Built Over 25 Years, Still Accelerating: Hamilton Lane's Secondaries Machine

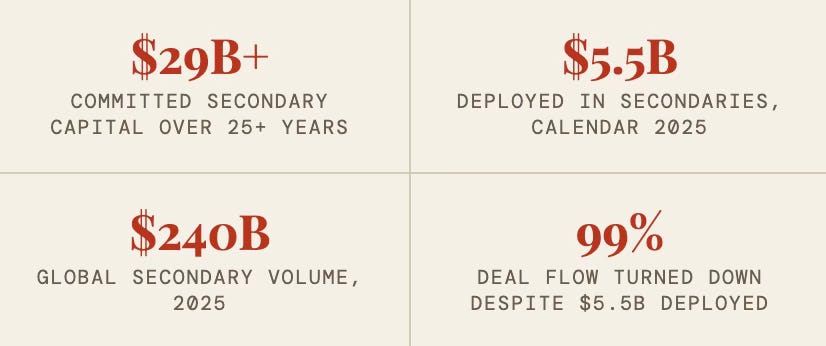

Twenty-five years in secondaries, $29 billion committed, and three fund vehicles simultaneously in market.

When Eric Hirsch, co-CEO of Hamilton Lane, addressed analysts on the firm’s Q4 and fiscal year 2026 earnings call last week, he devoted more time to the secondaries market than to any other single asset class. That was not an accident. Secondaries has become the strategic center of gravity at Hamilton Lane — the segment where the firm’s data advantages, LP and GP relationships, and 25-year track record converge most powerfully.

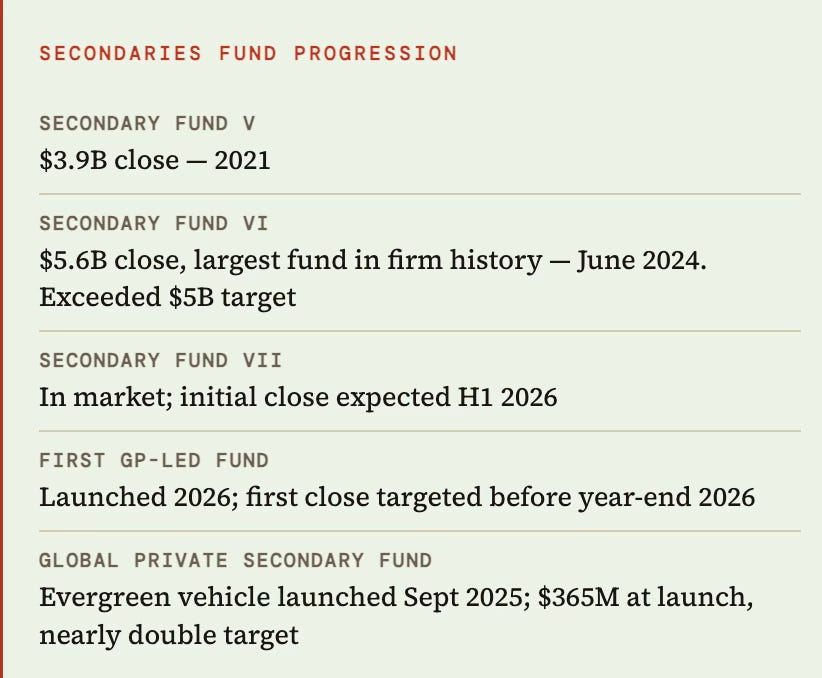

The headline numbers are striking. Hamilton Lane has now committed over $29 billion to secondaries across its platform’s history, deployed $5.5 billion in calendar 2025 alone, and is simultaneously running three distinct secondaries vehicles in market: its seventh closed-end LP-led secondary fund, its first dedicated GP-led secondary fund, and a growing suite of secondaries-focused Evergreen vehicles for both institutional and private wealth investors.

