European continuation vehicles entered 2026 not as a novelty, but as a standard instrument in the private capital toolkit. Invest Europe’s annual activity report — published May 2026 and based on data from over 1,140 European fund managers — dedicated a standalone section to continuation funds for the first time in its history. The data is unambiguous: CV fundraising across Europe reached €19.8 billion in 2025, up 113% from €9.3 billion in 2024. Investment by continuation funds doubled to €9.9 billion across 69 portfolio companies. And most strikingly, continuation funds captured 24% of the total value of PE-to-PE exit transactions in 2025 — up from just 8% the prior year — confirming that CVs have crossed the threshold from tactical tool to structural exit route.

H1 2026 builds directly on that momentum. The deals tracked by Secondary Scoop between January and May 2026 span four distinct asset classes — infrastructure, private credit, growth buyout and mid-market buyout — with disclosed sizes ranging from €155 million to €2.2 billion. What they share is the structural logic: a GP unwilling or unable to force an exit at a suboptimal moment, a high-conviction asset with further runway, and a secondary market with sufficient capital and sophistication to price the transaction fairly.

Critically, two of the five primary H1 2026 deals were first-ever continuation vehicles for their respective GPs — Latour Capital and Alantra Private Equity. That detail is more significant than it might appear. It marks the diffusion of the CV playbook beyond the large-cap buyout firms that pioneered it, into the European mid-market where the opportunity set is vast and the precedent-setting is only beginning.

"Continuation funds captured 24% of the total value of PE-to-PE exit transactions in Europe in 2025 — up from 8% in 2024. Invest Europe dedicated a standalone section to them for the first time."— Invest Europe Private Equity Activity Report 2025, May 2026

Infrastructure

1 deal · €2.2bn

The infrastructure segment produced the single largest transaction of the period, and one of the most structurally distinctive. Meridiam’s Europe Core Fund is not a GP-led CV in the traditional sense — it is a purpose-built liquidity window embedded into the design of a 25-year infrastructure mandate, demonstrating how the asset class is evolving its own variation of the continuation vehicle playbook.

The Meridiam transaction is notable for a second reason: alongside the institutional close, Meridiam launched its first retail-dedicated infrastructure fund, Meridiam Global Infrastructure Strategies, in partnership with Private Corner. The bundling of an institutional CV close with a retail feeder product is a structuring innovation that may become a template for other European infrastructure managers navigating the democratisation of private markets under ELTIF 2.0.

