Company-Led Secondary Transactions: The New Pillar of Private Market Liquidity

How a once-niche financing tool became a strategic imperative for growth-stage companies.

Source: STIFEL REPORT - MARCH 2026

The private markets are undergoing a quiet but profound transformation. As the path from venture funding to public listing grows longer and more uncertain, a new mechanism has stepped in to fill the gap — the company-led secondary transaction. What was once considered a niche, even stigmatised, corner of private finance has rapidly evolved into a structural pillar of the venture capital ecosystem, standing alongside IPOs and M&A as a mainstream source of liquidity.

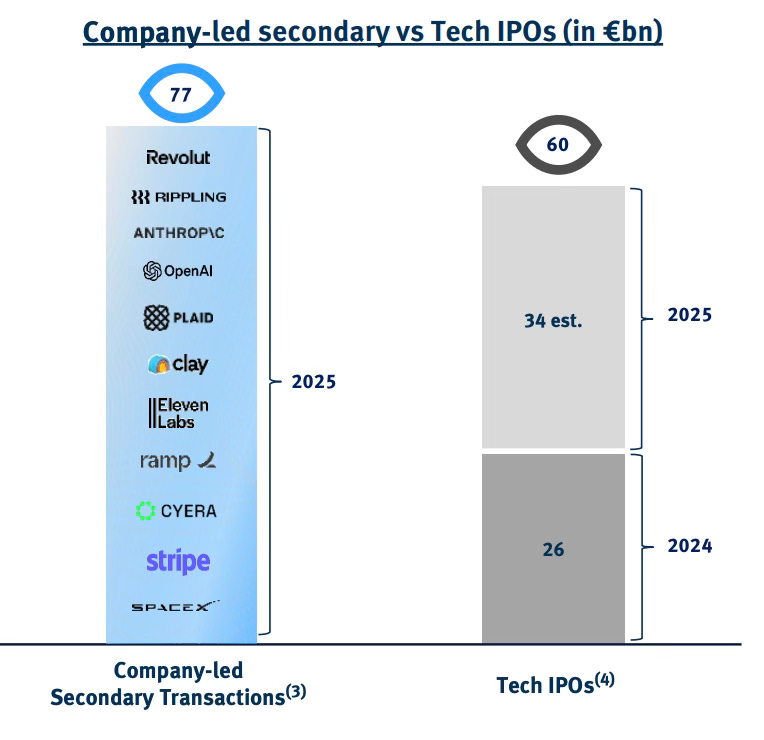

In 2025, company-led secondary transaction volume reached $77bn globally, up from $60bn the prior year — and for the first time, meaningfully surpassing Tech IPO volumes. This is not a temporary aberration. It is the product of deep structural shifts in how companies grow, how talent expects to be rewarded, and how institutional capital seeks exposure to private innovation.

The Problem: Companies Are Staying Private Longer

To understand why company-led secondaries have become so important, one must first understand the environment that created the demand for them.

The median age at IPO during the dot-com era was six to eight years. Today, many of the world’s most valuable private companies have been operating for well over a decade without a public listing. Klarna, which completed its NYSE debut in 2025, had been private for twenty years. Stripe, founded in 2010, has consistently deferred its IPO while conducting regular secondary liquidity events instead. OpenAI, despite being the world’s most valuable startup, remains private with a $500bn valuation.

This is the “Private for Longer” phenomenon — and it is no accident. Record levels of secondary dry powder allow companies to finance research and development and acquisitions via private rounds, strategies once reserved for public companies. Regulatory changes, including the JOBS Act and Accredited Investor Updates in the United States, and the ECSPR and 150-0 B ter frameworks in Europe, have further improved conditions for private companies to remain outside public markets.

The consequence of this extended private lifecycle is significant: a growing population of founders, early employees, and early-stage investors finds itself holding substantial paper wealth with no clear path to liquidity. By the time a company reaches Series D, the average fully-diluted employee option pool can represent 18 to 20% of shares outstanding. That is an enormous amount of value locked away from the people who helped create it.

What Is a Company-Led Secondary Transaction?

A secondary transaction, in the broadest sense, refers to the sale of existing securities among investors after the company’s initial issuance. Unlike a primary offering, the proceeds do not go to the company — they flow directly to the selling shareholders.

A company-led secondary takes this a step further: the company itself facilitates and controls the process, from selecting eligible sellers and buyers to setting the price and managing the timeline. This distinguishes it sharply from informal bilateral trades, where shareholders negotiate directly with buyers without company oversight, often introducing information asymmetry and governance risk.

There are three main formats through which company-led secondaries are conducted:

Tender Offers are the most structured and intensive format. The company or a third-party investor offers to purchase shares at a fixed price, within a defined window, from a pre-approved set of shareholders. The company manages every aspect of the process — pricing, investor selection, disclosure, and legal execution — ensuring transparency, fairness, and narrative control.