Yet the firm’s own description of its market position is notable for its candor. “If you look at us on a stack rank, weighting from just capital under management in the secondary space, we’re sort of a mid-tier player who has aspirations to be a top-tier player,” Hirsch told analysts. “We think we’ve got a lot of room to grow in that market environment.”

Hamilton Lane’s secondary history begins in the late 1990s, well before the market had reached any meaningful institutional scale. The firm completed its first GP-led transaction in 2014 — years before continuation vehicles became a mainstream tool — and has since built what it describes as a $20 billion-plus secondary platform through six closed-end fund vintages.

The fund progression tells a clear growth story. Secondary Fund V closed on $3.9 billion in 2021. Secondary Fund VI closed in June 2024 at $5.6 billion — the largest fund in Hamilton Lane’s history at the time, materially exceeding its $5 billion target — drawing from corporate and public pension funds, sovereign wealth funds, endowments, foundations, and private wealth platforms across more than 30 countries.

At the time of that close, Hamilton Lane’s secondaries platform stood at approximately $20.9 billion in assets under management. By the FY2026 earnings call, the figure had grown to over $29 billion in total committed capital across the platform’s history — a figure Hirsch cited as context for the firm’s scale and deal selectivity.

“Secondaries continue to offer one of the most compelling risk-reward profiles across private markets. Even after a record 2025, with a reported $240 billion of transaction volume completed, the market remains supported by a favorable supply-demand dynamic.”

— ERIC HIRSCH, CO-CEO, HAMILTON LANE — FY2026 EARNINGS CALL, MAY 21 2026

The Return Model: Appreciation, Not Just Discount

One of the most substantive parts of Hirsch’s secondaries commentary addressed a widespread misconception about how secondary returns are actually generated. The conventional narrative holds that secondaries managers earn their returns primarily by buying at a discount to NAV. Hamilton Lane’s data tells a different story.

“After over 25 years of doing secondary deals and over $29 billion of committed capital, nearly 70% of our performance is achieved from the appreciation of the underlying investments post-purchase”

— ERIC HIRSCH, CO-CEO, HAMILTON LANE — FY2026 EARNINGS CALL, MAY 21 2026

“After over 25 years of doing secondary deals and over $29 billion of committed capital, nearly 70% of our performance is achieved from the appreciation of the underlying investments post-purchase,” Hirsch said. “About 30% of our return came from good purchasing and good structuring.”

This framing has direct implications for how Hamilton Lane approaches pricing. The firm has paid premiums to NAV in numerous instances — explicitly — when conviction on underlying asset quality justifies it. “If we have high conviction that an asset marked today at $1 will ultimately be worth and sold for $3, we might gladly pay the seller $1.50 today,” Hirsch explained. When that happens, Hamilton Lane takes the asset onto its books below what it paid, showing a near-term loss — a deliberate choice that prioritizes long-term value over short-term optics.

The approach is validated by recent exit data. In Hamilton Lane’s sixth secondary fund, from calendar 2023 through 2025, there were more than 340 individual company exits across the underlying portfolio. On average, those assets were monetized at values nearly 9% above where they were marked two quarters prior to exit — consistent with the firm’s thesis that underlying company performance, not entry discount, is the primary driver of secondary returns.

The Market Context: Supply-Demand Still Favors Buyers

Hamilton Lane’s secondaries outlook is grounded in a structural market observation: despite record volumes, the secondary market remains supply-heavy relative to available capital. In 2025, the market transacted approximately $240 billion in volume — a record — yet available dry powder covers that volume at roughly one times. That imbalance, in Hamilton Lane’s view, continues to create an attractive backdrop for buyers: discounted entry, faster distributions, and a more muted J-curve.

Hirsch placed this within a longer arc of market growth. Secondary volume has grown at 18% annually from 2013 through 2024, with 2024 itself hitting a record $162 billion before 2025 surpassed even that. Hamilton Lane’s own deal flow reflects the scale: in calendar 2025, the firm reviewed enough secondary transactions to have deployed $5.5 billion while turning down 99% of total dollar deal flow. Hirsch was explicit that the rejection rate is not a function of competition pricing it out — it is a function of quality standards.