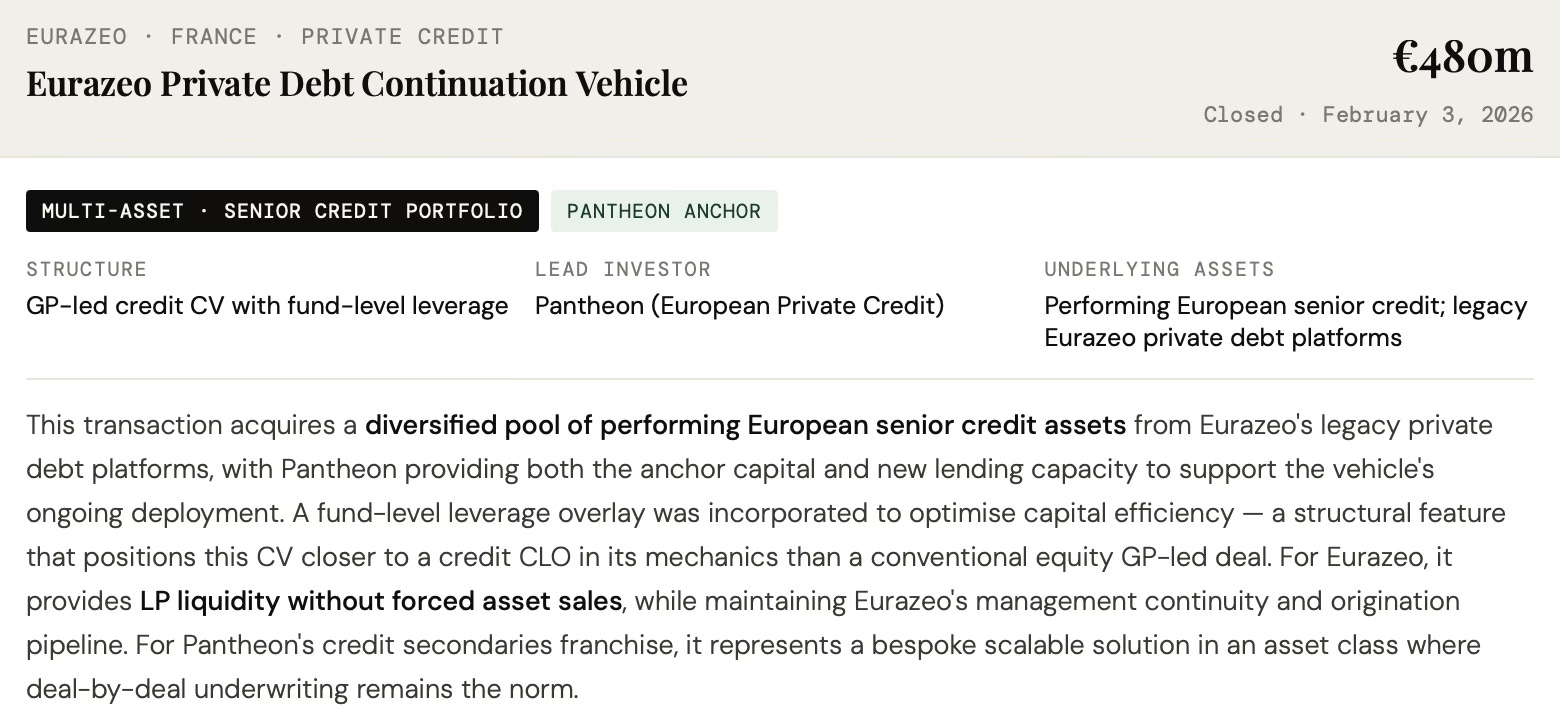

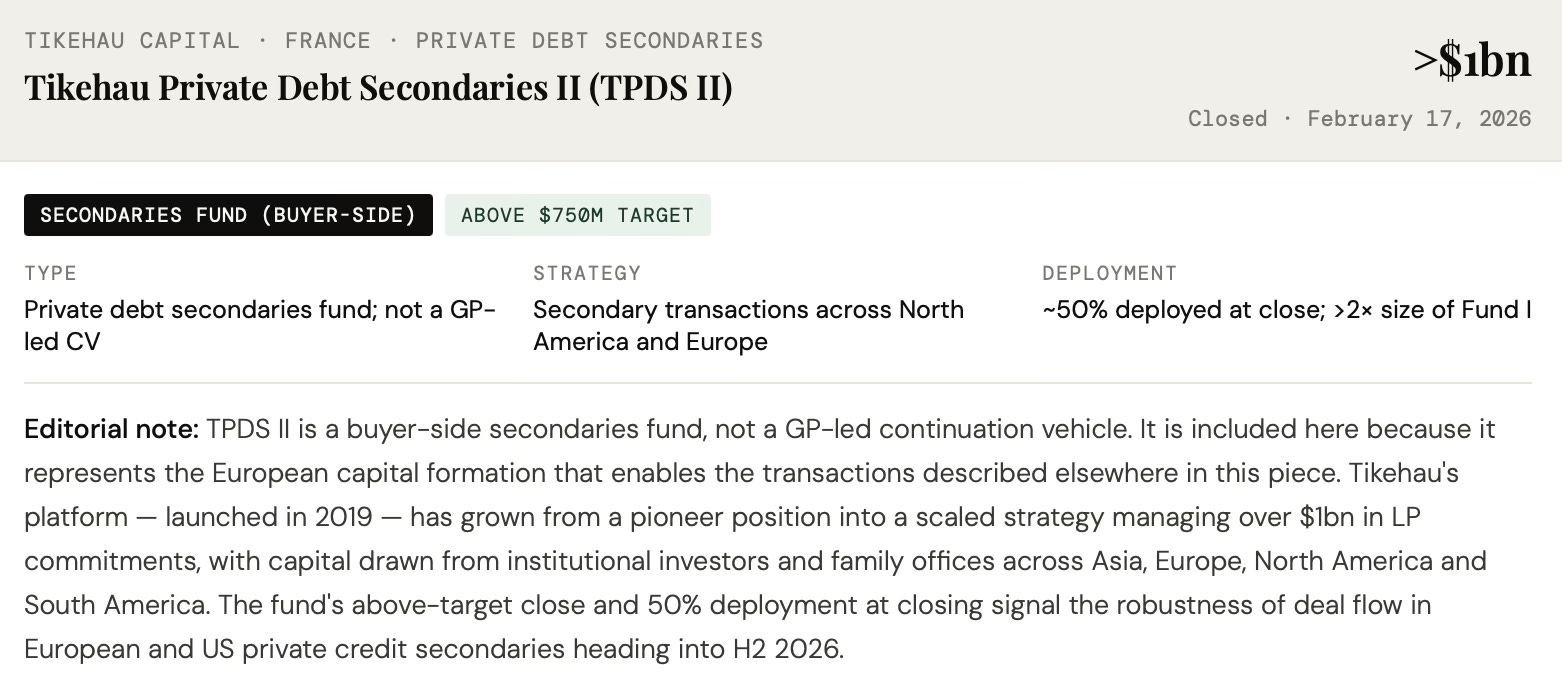

Private credit

2 deals · €480m + >$1bn

Private credit secondaries is the fastest-growing segment of the broader secondaries market — and H1 2026 produced both a GP-led CV and a dedicated secondaries fund close out of European managers. The asset class is maturing rapidly: where credit CV activity was once concentrated in US direct lending, European platforms are now producing their own structures with European collateral, European borrowers, and European institutional anchors.

