual volume didn’t reliably clear $1 billion until the 2000s. The market’s reputation problem (secondaries as a “signal of distress”) took root here and has taken Secondary Scoop’s entire editorial thesis to unwind.

Two shocks, both centered on U.S. institutional capital, changed that.

THE MECHANISM

The denominator effect, 2022. When public equities fell sharply in 2022, the private allocations sitting on U.S. pension, endowment, and foundation balance sheets, priced on a lag and marked more slowly, suddenly represented an outsized share of total portfolio value. Funds kept calling capital regardless. Institutions that found themselves over their private equity targets did the only thing they could do to rebalance without waiting for distributions: they sold fund stakes on the secondary market. That single dynamic, concentrated among America’s largest LPs, is broadly credited with pulling secondaries out of the niche and into the standard toolkit.

The second shock ran in the opposite direction, from GPs rather than LPs. Continuation vehicles, where a sponsor moves one or more portfolio companies into a new, purpose-built fund instead of selling them outright, first appeared in meaningful volume after the 2008 financial crisis, as GPs looked for ways to hold onto assets through a dead exit market. They stayed a niche, discount-heavy product through the 2010s. Then adoption inflected: single-asset continuation vehicle volume ran to roughly $70 billion between 2021 and 2023, more than three times the $21 billion transacted from 2018 to 2020. By 2025, nearly 80 percent of the top 100 sponsors globally by assets under management had completed at least one CV transaction, and GP-led deals reached $115 billion for the year, 48 percent of the total secondary market, up 53 percent year over year, according to Jefferies.

The market wasn’t handed liquidity by IPOs or strategic buyers. It built its own, and the largest pool of institutional capital and the largest inventory of aging private assets both happen to sit in the United States.

