Carlyle Goes All-In on Secondaries: The Firm's Biggest Strategic Bet in Q1 2026

Carlyle’s first quarter 2026 earnings call delivered several headlines, but for those of us tracking the secondaries market, there was one unmistakable central message: Carlyle Alpinvest is not just a secondaries platform. It is the defining edge of the entire firm.

The Deal of the Quarter: $5 Billion and a Structure Nobody Has Done Before

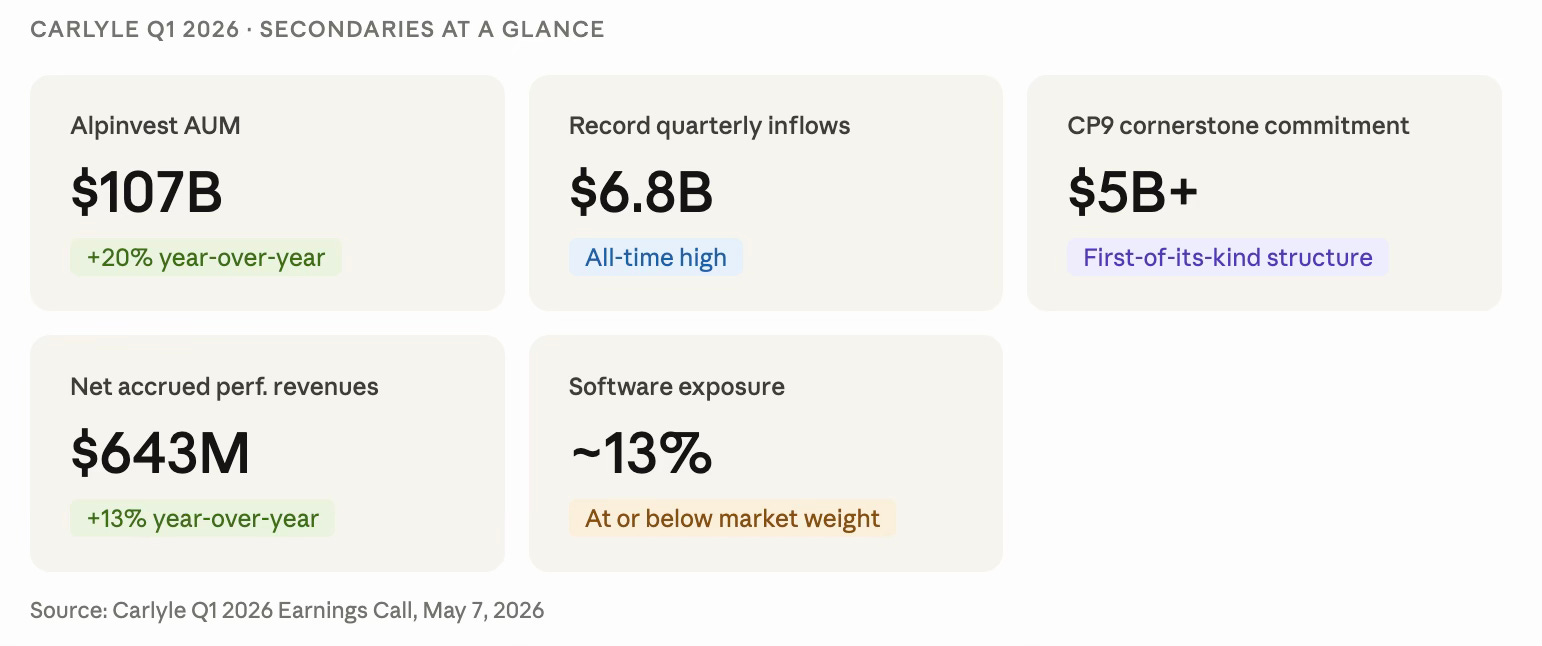

The standout moment of the quarter wasn’t an AUM figure or a return multiple. It was a structured transaction that CEO Harvey Schwartz described as “the first of its kind”: a $5 billion commitment secured for Carlyle’s next U.S. Buyout vintage fund — before the formal fundraise has even launched.