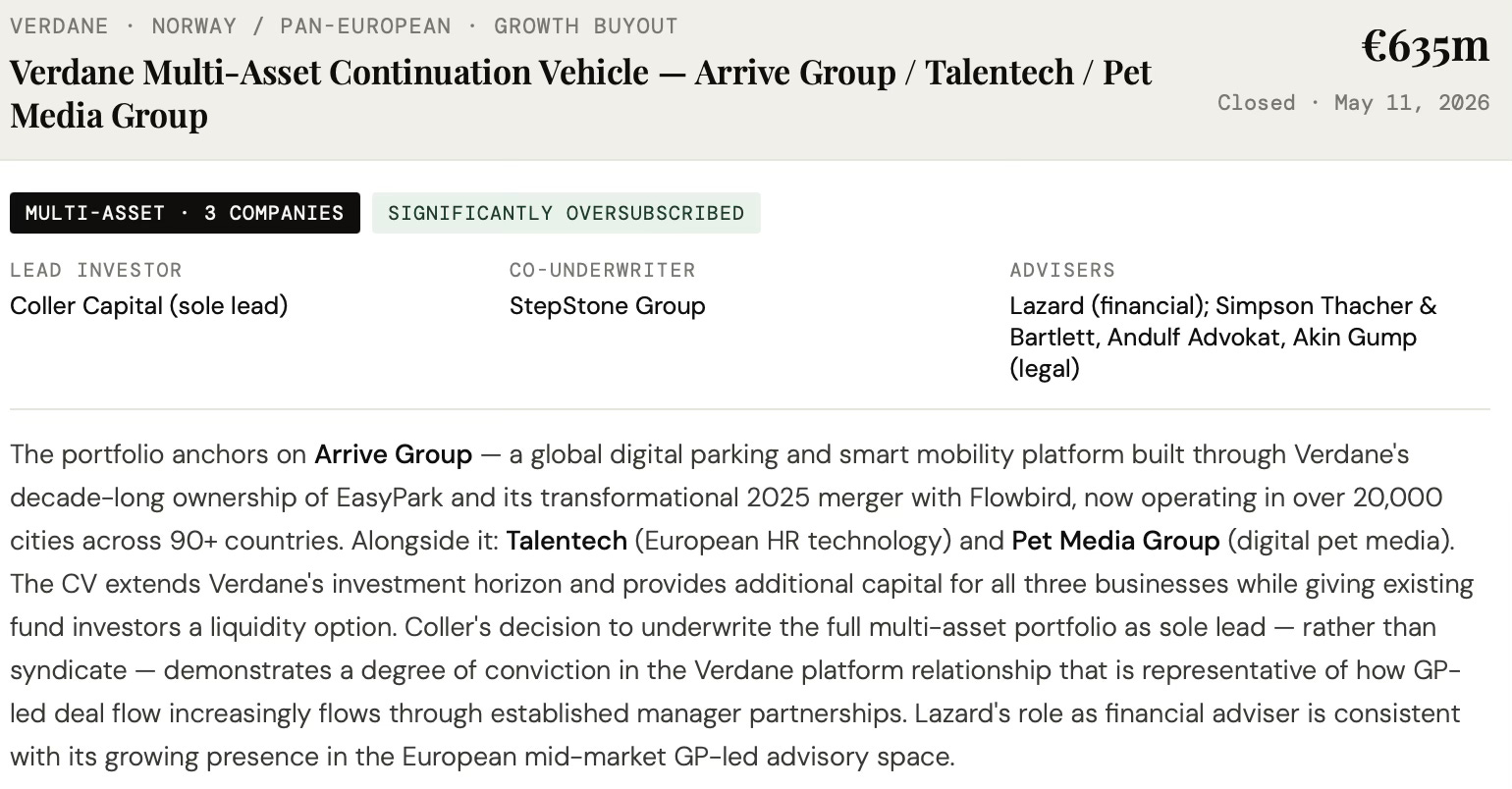

Growth buyout

1 deal · €635m

The Verdane transaction is the cleanest expression of the canonical European GP-led CV in H1 2026: a Nordic growth specialist, a 10-year-plus relationship with a flagship asset, a sole-lead secondaries buyer with the conviction and mandate to underwrite a full multi-asset portfolio, and a significantly oversubscribed outcome. It also carries a notable structural footnote — Arrive Group is moving into a continuation vehicle for the second time, having previously been held in a prior Verdane structure as EasyPark before the 2025 Flowbird merger.

