Credit Takes the Podium: Secondary Scoop's H1 2026 Continuation Vehicle and Fundraising Balance

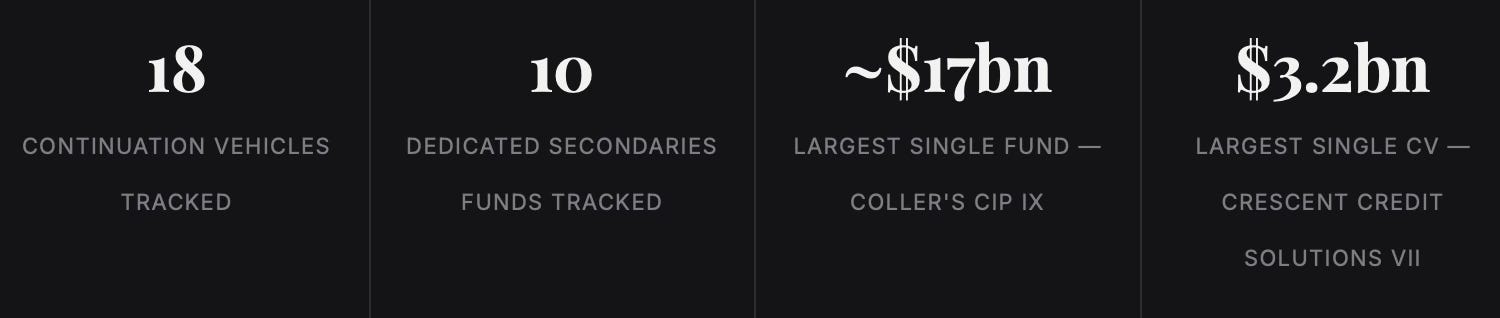

Eighteen continuation vehicles, ten dedicated secondaries funds and four LP-led portfolio sales, tracked across Europe and the rest of the world through open sources in the first six months of 2026.

Six months into 2026, the continuation vehicle is no longer only a buyout story with a credit footnote. Of the CVs we tracked, the two largest by disclosed size were both private credit vehicles: Crescent Capital's $3.2 billion Credit Solutions VII and Arcmont's $2.5 billion Direct Lending Fund III CV, and credit vehicles make up four of the seven largest CVs overall. On the fundraising side, the single largest dedicated secondaries fund of the half was a generalist, not a credit specialist: Coller Capital's $17 billion CIP IX. But the largest credit-*dedicated* fund, Ares's $7.1 billion Credit Secondaries Fund, was itself larger than every other fund we tracked bar Coller's flagship. Credit secondaries haven't overtaken buyout. They have, for the first time in this data, stopped looking like its junior partner.

This is our first structured pass at a H1 2026 balance: eighteen continuation vehicles (eight in Europe, ten across the rest of the world), ten dedicated secondaries funds (two European, eight elsewhere), and four LP-led portfolio sales (one European-asset, three elsewhere), compiled deal-by-deal from primary sources, law firm announcements and trade press, then cross-checked against major buyers’ own disclosures. It is not exhaustive, Secondaries Investor’s own paywalled Q1 log alone counted 27 CV closes in the first three months of the year, but it is verifiable, and it is enough to draw some lines.

Credit’s coming-out half

Start with the vehicles themselves. In Europe, Arcmont Asset Management’s $2.5 billion credit continuation vehicle, backed by Ares Credit Secondaries and closed in April, was billed by its own advisers as the largest European credit CV to date. In the U.S., Crescent Capital Group’s $3.2 billion Credit Solutions VII, led by Pantheon with Allianz Global Investors co-leading, went one better, and was marketed as the largest private credit CV of any kind to date. Antares Capital closed its second Ares-led credit CV at $1.7 billion in March. Audax Private Debt closed a $1 billion direct-lending CV with Pantheon in May. Coller Capital itself led a $1.3 billion credit CV on Ares’s 2018-vintage U.S. Direct Lending fund in February.

Add it up and disclosed credit CVs outsized disclosed equity CVs in both regions this half. That is not a rounding error. It is the clearest evidence yet that the credit secondaries market, long treated as PE’s smaller, quieter cousin, has caught up on deal size within the space of about eighteen months.