Hybrid Rounds combine elements of a primary fundraise with a secondary component. While new capital is raised from investors, a portion of the round is allocated to purchasing existing shares from current shareholders. This allows companies to address liquidity needs without running a separate, standalone process.

Bilateral Transactions are more informal arrangements, where the company facilitates direct trades between shareholders and secondary investors on an at-will basis. While simpler to execute, they carry meaningful risks: information asymmetry, inconsistent pricing, and reduced control over who ends up on the cap table.

Why Tender Offers Have Become the Gold Standard

Among these formats, structured tender offers have emerged as the preferred mechanism for mature growth-stage companies. The reasons are both practical and strategic.

From a seller’s perspective, the fixed price and regulated process provide predictability — critical for institutional investors managing expectations with their own LP base. Transparency is enhanced through formal data rooms and third-party valuation exercises, which in turn attract more sophisticated buyers. And the efficiency of an established legal framework makes for cleaner, faster execution.

For the company, the advantages are arguably even more compelling. Management retains full control over the information released, protecting the company’s narrative at a sensitive moment. Perhaps most importantly, the company can exercise genuine selectivity over who purchases shares — intentionally prioritising long-term strategic investors over opportunistic capital. This is not a trivial benefit. The composition of a cap table can materially affect a company’s trajectory, its governance quality, and its positioning for a future IPO.

The numbers underscore how enthusiastically shareholders have embraced this format. In the first half of 2025, tender offers achieved a median subscription rate — the percentage of eligible shareholders who elect to sell — of 99.9%, a remarkable improvement from the 73.8% rate seen in early 2021. Participation rates among late-stage employees, many of whom have held vested shares for years without an IPO in sight, reached 65.6% at Series C and beyond.

The Mechanics: How a Tender Offer Works

A well-run company-led tender offer typically unfolds over approximately fourteen weeks, structured across five distinct phases.

The process begins with structuring the offer — a two-week phase in which the company and its advisor align on deal metrics, timing, target investor profile, and initial valuation ranges. Equally important at this stage is framing clear guidelines for employees, setting expectations around how much of their vested holdings they will be permitted to sell.

This is followed by preparing the deal, another two-week period focused on solidifying the investor universe, identifying pricing ranges through anchor investor conversations, and crafting a process architecture aligned with the company’s strategic objectives.

The longest phase — five weeks — is devoted to marketing the shares, guiding investors through a structured and competitive diligence process. Finance and legal teams are primed for execution work during this window.

In the late-stage due diligence phase, spanning three weeks, selected investors are pushed toward advanced conversations with management and the board, and key governance terms begin to be negotiated. Finally, book building and closing — the last two weeks — involves matching investor demand with selling shareholder supply and managing the final legal and board approval process.

Share pricing throughout this process follows a rigorous three-step methodology. First, a cap table snapshot and analysis establishes the current ownership structure, share classes, and preference rights. This culminates in an equity waterfall model — a mathematical representation of how value is distributed across shareholders in various exit scenarios. Second, a multi-component valuation study, grounded in board-approved projections and current market conditions, establishes acceptable pricing thresholds. Third, a granular share class pricing model applies industry-standard methodologies in conjunction with proprietary equity waterfall analysis to price each class of shares individually.

A Fundamental Shift in How Pricing Works

One of the most significant developments in the secondary market has been the evolution of pricing discipline. For much of the market’s early history, secondary valuations were anchored to the last primary round — shares were simply sold at a discount to the most recent mark. This approach is no longer adequate or accurate.

Pricing in today’s secondary market has bifurcated sharply based on a company’s last financing vintage. Companies that raised primary capital during the peak years of 2020 to 2022 are now facing median secondary discounts ranging from 33.6% to 61.5% — a steep repricing that reflects the market’s correction of valuations set at elevated multiples during the pandemic-era boom. By contrast, companies that successfully raised a primary round in 2024 or 2025 are trading at near-par, with median discounts of just 0% to 8.5%.

The direction of travel here is significant: it signals a healthy market stabilisation in which strong fundamentals and recent operating performance command a genuine premium. As one market participant put it, pricing must be grounded in fundamentals rather than anchored to outdated primary rounds, with a scenario-based approach — balancing downside protection with credible upside — now a standard expectation from sophisticated buyers.

This shift is also reflected in how volume is distributed across company stages. In the first half of 2025, late-stage deals at Series C and beyond represented 61.2% of total tender offer volume, up from just 19.8% in 2021. The secondary market has matured from a relief valve for early-stage investors into a quasi-public liquidity mechanism for some of the world’s most advanced private companies.

The Strategic Case: Why CFOs Are Embracing Secondaries

For growth-stage CFOs, managing a heterogeneous cap table has become one of the most consequential and demanding aspects of the role. By the time a company reaches late stage, the cap table typically includes early employees seeking liquidity to finance personal expenses, founders with a disproportionate share of their net worth tied up in illiquid stock, seed and early-stage VC funds relying on distributions to serve their LP base, family offices with flexible but distinct timelines, growth and private equity funds expecting ambitious outcomes and carrying significant governance protections, and in many cases, investors from the 2021 and 2022 vintage who may be averse to realising a loss.