The scoreboard: who actually runs this market

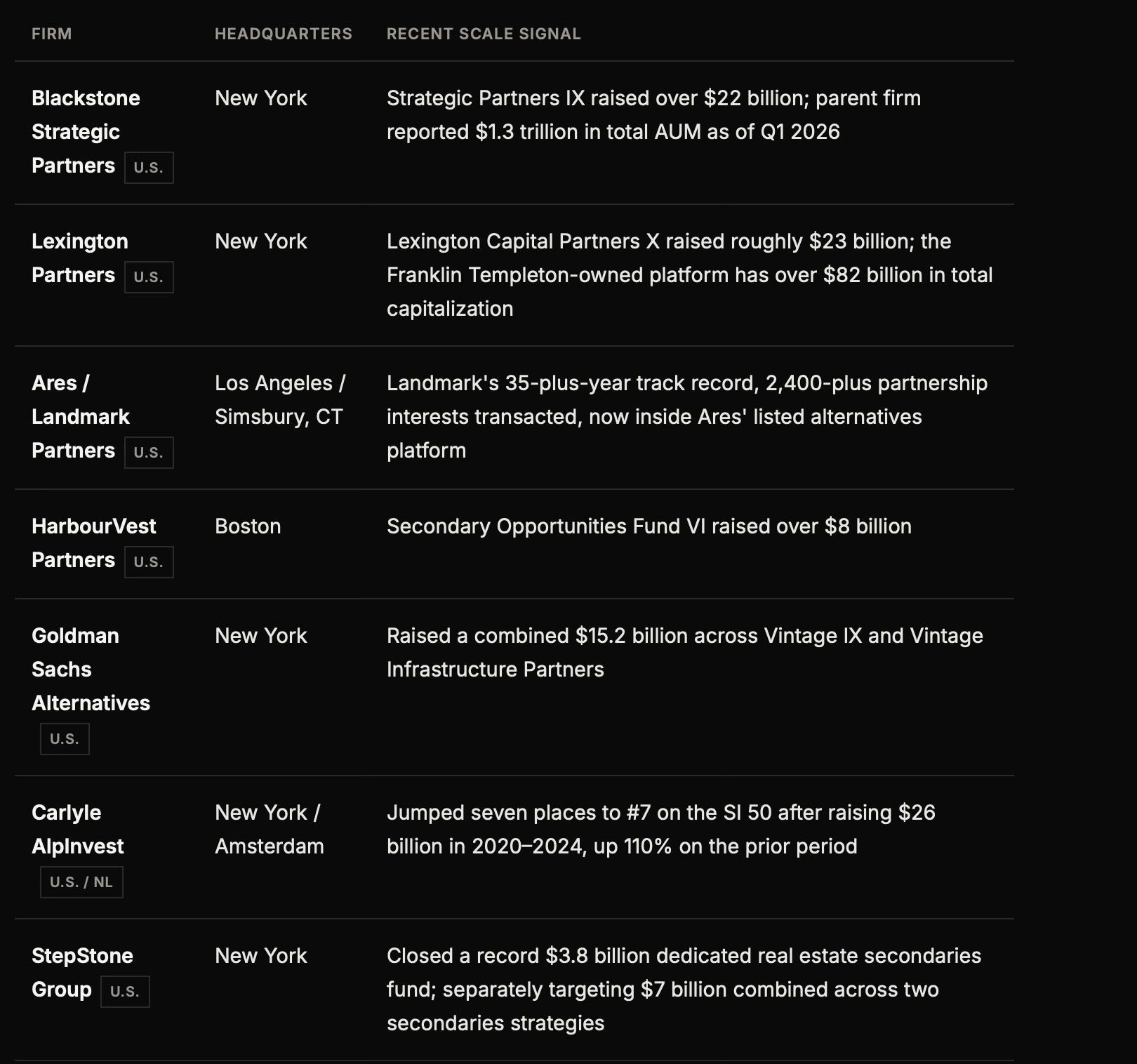

Rank the industry by dedicated secondaries capital raised over the past five years, and one name sits above everyone else, and it isn’t American. Ardian, headquartered in Paris, closed Ardian Secondary Fund IX at $30 billion in 2023, the largest secondaries fund ever raised, and tops Secondaries Investor’s SI 50 ranking of the world’s largest firms. Any honest accounting of “who’s king” has to start by naming the exception.

Past that top line, though, the depth chart is overwhelmingly American.

Fund sizes reflect most recent publicly reported closes as of mid-2026; see sources below. Coller Capital (London) and Pantheon (London) remain major global players but are excluded here as non-U.S.-headquartered.

Zoom out to the full SI 50 ranking and the pattern holds: the top 50 secondaries firms collectively raised $522.5 billion between 2020 and 2024, and a clear majority of that capital sits with U.S.-headquartered managers, even with Ardian at the very top of the list.

WHY THE VOLUME FOLLOWS THE FLAG

Capital raised by U.S. managers is one measure. Where the deals actually happen is another, and it’s less ambiguous: North American funds represented 80 percent of global secondary transaction volume in 2024, up from 68 percent in 2023, per Jefferies’ Private Capital Advisory group. Three structural facts explain why that share sits where it does.

The asset base is American-sized. U.S. private equity alone generated $1.1 trillion in deal activity across more than 8,200 transactions in 2025, and the U.S. PE universe now holds upward of 13,000 portfolio companies — about eight years of inventory at the current pace of exits, with 30 percent of companies aged seven years or older. Buyout funds globally are sitting on a record $3.8 trillion of unrealized value; a disproportionate share of that overhang is American, because the American buyout market is simply larger than any other. More aging NAV means more that eventually needs to trade.

The LP base is the deepest and most price-insensitive in the world. U.S. public pensions, university endowments, and foundations built the largest, longest-tenured institutional allocations to private equity anywhere — which is precisely the base that generated the 2022 denominator-effect selling wave and continues to generate the largest, most routine LP-led portfolio sales today.

The wealth channel innovation is happening here first. Franklin Templeton and Lexington Partners launched the first registered tender-offer private equity secondaries fund built for the U.S. wealth channel, part of a broader ‘40-Act evergreen fund wave that pulled retail and semi-liquid capital into the market. Evergreen vehicles brought in an estimated $113 billion of inflows in 2025 alone, with roughly 41 percent of that allocated to secondaries strategies — a distribution channel U.S. asset managers built first and still dominate.

CONTEXT

None of this erases the European side of the ledger. Ardian’s scale, Coller’s five-decade track record, and Pantheon’s founding role all sit outside the U.S. And Secondary Scoop’s own editorial focus runs toward European market dynamics for good reason — CV activity, LP-led volume, and fundraising are all scaling faster off a smaller base in Europe than in the U.S. right now. But scaling faster off a smaller base is not the same as leading. On raw transaction volume, LP depth, and franchise count, the U.S. remains the market’s center of gravity, and has been since Dayton Carr bought IBM’s fund stakes in 1979.

The independence angle

There’s a version of this story that fits the holiday without straining for it. Private equity’s entire liquidity model was historically dependent on two exits it didn’t control: the IPO window and the M&A cycle. Both are set by public market sentiment, interest rates, and buyer appetite — conditions no GP or LP can engineer. What the U.S. secondaries market did, starting with a single trade in 1979 and compounding through four decades of institutional adoption, was build a third exit route that private capital controls on its own terms. That’s not a distress mechanism. It’s the industry declaring liquidity independence from public markets — a distinctly American origin story for a genuinely global tool.