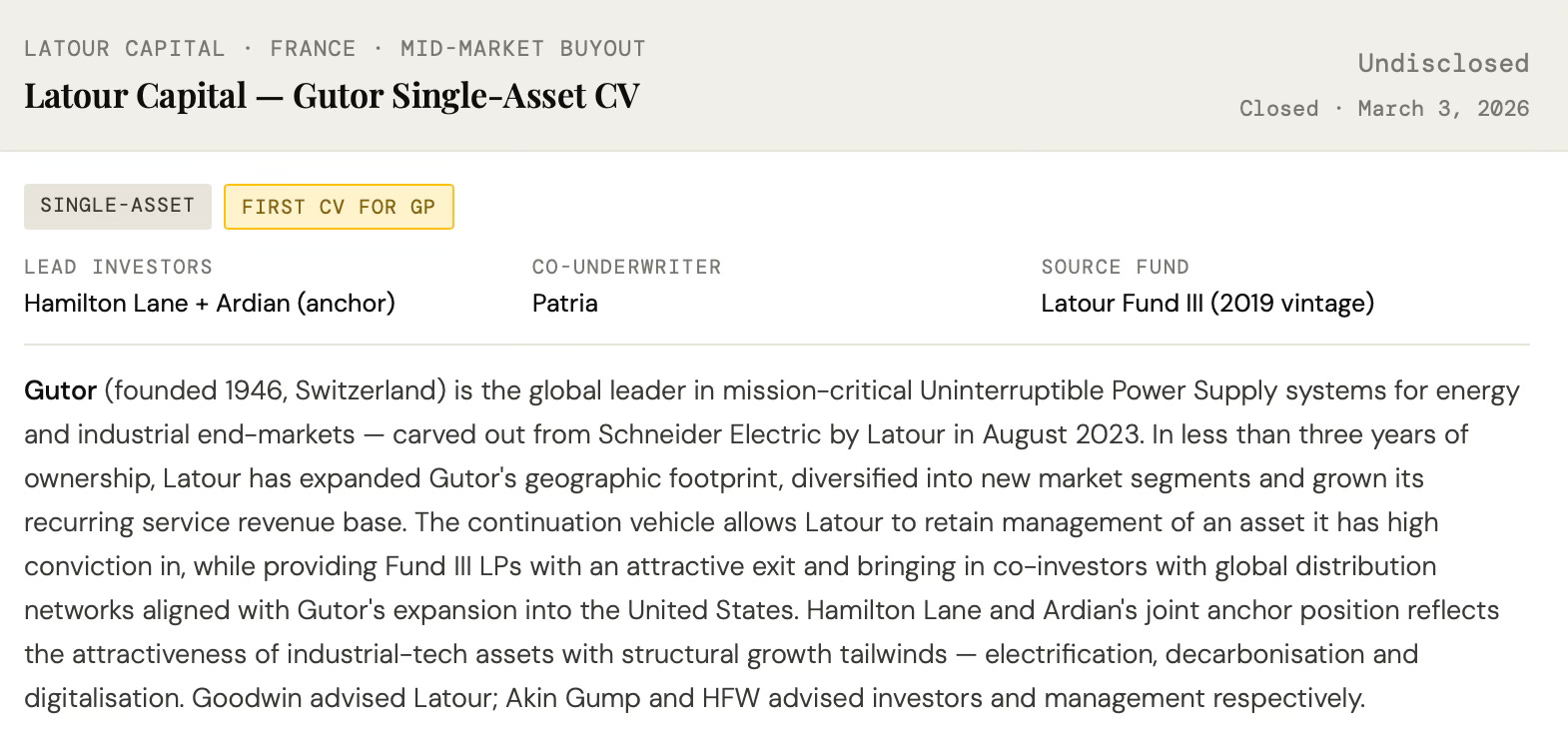

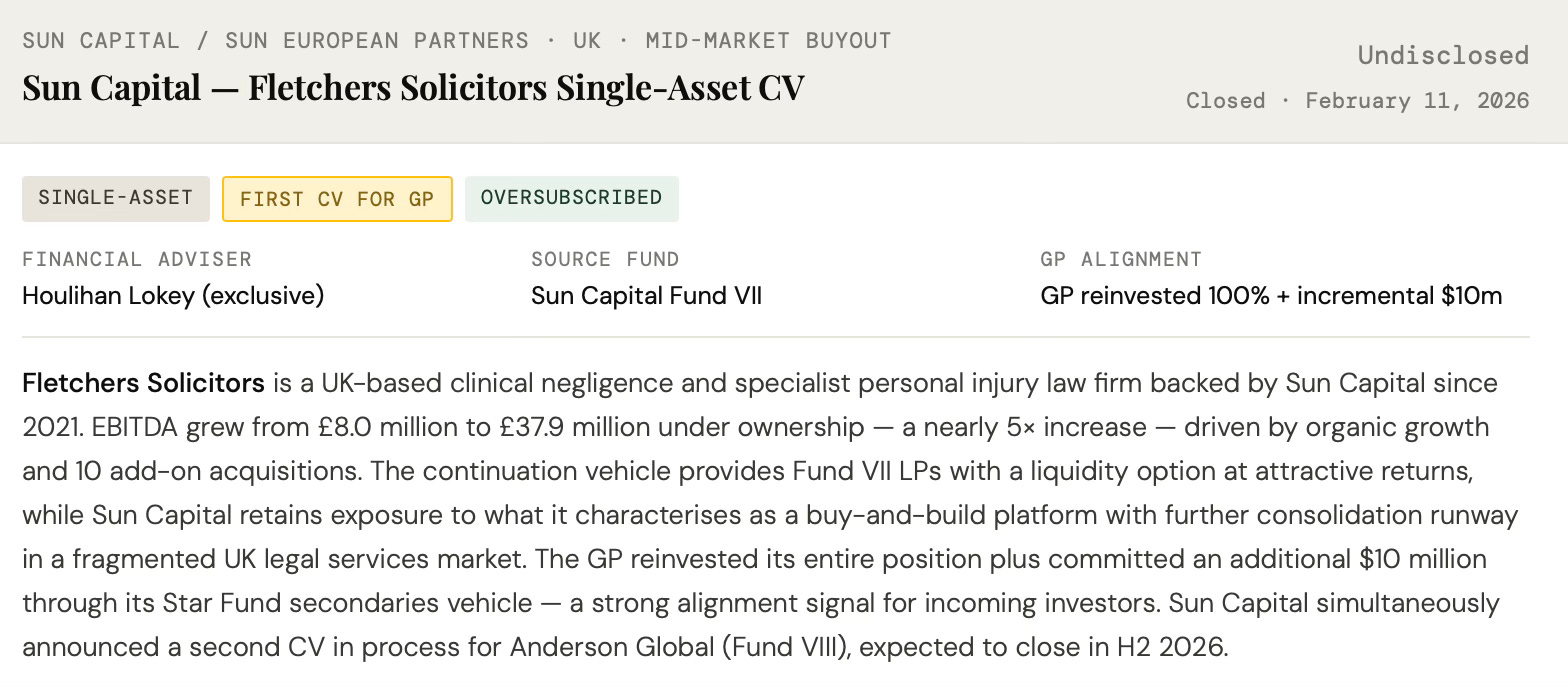

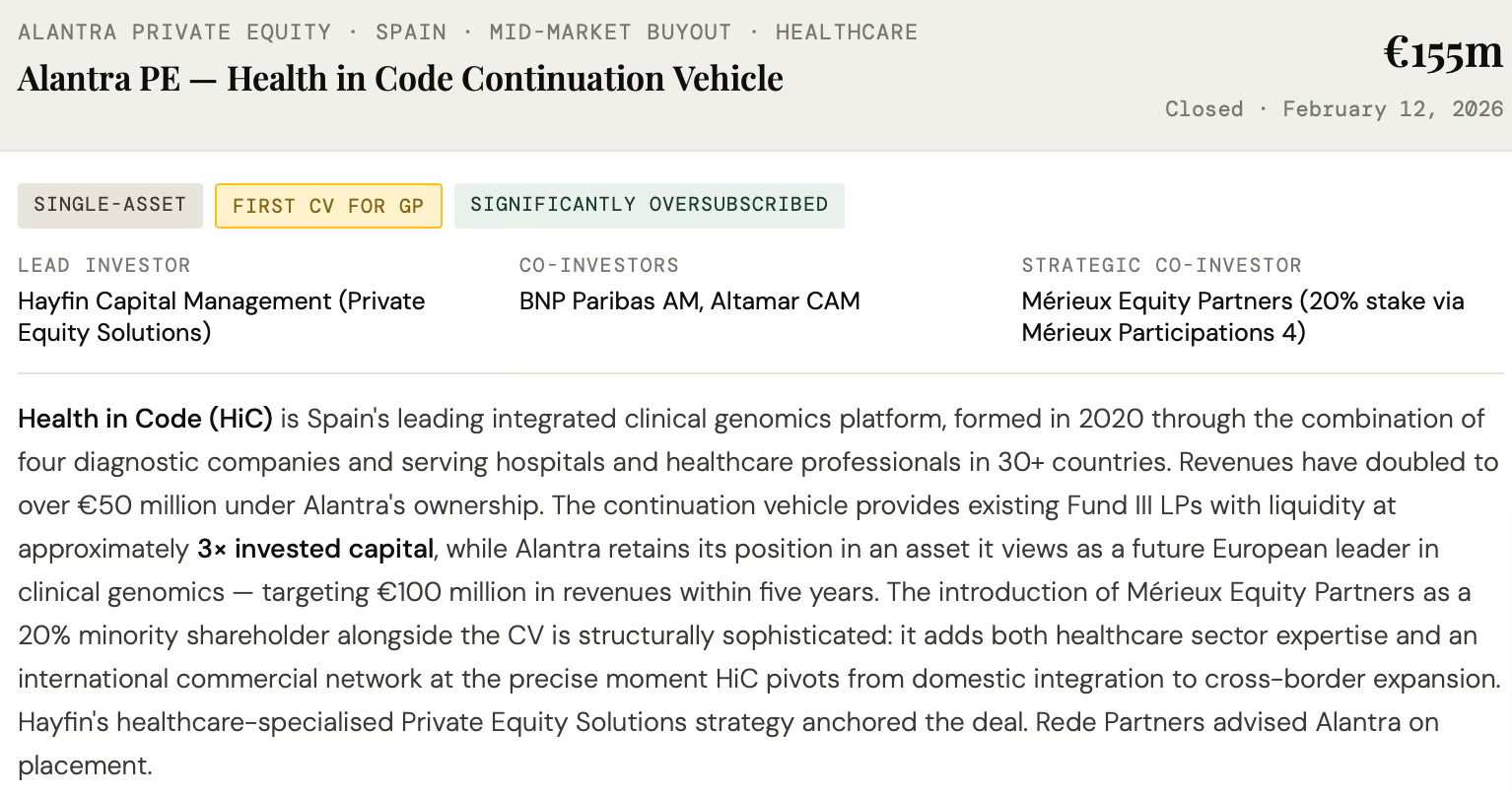

Mid-market buyout

3 deals · €155m + 2 undisclosed

The mid-market segment produced three of the five primary H1 2026 deals, spanning France, Spain and the UK. Two were first-ever CVs for their GPs — a structural milestone that signals the diffusion of continuation vehicles beyond the large-cap PE world into the heart of European mid-market private equity. The assets involved — a mission-critical Swiss industrial manufacturer, a UK legal services platform, and a Spanish clinical genomics group — reflect the breadth of sectors where GPs are now choosing extension over forced exit.

