Continuation Vehicles Don't Need a Distressed Market Anymore. LPs Just Said So.

Exit conditions will improve. CV volume will keep growing anyway. That's the structural shift hiding in plain sight in Coller Capital's Summer 2026 Barometer.

For years, the critique of continuation vehicles was straightforward: they’re a workaround. When exit markets close, GPs manufacture liquidity through CVs rather than returning capital. When IPO windows reopen and M&A recovers, the volume will normalize. The implication was that CV activity was cyclical — a symptom of a difficult market, not a permanent feature of how private equity operates.

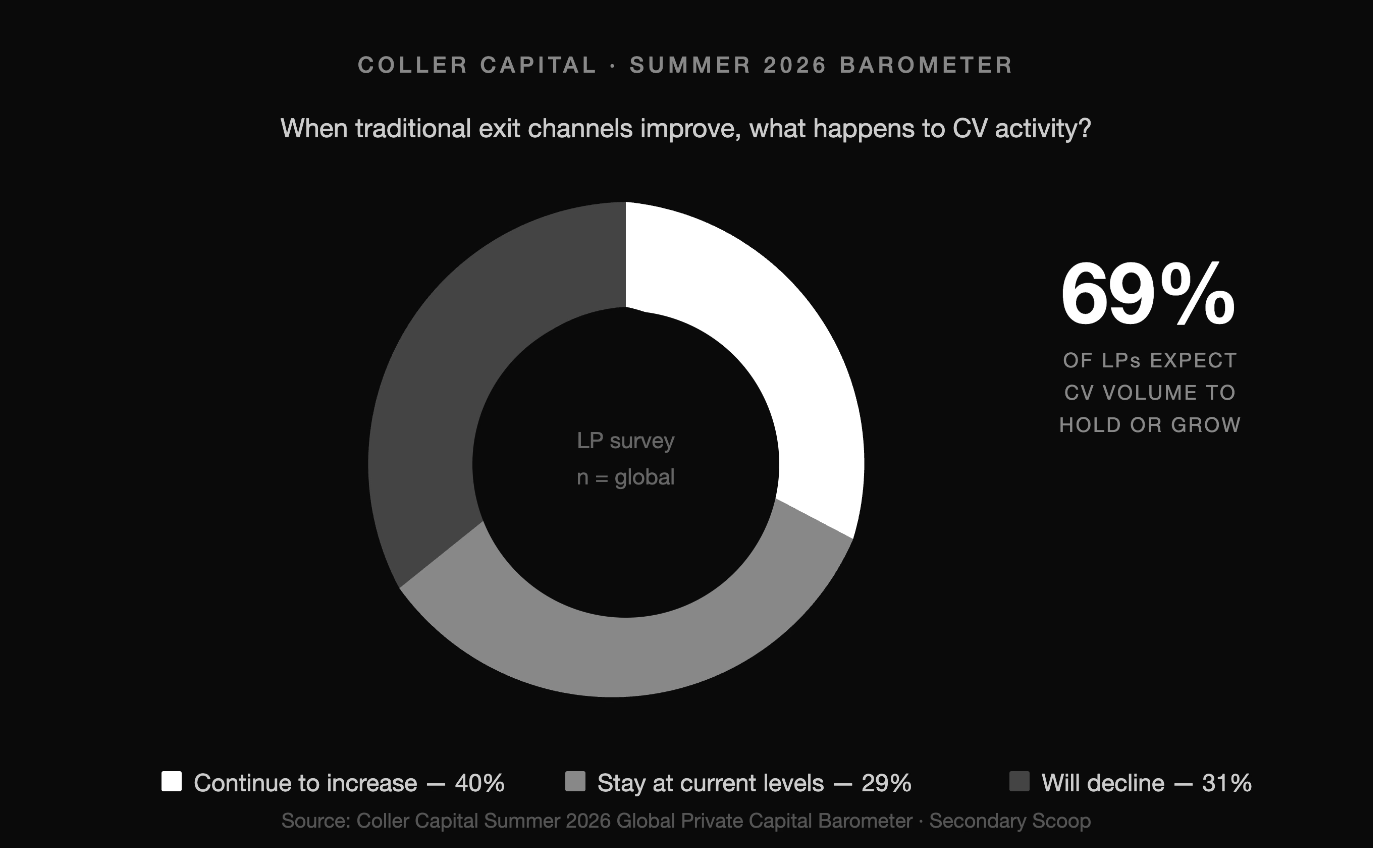

Coller Capital’s Summer 2026 Global Private Capital Barometer offers the clearest LP-level rebuttal of that argument to date. When asked what happens to CV activity when traditional exit channels improve, 40% of LPs said it will continue to increase. Another 29% expect it to stay at current levels. Just 31% anticipate a decline.

