Decoding Secondary Returns Beyond Discount: Abbott's Five-Factor Framework for LP Diligence

Abbott Capital just quantified what the market has long argued informally: discount doesn't drive secondary outperformance, value appreciation does. Here's what the numbers mean for manager diligence.

Abbott Capital’s latest research note doesn’t break new conceptual ground for anyone who has spent time underwriting secondary transactions. What it does is put numbers to intuitions the market has mostly traded in qualitative form, and in doing so, it hands LPs a diligence framework that’s more useful than most of what circulates as “secondaries education” today.

The paper isolates five factors that determine the risk-return profile of any given secondary transaction and the MOIC and IRR ultimately reported to investors: value appreciation of the underlying assets, diversification, valuation and discount at entry, transaction-level leverage, and how cash flow recycling is accounted for. None of these are new vocabulary to anyone in the market. What’s useful is Abbott’s attempt to isolate and size each one, because in practice, most reported secondary returns blend all five into a single headline number, and that number tells an LP almost nothing about where the return actually came from.

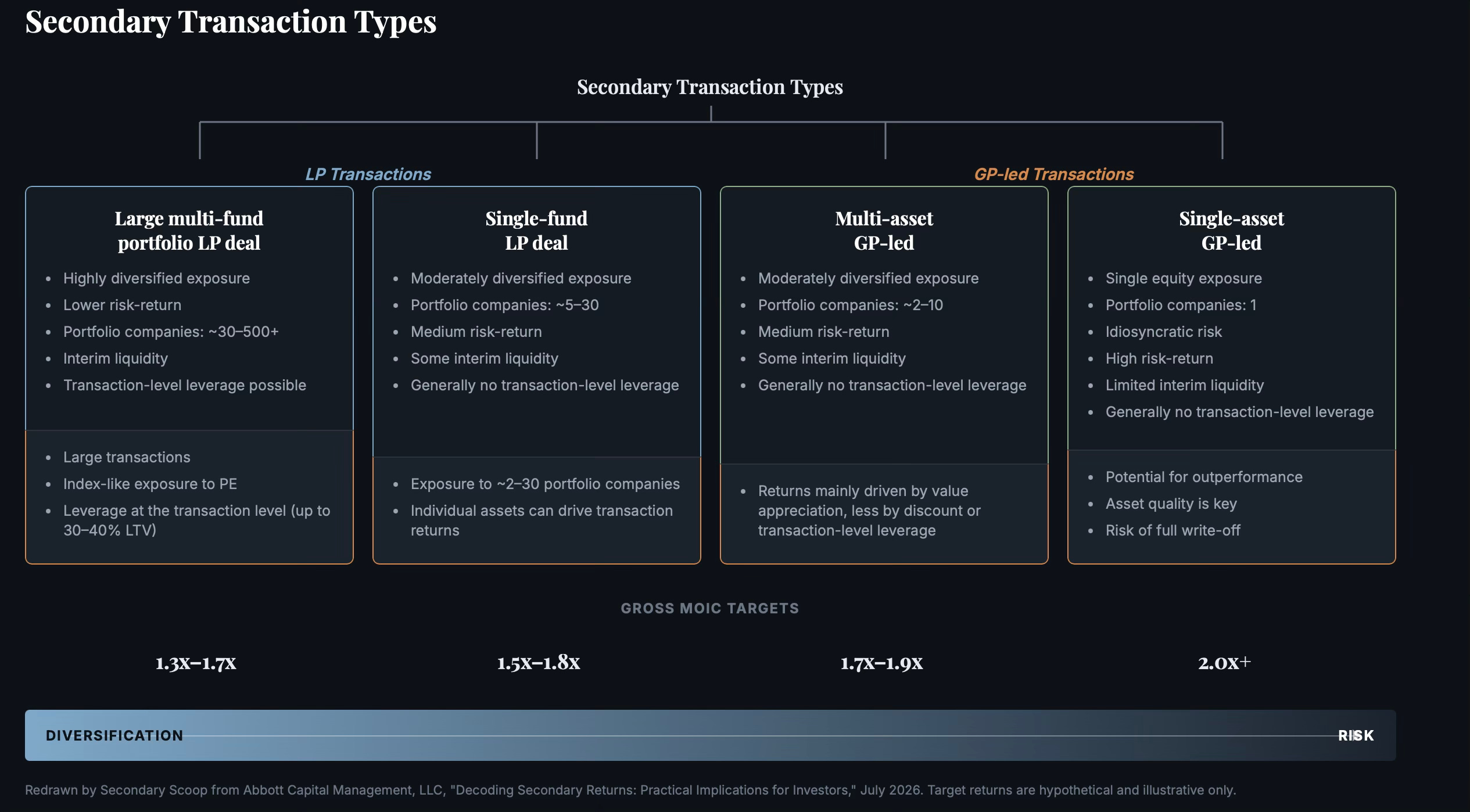

The transaction-type spectrum isn’t optional context. It’s the starting point

Abbott’s framing starts from the observation that the secondaries market has stopped being one strategy. Diversification level now functions as the primary axis separating four distinct transaction archetypes, each underwritten to a different return target on an unlevered basis.