“We’re looking for really high quality assets managed by really high quality fund managers at an appropriate price,” he said. “The luxury of having as much deal flow as we have means that the team doesn’t need to agonize over things that don’t quite hit the bar. They just have a quick no, and they move on to the next thing.”

The GP-Led Expansion: A New Fund, a Long History

The most significant product announcement on the earnings call was the launch of Hamilton Lane’s first dedicated GP-led secondary fund. The timing reflects the segment’s maturation: what was an emerging transaction type a decade ago is now, in Hirsch’s words, “a mainstream high-quality part of the secondary toolkit.”

Hamilton Lane is not new to GP-leds. The firm completed its first continuation vehicle transaction in 2014, building a track record across buyout GP-led deals with a focus on high-quality middle market opportunities alongside GPs with whom it has longstanding relationships. The new dedicated fund formalizes that activity into a standalone vehicle — targeting a first close before calendar year-end 2026.

Hamilton Lane’s own research on the GP-led market, published in February 2026, points to the quality of assets flowing through continuation vehicles: across CV transactions the firm reviewed as an existing LP between Q4 2022 and Q2 2025, the average realized multiple of cost for selling funds was 4.5x across multi-asset CVs and 3.9x across single-asset CVs. GP alignment is also high — average GP commitment to CVs over the past three years has been approximately 9% of total commitments, with GPs rolling 100% or more of realized carry proceeds in 88% of deals.

“High-quality managers are now using GP-leds as a regular portfolio management tool, and in some cases, as an alternative to a traditional M&A exit or IPO.”

— ERIC HIRSCH, CO-CEO, HAMILTON LANE — FY2026 EARNINGS CALL, MAY 21 2026

Democratizing Secondaries: The Evergreen Push

Beyond its institutional closed-end franchise, Hamilton Lane has moved aggressively to bring secondaries exposure to a broader investor base through its Evergreen platform. In September 2025, the firm launched the Hamilton Lane Global Private Secondary Fund (HLGPS) — its 10th Evergreen vehicle and the first dedicated to secondaries within the platform. The fund opened to accredited high-net-worth investors and institutions across Europe, the Middle East, Asia, Latin America, and Canada. Demand at launch nearly doubled the target size, with commitments exceeding $365 million at commencement.

James Martin, Head of Global Client Solutions at Hamilton Lane, described the rationale at launch: “The secondary market has evolved into a permanent fixture in private markets and is one of the fastest growing strategies today, as evidenced by this fund being oversubscribed.”

By the FY2026 earnings call, Hamilton Lane’s overall Evergreen platform — which now includes multiple secondaries-focused vehicles — had reached $17.5 billion in total AUM, representing 64% growth year-over-year. Institutional investors now account for over 25% of inflows into Evergreen products, a share Hirsch described as rising, with large pension plans using Evergreen secondaries vehicles for tactical portfolio construction in ways that closed-end drawdown structures cannot support.

What Comes Next

Hamilton Lane enters the second half of calendar 2026 with three secondaries vehicles simultaneously in market — an unusually broad simultaneous deployment across LP-led, GP-led, and Evergreen structures. The seventh secondary fund and first GP-led fund both target initial closes in the coming months. A separately launched insurance-wrapped vehicle investing in secondary Evergreen offerings is designed to open the insurance channel as a new source of secondaries capital.

The firm’s strategic self-description — mid-tier with top-tier ambitions — is not false modesty. By AUM, Hamilton Lane sits below the dedicated secondaries giants that manage $50 billion or more. But by deal volume, data infrastructure, relationship depth, and the breadth of its product architecture, it is building the infrastructure of a much larger platform. The question, as Hirsch framed it, is not whether the opportunity is there. “The secondary space continues to be one of the most imbalanced in terms of just tons of volume, and frankly, not enough capital,” he said. The question is execution at scale.

| A guest post by

|