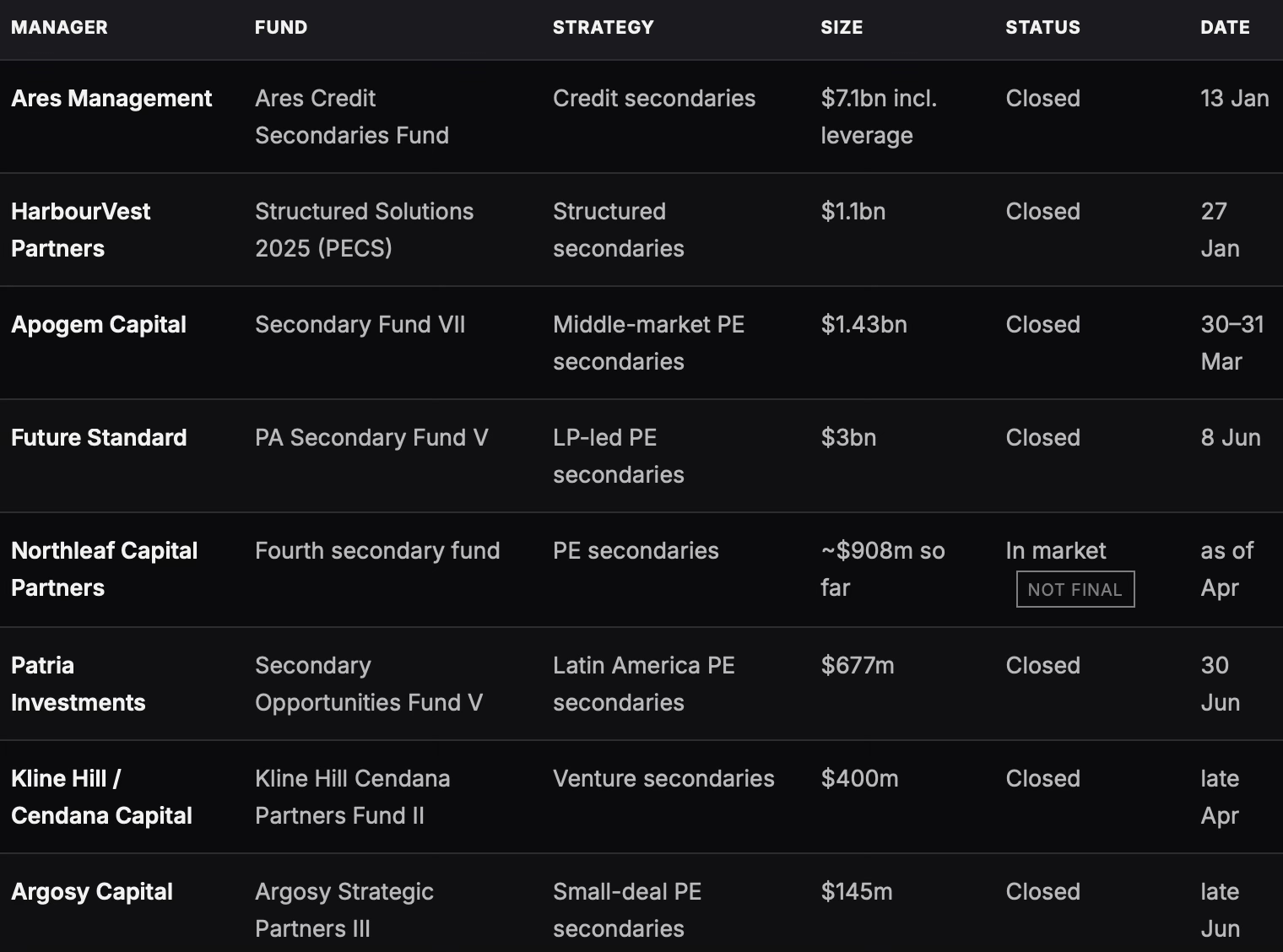

The fundraising data tells the same story from the buy side. Ares Management’s inaugural Ares Credit Secondaries Fund closed at $7.1 billion including leverage in January, which Ares describes as the largest dedicated institutional credit secondaries fund globally by LP equity commitments. That is larger than every other dedicated secondaries fund we tracked this half except Coller’s flagship.

Credit secondaries used to be the vehicle you built once you’d exhausted the equity playbook. In H1 2026, credit CVs are outsizing the equity deals in the same league tables.

