Carlyle AlpInvest Thinks Credit Secondaries Will Be $80 Billion by 2030.

Here is what is driving the growth and why the largest players are already positioning credit secondaries as a core part of how private markets will function going forward.

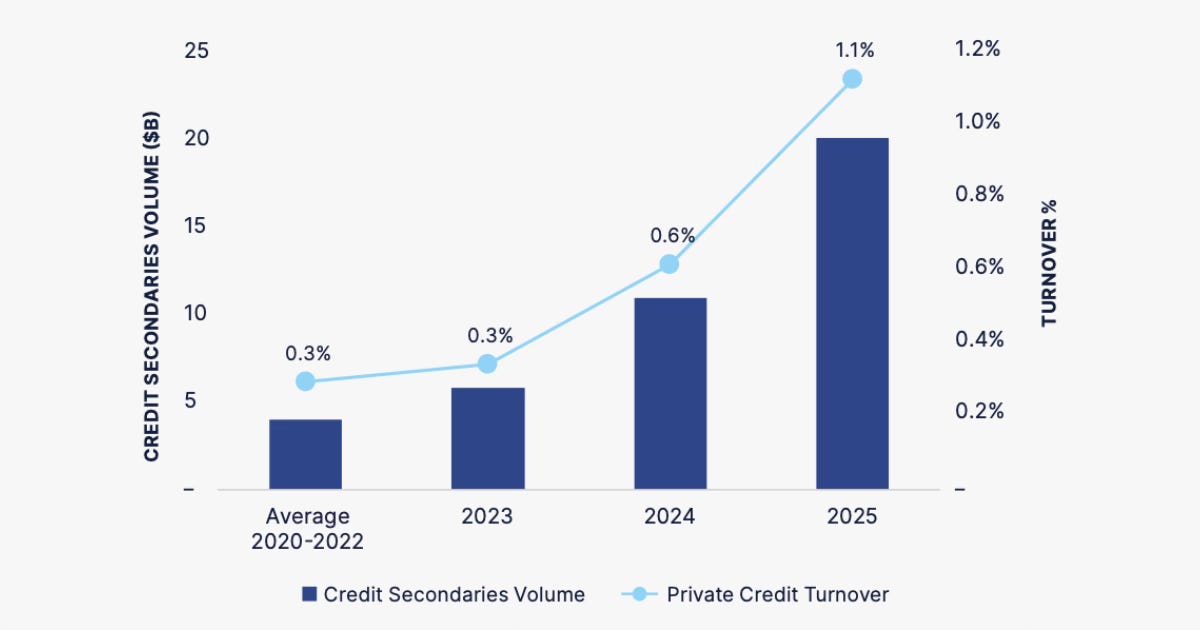

Carlyle AlpInvest estimates the market reached $20 billion in transaction volume in 2025, up from less than $10 billion two years prior. Fund turnover sits at roughly 1% of total private credit AUM, well below the 2 to 3% typical in private equity secondaries. That gap is the opportunity.

“We believe that the credit secondary market is $20 billion today and will grow to over $80 billion by 2030, implying significant runway ahead.” Michael Hacker, Global Head of Portfolio Finance, Carlyle AlpInvest

The firm projects the $80 billion market by 2030 will be driven primarily by GP-centered transactions (~$55 billion), with LP interest sales making up the remaining ~$25 billion.

What Is Driving the Growth

The rise of credit secondaries tracks directly with the growth of private credit itself. Since the Global Financial Crisis, banks pulled back from leveraged lending and private credit managers filled the gap. The overall private credit market now stands at nearly $2 trillion in AUM, growing at a 13% CAGR since 2012, with direct lending alone compounding at 25% over the same period.

As the primary market matured, so did the need for secondary solutions. Private credit funds carry structural duration mismatches: investment periods end, but loans originated late in the cycle often remain outstanding well beyond a fund’s contractual life. Since 2022, rising rates have pushed borrowers toward amend and extend solutions, lengthening loan lives further. LPs holding these funds increasingly need a way out that does not require waiting for natural portfolio runoff.

Perceptions have shifted accordingly. Selling a private credit fund interest used to signal distress. Today, both GPs and LPs treat secondary transactions as a routine portfolio management tool.

Carlyle Is Betting on It

Carlyle’s own commentary from its February 2026 Shareholder Update reinforces the conviction. Co-President John Redett, speaking about the AlpInvest platform, was direct: “Credit secondaries, portfolio finance, and insurance should further accelerate growth when we look forward.” He described the broader secondaries market as doubling in size every four to five years, a tailwind he called both secular and structural rather than cyclical.

That confidence is grounded in scale. They have 375 GP relationships, data on 30,000 companies, and a 25-year track record. Redett noted that 75% of GPs they speak to today plan to use the secondary market in the next two years, up from roughly 25% five years ago.

What Comes Next

The market is still early. A 1% turnover rate on nearly $2 trillion in AUM means current volume is a fraction of what could theoretically trade. Even a move to 1.5% turnover would imply a market roughly double its current size, and it would still trail private equity secondaries penetration rates.

The trajectory from here depends on continued growth in the primary private credit market, broader GP and LP adoption of secondary solutions, and a deepening buyer base with the expertise to underwrite credit risk properly. All three are moving in the right direction, and the largest players are already positioning credit secondaries not as a niche strategy but as a core part of how the private markets ecosystem will function going forward.