That means 69% of LPs expect CV volume to hold or grow regardless of exit conditions. The cyclical thesis is effectively dead.

Why the exit timing gap makes CVs permanent

The structural case for CVs doesn’t rest on market dysfunction. It rests on a more fundamental problem: LPs and GPs have different clocks.

The Barometer makes this tension quantifiable. When asked whether GPs are correctly balancing liquidity needs against portfolio company value creation, only 40% of LPs said the balance is about right. Thirty-nine percent said GPs are not providing liquidity early enough. A further 22% said the best companies are being sold too soon.

Read those numbers carefully. Sixty percent of LPs are dissatisfied with exit timing — but they’re dissatisfied in opposite directions. Nearly two-fifths want liquidity faster. More than a fifth want GPs to hold longer. That’s not a problem with a single solution. That’s a structurally heterogeneous LP base with irreconcilable holding period preferences sitting inside the same fund.

Continuation vehicles are the mechanism that resolves this. By offering LPs the choice of selling for liquidity or rolling to retain exposure, CVs allow a single GP decision — hold the asset — to accommodate both outcomes simultaneously. An LP that needs DPI can exit. An LP that believes in the remaining value creation story can roll. Neither has to override the other.

That logic doesn’t disappear when exit markets improve. If anything, it becomes more relevant when GPs have genuine optionality — when the choice to run a CV reflects conviction about an asset’s trajectory rather than an inability to find a buyer elsewhere.

The normalization of CV acceptance

What’s changed in LP sentiment is not just tolerance for CVs but active expectation of them as a portfolio management tool. The Barometer describes CVs as having “gained acceptance among LPs as an established feature of private markets.” That language matters. Established feature is meaningfully different from necessary evil.

This shift has been gradual but consistent. Early CV transactions — particularly single-asset vehicles in the 2018–2020 period — faced significant LP skepticism around conflicts of interest, valuation integrity, and GP motivations. ILPA guidance, increased use of independent advisors, and more standardized process norms around fairness opinions have progressively addressed those concerns. LPs are better equipped to evaluate CV terms than they were five years ago, and the market infrastructure around these transactions has matured accordingly.

The result is a cohort of LPs who are no longer reacting to CVs defensively but incorporating them into their portfolio planning. When 40% of your LP base expects CV activity to keep growing in a recovered exit environment, you’re no longer looking at a crisis instrument. You’re looking at standard toolkit.

What this means for secondary market structure

The permanence of CV activity has direct implications for how the secondary market develops over the next cycle.

GP-led volume — of which single-asset and multi-asset CVs are the dominant form — has grown from a marginal share of secondary transaction volume to roughly half of total market activity over the past several years. If LP sentiment in the Barometer is directionally correct, that share is unlikely to compress back toward historical norms even as LP-led volume also grows.

That has consequences for secondary fund positioning. Buyers that built capabilities specifically around GP-led transactions during the 2019–2023 buildout are not holding a cyclical skill set. They’re holding infrastructure for a permanent market segment. Conversely, traditional LP-led focused buyers face a secondary market where their historical edge — portfolio pricing, relationship-driven sourcing — is a smaller proportion of available deal flow than it once was.