What makes this structure remarkable? It simultaneously solves two client problems in a single vehicle: access to the next buyout fund and liquidity for LPs already sitting in existing positions. In Schwartz’s own words, it was “a win-win situation.” The cornerstone LPs who participated were able to reposition their portfolios, increase their exposure to U.S. Buyout, and get liquidity — all without waiting for a traditional fundraising cycle.

Carlyle holds a subordinated equity position in the structure, aligning the firm’s interests with those of its LPs. Fees, as Schwartz confirmed under analyst questioning, are at full rates. No volume discount.

Alpinvest: Record AUM, Record Inflows, and a Business That Is No Longer Just “Secondaries”

Carlyle Alpinvest closed the quarter with total AUM of $107 billion, up 20% year-over-year. Quarterly inflows hit $6.8 billion — also a record — driven by broad-based institutional and wealth activity across three pillars: secondaries, co-investment, and portfolio finance.

Net accrued performance revenues for Alpinvest reached $643 million, up 13% year-over-year. Segment FRE came in at $68 million, ahead of the prior year despite absorbing $13 million less in catch-up fees.

But the most strategically significant data point was the shift in narrative. Schwartz was deliberate on the call in noting that Alpinvest is often “thought of by people as a secondary business” but that “it really is obviously much more than that.” It is a secondaries business, a primary business, and above all, a solutions business. And it is precisely that third pillar — the ability to deliver bespoke solutions to both GPs and LPs — that is generating the most momentum across the platform.

The Phone Is Ringing Off the Hook

The market reaction was immediate. Following the announcement of the $5 billion structure, Schwartz told analysts that inbound interest had already been significant: people across the industry were reaching out to explore whether they could do something similar — either to create value for their LPs or their GPs.

But Schwartz was also clear about the barrier to entry. “You really have to have the thoughtful experience of a Carlyle Alpinvest team to actually bring this together,” he said. The implication was direct: this is not a structure any firm can replicate overnight. The ability to run secondaries, co-investment, and portfolio finance under one roof — and to deploy all three simultaneously in service of a single client solution — is what made this deal possible.

His conclusion on where the industry is headed was unambiguous: “I just think this is a direction to travel for the industry.”

Risk Management in Secondaries: Vintage, Software, and Diversification

An Evercore analyst asked an uncomfortable but sharp question: given the timing of capital raised in the secondaries market and the types of companies seeking liquidity in those years, does Alpinvest carry higher software and 2021–2023 vintage concentration than it might appear on the surface?

Management’s answer was direct. Software exposure across Alpinvest’s portfolios sits in the low-to-mid teens — characterized by the firm as “market weight or below market weight.” On the vintage question, the team pointed to 25 years of cycle experience and a disciplined portfolio construction approach that explicitly manages diversification not just by manager and position, but by vintage year. The message: they saw 2022 and 2023 valuations clearly, and they built around that risk.

What This All Means for the Secondaries Market

Three takeaways from this call that matter beyond Carlyle’s own results:

First, GP-led secondaries and structured solutions are becoming a standard tool for top-tier GPs to pre-seed their next flagship fund. The line between fundraising and secondaries strategy is blurring — fast.

Second, the platforms that can offer both liquidity and primary access in a single structure will increasingly win cornerstone capital. Scale and multi-product capability are now table stakes at the top of the market.

Third, Alpinvest’s $107 billion AUM and 20% year-over-year growth signals that institutional and wealth demand for secondaries exposure remains structurally strong — even in a complex macro environment. Carlyle’s management was explicit that they expect to meet or exceed their targets of $200 billion in total inflows and $1.9 billion in FRE by end of 2028, with Alpinvest as a core driver of that growth.

The secondaries market is no longer a niche liquidity solution. At Carlyle, it is the center of gravity.

Sources: Carlyle Q1 2026 Earnings Call transcript, May 7, 2026

| A guest post by

|