This is a useful quantified check on a framing that still shows up often: treating "secondaries" as one homogenous strategy with a single risk-return signature. A large diversified LP portfolio at 30-40% loan-to-value and a single-asset GP-led continuation vehicle are not the same asset class wearing different clothes. They sit at opposite ends of a genuine risk spectrum, and conflating them makes it harder for LPs to build a coherent secondaries allocation policy.

DIVERSIFICATION, DECODED

Abbott also takes a position on a question that gets less airtime: is there such a thing as over-diversification? Citing Modern Portfolio Theory’s observation that the marginal benefit of diversification tapers meaningfully past 20–30 positions, the paper argues that a secondary portfolio spanning hundreds of underlying companies may reduce idiosyncratic risk to near zero, but at the cost of any ability to outperform. If your portfolio mirrors the index, you get index returns. That’s a useful discipline check for LPs evaluating whether a manager’s “diversified” pitch is actually a return thesis or a risk-avoidance thesis dressed up as one.

The discount is doing less work than the market thinks

“A buyer transacting at a 10% discount can report a 53.3% IRR after one quarter, purely from the mark-up to NAV. By month 18, that same discount-driven IRR has collapsed to 7.3%” , Abbott Capital, “Decoding Secondary Returns,” July 2026

This directly quantifies a distortion that shows up constantly in how secondary transactions get marketed in their first year of life. Buy at a discount to NAV, mark the position back up to the GP’s reported NAV post-close, and the unrealized IRR in month one looks spectacular, not because value was created, but because of an accounting mechanic. Abbott’s decay curve shows that effect evaporating almost entirely within six quarters, which is a useful number to have on hand the next time a placement deck leads with a triple-digit early-stage IRR.

More importantly, Abbott runs the long-horizon comparison LPs actually care about: holding value appreciation constant at a 1.60x MOIC, moving from par pricing to a 10% discount only lifts the outcome to 1.78x MOIC and from 16.9% to 21.1% IRR. Discount matters, and it isn’t nothing, but across the life of the deal, it’s a secondary contributor sitting well behind the appreciation of the underlying companies themselves. That’s a materially different message than the “buy cheap, win big” pitch that still circulates in generalist coverage of the asset class, and it’s the strongest piece of quantitative support yet for the view that secondaries are a portfolio construction tool built on genuine value creation, not a distressed-asset bargain hunt.

What leverage actually does, and how fast it unwinds

The leverage section is the one GPs pitching levered secondary vehicles should expect LPs to start asking about directly. Abbott’s illustrative $500 million NAV portfolio, financed at 40% LTV with a cash-sweep amortization structure, lifts the unlevered base case from 1.60x/16.9% IRR to 1.94x/19.7% IRR. That’s a real uplift. But the paper’s distribution-delay sensitivity is the part worth sitting with: a three-year lag in distributions relative to the base case brings the levered MOIC down to 1.62x, barely above the unlevered 1.56x, and the entire benefit of the leverage has essentially disappeared under the weight of accruing interest and a slower-amortizing loan balance.

WHY THIS MATTERS FOR TRACK-RECORD COMPARABILITY

Gross vs. net of recycling — Abbott’s worked example shows the same $100 million transaction reporting a 1.48x MOIC under the traditional ILPA gross method versus 1.60x when cash flow offsets are netted out. Same deal, same cash flows, two different headline multiples.

DPI diverges too — under gross accounting, DPI runs slightly ahead in the early years; under net accounting, it eventually overtakes and finishes higher as the multiple converges toward final MOIC.

The practical implication — an LP comparing two managers’ track records without confirming which convention each one uses is, in effect, comparing two different measurement systems and calling it apples-to-apples.

This recycling section is understated in the paper but may be the most operationally relevant finding for LPs doing manager selection. A 12-point MOIC gap (1.48x vs. 1.60x) purely from a reporting convention, on an identical underlying cash flow profile, is large enough to change a manager ranking. It’s a reminder that “MOIC” and “IRR” are not standardized enough terms to take at face value in a diligence process — the fine print on methodology deserves the same scrutiny as the fine print on fees.

About Abbott Capital Management

Abbott Capital Management, LLC is an independent investment adviser founded in 1986, specializing in the creation and management of private equity investment programs across private equity, growth equity, and venture capital. Since inception, the firm has committed more than $29 billion to over 850 primary, secondary, and co-investment transactions on behalf of its clients, a global investor base spanning public, corporate, and multi-employer pension funds, foundations, endowments, family offices, and high-net-worth individuals.

Abbott’s Secondary Investments team, led by Managing Director Wolf Witt alongside Vice President Declan Feeley and Senior Associate Alexis Maida, focuses on acquiring and analyzing secondary transactions across the full risk-return spectrum, from large, diversified multi-fund LP portfolios to concentrated single-asset GP-led continuation vehicles. As a fund-of-funds investor with its own capital allocated across the asset class.