Managing this constellation of incentives — while staying focused on executing business strategy — is an overwhelming undertaking. Company-led secondary programmes offer CFOs a structured mechanism to address these pressures proactively.

The benefits are multiple. Cycling out disaffected early-stage investors simplifies the cap table, reduces governance friction, and protects future IPO pricing from the downward pressure that can arise when locked-up shareholders rush to sell the moment a post-IPO restriction period expires. Structured tender offers also allow companies to attract new cornerstone investors who bring strategic value, industry expertise, and long-term capital — partners who can enhance credibility with financial markets ahead of a public offering.

And there is the talent dimension, which may be the most urgent consideration of all. In an era of fierce competition for top technical and operational talent, publicly-listed companies can offer liquid equity as part of compensation packages. Private companies that cannot offer any pathway to liquidity are at a structural disadvantage. Recurring secondary liquidity programmes — like those institutionalised by SpaceX, Stripe, Revolut, and OpenAI — are increasingly viewed not as perks but as essential retention and alignment mechanisms.

OpenAI and Stripe: Case Studies in Secondary Strategy

Two recent examples illustrate how sophisticated companies are deploying secondary programmes strategically.

OpenAI’s 2025 liquidity programme was driven as much by retention urgency as by capital need. By July 2025, Pitchbook analysis had identified that over 25% of key research and leadership staff had departed within two years, creating acute pressure for a liquidity event to compete with the compensation packages of publicly-listed rivals. By October, OpenAI had closed a $6.6bn tender offer — out of $10.3bn authorised — at a $500bn valuation, led by SoftBank Group, Thrive Capital, and Dragoneer Investment Group. The outcome was dual: it solidified OpenAI’s status as the world’s most valuable startup while resetting the retention baseline by delivering tangible liquidity to long-term employees.

Stripe’s journey is equally instructive. After executing a $6.5bn Series I raise in March 2023 at a $50bn valuation — nearly 50% below its 2021 peak of $95bn — Stripe steadily rebuilt its secondary valuation through disciplined fundamentals and systematic liquidity management. By March 2025, it finalised a broad-based tender offer at $91.5bn, nearly recovering its previous high-water mark. By February 2026, Stripe had closed a further secondary round at $159bn — a remarkable demonstration of how a well-managed private company can use secondary markets to both reward shareholders and signal value, without ever needing to go public.

Institutional Capital Transforms the Buyer Landscape

The rapid growth of company-led secondaries has been matched by an equally rapid evolution on the buy side. The secondary buyer universe now spans four broad categories of investor.

Growth and crossover funds use direct secondaries to increase their positioning in portfolio companies or secure access to top-tier assets at attractive entry points, often using secondary positions as a bridge to future primary rounds or IPOs. Family offices have established themselves as active liquidity providers, scaling exposure as the market becomes more structured. Pension funds and sovereign wealth vehicles — including institutions such as ADIA, GIC, Temasek, and Mubadala — participate in the largest and most well-scaled company-led rounds. And a rapidly growing cohort of dedicated secondary funds and strategies, ranging from pure direct secondaries vehicles to global institutional allocators with specialist venture programmes, provide flexible capital across a wide range of deal sizes and structures.

The entry of the world’s largest asset managers has been particularly significant. Goldman Sachs’ acquisition of Industry Ventures — a specialist with $7bn in assets under management and 25 years of industry history — represented a watershed moment, signalling that secondaries have become a necessary entry point into the innovation economy. BlackRock has filed for a dedicated venture secondaries fund. Morgan Stanley, via EquityZen, and Charles Schwab, via Forge Global, have acquired the distribution infrastructure to channel accredited and retail investor capital into the asset class. Dedicated US VC secondary dry powder has nearly doubled since 2022, reaching $6.4bn in 2024.

The Road Ahead

The structural forces driving the growth of company-led secondaries show no signs of abating. Traditional exit windows, while recovering, remain top-heavy. Headline IPOs like Klarna’s $17bn NYSE debut, Figma’s $56bn listing, and Coreweave’s $19bn valuation signal resurgent institutional interest — but deal counts remain well below peak levels, and the backlog of excellent private companies with IPO ambitions continues to grow.

In this environment, secondary liquidity is no longer a stopgap. It is a permanent feature of the private market landscape — a governance tool, a talent strategy, a cap table management mechanism, and an institutional asset class in its own right. The historical stigma that once attached to partial liquidity for founders and employees has been replaced by a recognition that structured secondary programmes are a sign of organisational maturity, not distress.

For any late-stage private technology company, the question is no longer whether to offer secondary liquidity, but how to do it well. The answer, increasingly, is through company-led, advisor-facilitated tender offers — structured, transparent, and strategically disciplined processes that align the interests of employees, early investors, management, and the long-term shareholders who will carry the company toward its ultimate exit.

Data and insights sourced from Stifel’s Company-Led Secondaries Report, March 2026.