EUROPE’S CONTINUATION VEHICLES, H1 2026

REST OF WORLD CONTINUATION VEHICLES, H1 2026

Europe’s paradox: deep deal flow, shallow fundraising

Flip to the buy side and Europe looks almost inverted. Eight CVs closed or landed in the market across Spain, the U.K., France, Switzerland, the Nordics and Germany this half, a genuinely diversified spread by geography and sector, from frozen dough in Catalonia to UPS manufacturing on the Swiss border to childcare in the U.K. But only two dedicated European secondaries funds registered any real fundraising milestone in the same window, and one of those, CVC Secondary Partners’ Secondary Opportunities Fund VI, had not even reached final close as of its Q1 update, sitting at $8.7 billion against a $7 billion target, with the close pushed into the second half.

The other is Coller Capital’s Coller International Partners IX, which closed at $17 billion in January, the firm’s largest fund ever and, on the numbers we tracked, the largest single vehicle of any kind raised in H1 2026, CV or fund, anywhere. One number does a lot of work here: Coller alone raised roughly as much in six months as the entire rest-of-world fund cohort we tracked combined.

READING THE GAP

Europe’s thin fund count is not necessarily a demand problem — it is a base-rate one. Flagship secondaries funds are raised every two to four years, and the region’s major platforms (Ardian’s ASF IX, AlpInvest’s ASP VIII) both closed their current vintages in 2025 or earlier, just outside this window. What the eight-CV, two-fund split actually shows is that deal flow and fund cycles move on different clocks — and in H1 2026, Europe’s clock for deals was ticking a good deal faster than its clock for capital formation.

EUROPE: DEDICATED SECONDARIES FUNDS, H1 2026

REST OF WORLD: DEDICATED SECONDARIES FUNDS, H1 2026

The buyer base is quietly getting wider

The most interesting story in the fund data may be the one furthest from the headline numbers. Alongside the usual megafunds, H1 2026 produced three closes that would barely have registered five years ago: Patria Investments’ $677 million fifth secondaries fund, dedicated entirely to Latin America; Kline Hill Partners and Cendana Capital’s $400 million second fund, built specifically for seed-stage venture LP stakes; and Argosy Capital’s $145 million Strategic Partners III, which writes cheques as small as $100,000 into small-deal secondaries that larger platforms don’t bother chasing.

None of these will move the league tables. All three matter for the same reason: they show the secondaries toolkit, LP stake sales, GP-leds, structured liquidity, being adapted to markets and check sizes that the Collers and Ardians of the world were never built to serve. Latin America, seed-stage venture and sub-$10 million deals are not adjacent markets discovering secondaries for the first time; they are proof that the mechanism has become generic enough to travel.

WHAT’S STILL IN THE PIPELINE

Two of the largest processes we tracked in Europe hadn’t closed by 30 June. CapVest’s roughly $3.8 billion continuation vehicle for radiopharmaceuticals group Curium was announced in November 2025 and guided to a Q1 2026 close, but no confirmed completion had surfaced in open sources by our cutoff. Ardian, meanwhile, was reportedly preparing teasers as of April for a continuation fund on its stake in German utility EWE — sized at “well above €1 billion” and, if it proceeds, one of Ardian’s first infrastructure CVs. Both are strong candidates for the top of an H2 2026 list.

The other side of the ledger: LPs cash out

CVs and dedicated funds are the buy-side and sponsor-side of the secondaries trade. The seller side, LPs choosing to sell fund stakes rather than wait for a distribution, had its own H1 2026, and it was smaller and messier to track than either of the above, precisely because so many of the largest processes were still in the market rather than closed.

The cleanest data point is also the most American: CalPERS closed a $2.3–3 billion LP-led portfolio sale in early February, with Lexington Partners and Partners Group among the buyers, continuing a run of sales the pension giant has made a habit of since adopting a total portfolio approach. The University of California followed in March, shopping a $3 billion LP portfolio of its own, still in the market as of our cutoff. Singapore’s GIC has reportedly been testing appetite since October 2025 for a sale of up to $1–3 billion across roughly 30 fund positions, mostly 2016-vintage Blackstone, Apollo and TDR Capital commitments; no confirmed 2026 close had surfaced by 30 June.

Europe’s clearest entry is an odd one: CPP Investments, a Canadian pension giant, agreeing in May to sell its remaining interests in a European non-performing loan portfolio to a joint venture between Arrow Global and Fortress Investment Group for roughly C$1 billion. It is a reminder that “European secondaries” increasingly means European assets changing hands between non-European institutions as often as it means European sellers, and that credit and real-asset secondaries are broadening the definition of what counts as an LP sale in the first place.