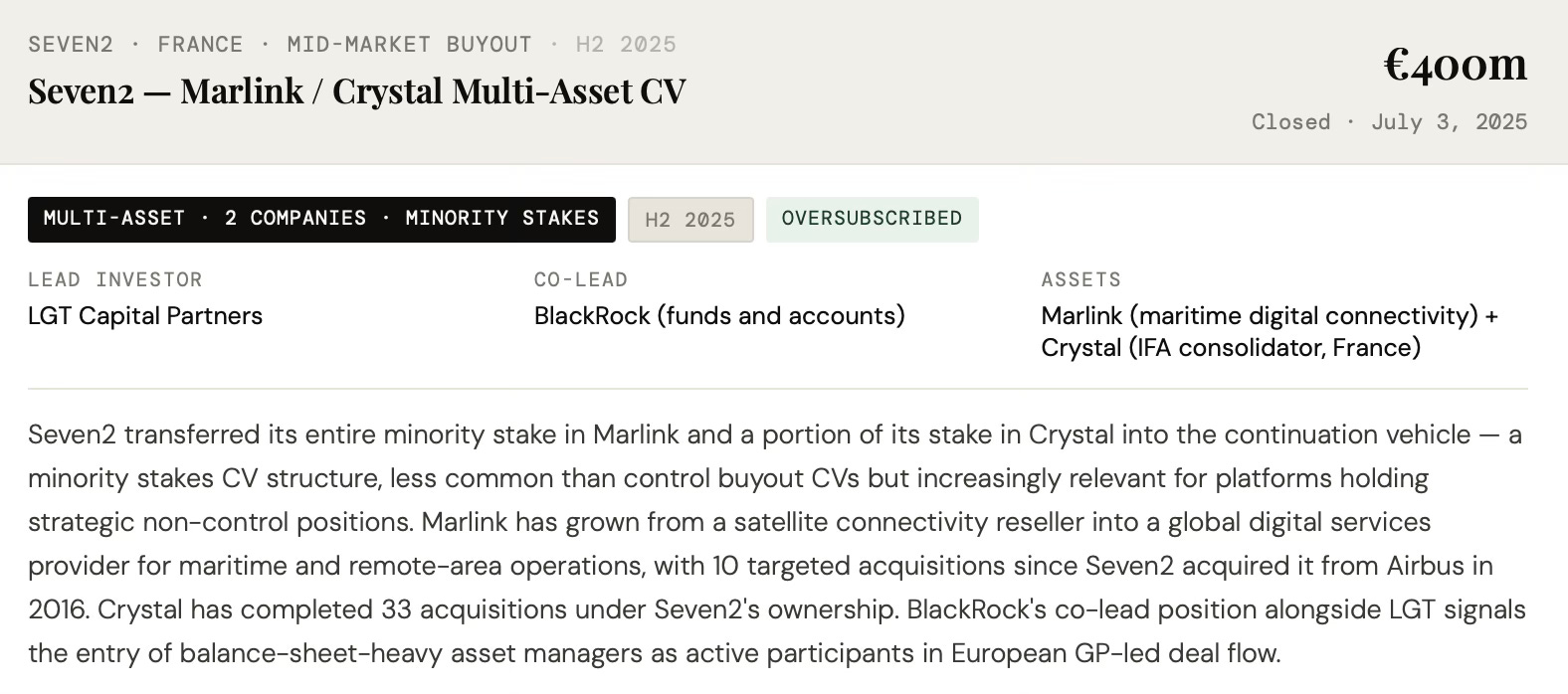

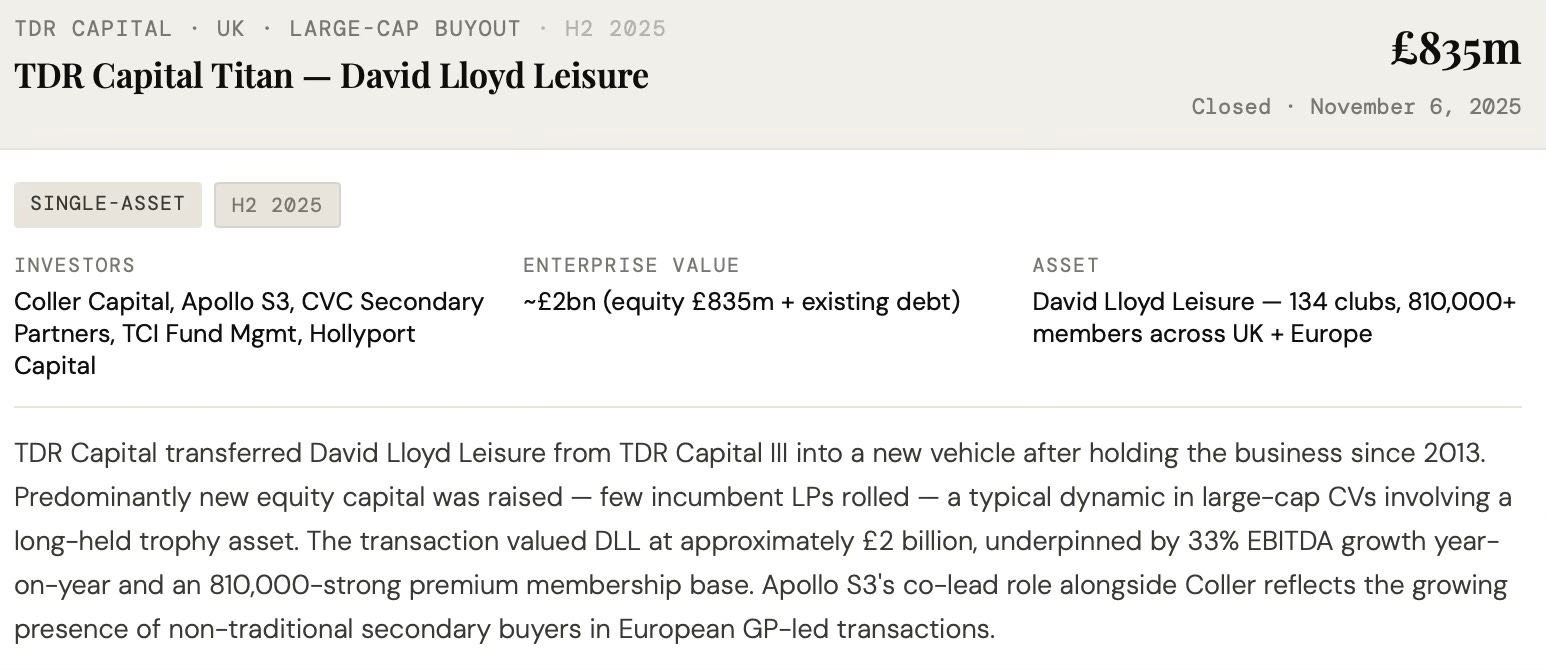

Prior period reference deals (H2 2025): Two high-profile European CVs closed in the second half of 2025 establish the pipeline context for H1 2026 activity and are included here for market completeness