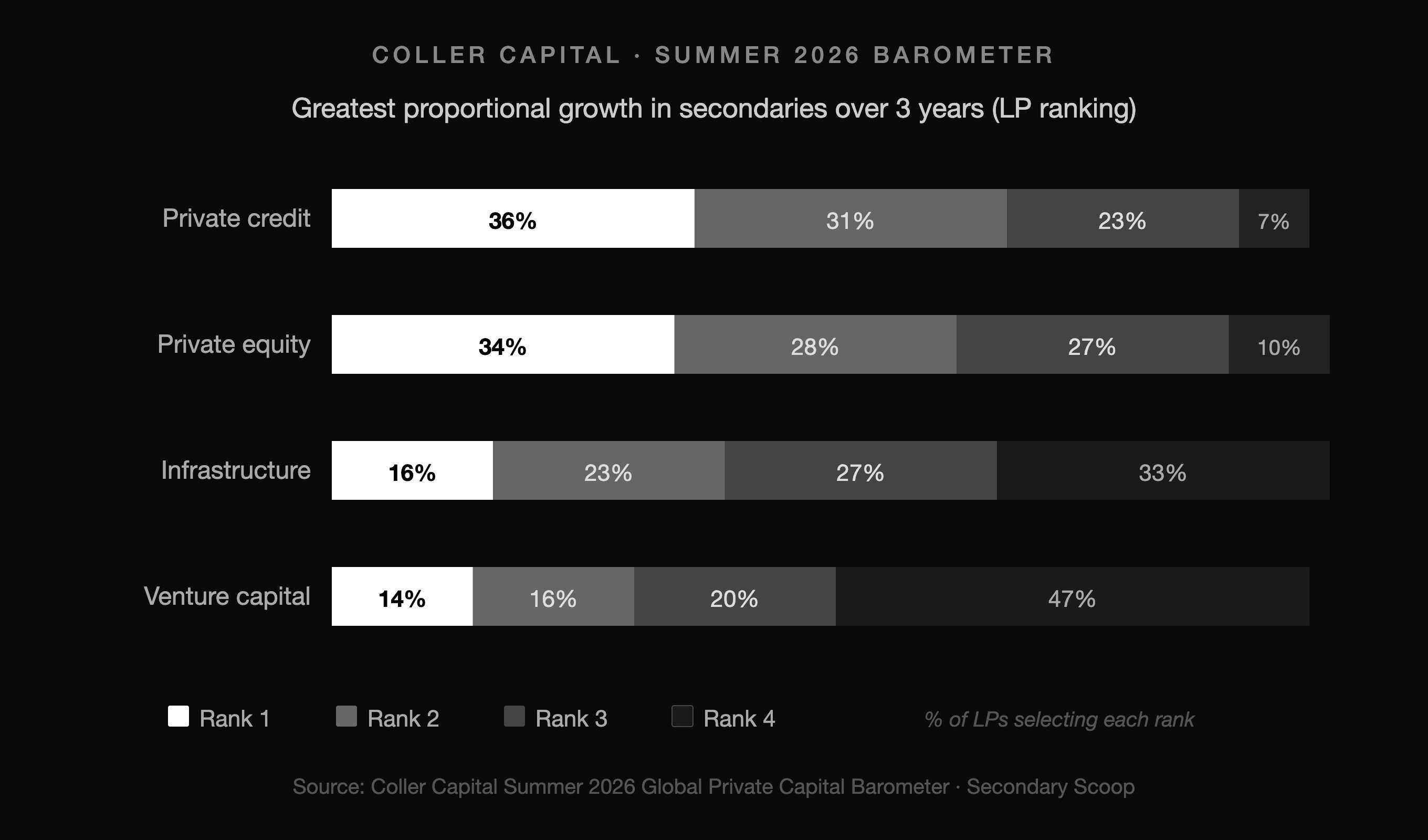

The Barometer also flags private credit secondaries as the asset class LPs expect to see the greatest proportional growth in the secondary market over the next three years, ahead of private equity. If CV structures migrate into private credit at scale — which the growth of NAV lending and credit fund continuation structures suggests is already beginning — the GP-led market expands further beyond its buyout origins.

The thesis, restated

The argument that CV volume is a distressed-market phenomenon has always been partly wrong. It conflated the conditions that accelerated CV adoption — a closed exit environment from 2022 through much of 2024 — with the underlying structural driver, which is the mismatch between LP holding period heterogeneity and traditional closed-end fund structures.

Coller’s Barometer is the first major LP sentiment survey to capture this distinction cleanly in the data. When 69% of LPs expect CV activity to hold or grow in a recovered market, they’re not describing a temporary accommodation. They’re describing a permanent repricing of how GP-LP relationships manage the end of the investment period.

The cycle argument for CVs is over. The structural argument is just getting started.

Source: Coller Capital Global Private Capital Barometer, Summer 2026 (44th Edition). Survey conducted February 18 – April 21, 2026, across 108 LPs overseeing $2.045 trillion in AUM. Editorial note: Coller Capital is a secondary fund manager with $54 billion in AUM and a direct commercial interest in secondary market growth. Data points are sourced directly from the report; structural interpretations are Secondary Scoop’s editorial framing.