WHY THIS TABLE IS THINNER THAN THE OTHER FOUR

LP portfolio sales are structurally harder to track in real time than CVs or fund closes: sellers rarely issue press releases, buyers are contractually discouraged from confirming pricing, and “the process is in market” can describe anything from a live auction to a shelved plan. Yale’s widely reported exploration of a sale of up to $6 billion in PE and venture stakes, and Harvard’s parallel look at roughly $1 billion, both appear to have narrowed in scope over 2025 and had not been confirmed as closed transactions within this window, so neither appears in the table below. We would rather under-report a category than print a rumor as a fact.

EUROPE (ASSET-FOCUS): LP-LED SECONDARIES TRANSACTIONS, H1 2026

REST OF WORLD: LP-LED SECONDARIES TRANSACTIONS, H1 2026

The house view

Put the five tables side by side and H1 2026 reads less like a single trend than three running in parallel. Credit secondaries, both the vehicles and the funds that buy into them, have grown from a subplot into a competing storyline, with the single largest CV (Crescent, $3.2bn) and the single largest dedicated fund apart from Coller’s flagship (Ares, $7.1bn) both credit plays. Europe’s deal pipeline is wide and increasingly varied by sector, even as its fund-formation calendar sits mostly idle until the region’s next vintage cycle turns over. And underneath both of those stories, a longer tail of specialist buyers: regional, strategy-specific, deliberately small, is proving that the continuation vehicle is no longer a mega-cap phenomenon looking for smaller imitators. Meanwhile the sell side shows the mirror image: it is the giant, generalist LPs: CalPERS, the University of California, GIC, doing the confirmed selling this half, even as the market talks endlessly about endowments. It is infrastructure now, and infrastructure gets used by whoever needs it, on both sides of the trade.

That is consistent with where this publication has stood since its first issue: secondaries are a portfolio management tool, not a distress signal. H1 2026’s numbers are the clearest evidence yet that the market agrees.

DISCLOSURE: WHAT THIS BALANCE IS, AND ISN’T

This is a compilation from open sources — press releases, law firm and adviser announcements, and trade coverage — not a subscription-grade transaction log. We are confident in every deal listed, but we are not confident the lists are complete. Operations that were never announced, announced only in outlets we don’t cover, or disclosed solely to subscription services (Secondaries Investor’s own Q1 2026 CV log alone counted 27 closes against the eight we have for Europe in the same period) will be underrepresented here, particularly in private-credit CVs, small-cheque and regional secondaries funds, and LP sales that never went to press. Treat the totals below as a floor, not a ceiling. If you know of an operation we’ve missed, we want to hear about it.

METHODOLOGY

Continuation vehicles, dedicated secondaries funds and LP-led portfolio sales were identified through primary press releases, law firm and adviser announcements, and trade coverage (Secondaries Investor, PE Hub, AltAssets, Alternative Credit Investor, Bloomberg and others), then classified by sponsor/target geography for CVs, by manager headquarters for funds, and by underlying asset geography (noted where it differs from seller domicile) for LP sales. Deals are included where a launch, interim close or final close fell within 1 January–30 June 2026; two European CVs (CapVest/Curium, Ardian/EWE), two funds (CVC’s SOF VI, Northleaf’s fourth vehicle) and two LP sales (University of California, GIC) are flagged as not yet finally closed or confirmed as of this writing. This dataset is a verified sample, not a census: Secondaries Investor’s own subscription-gated Q1 2026 CV Deal Log alone counted 27 closes in the first quarter. No confirmed, named Asia-Pacific or Middle East continuation vehicle or dedicated secondaries fund close was identified in open sources for this period, and reported endowment sale processes (Yale, Harvard) were excluded as unconfirmed within the window.

Sources: Ardian, Coller Capital, CVC Capital Partners, Ares Management, Arcmont Asset Management, Crescent Capital Group, Antares Capital, Audax Private Debt, Cerberus Capital Management, Onex Partners, Align Capital Partners, Partners Group, Avenue Capital Group, HarbourVest Partners, Apogem Capital, Future Standard, Northleaf Capital Partners, Patria Investments, Kline Hill Partners, Argosy Capital, Fremman Capital, Latour Capital, MCH Private Equity, Eurazeo, Verdane, CapVest Partners, CPP Investments, CalPERS, University of California, GIC; Secondaries Investor, PE Hub, AltAssets, Alternative Credit Investor, Alternatives Watch, Bloomberg, ION Analytics (Infralogic, Mergermarket), Global SWF, DealStreetAsia, Kirkland & Ellis, Goodwin, Hogan Lovells, Davis Polk.