Europe's PE-VC continuation fund market doubled in a year raising €19.8 billion in 2025

For the first time, Invest Europe dedicated a standalone section to continuation funds in its annual activity report. Continuation funds deployed €9.9 billion into 69 portfolio companies in 2025.

The Invest Europe annual activity report has tracked European private equity and venture capital since 1984. It is the most comprehensive dataset of its kind, covering fundraising, investments and divestments across the full spectrum of the asset class. The 2025 edition, published in May 2026, introduced continuation funds as a dedicated reporting category for the first time — a decision that is itself a statement about the structural significance the segment has reached.

The data covers PE and VC continuation funds contributing to the European Data Cooperative. Infrastructure funds, private debt funds, real estate funds and secondary funds of funds are explicitly excluded from Invest Europe’s universe. This is a critical methodological note: several of the largest European CV transactions of 2025–2026 — including Meridiam’s €2.2bn infrastructure continuation fund and Eurazeo’s €480m private debt CV — fall entirely outside the Invest Europe perimeter. The actual market is materially larger than the figures below.

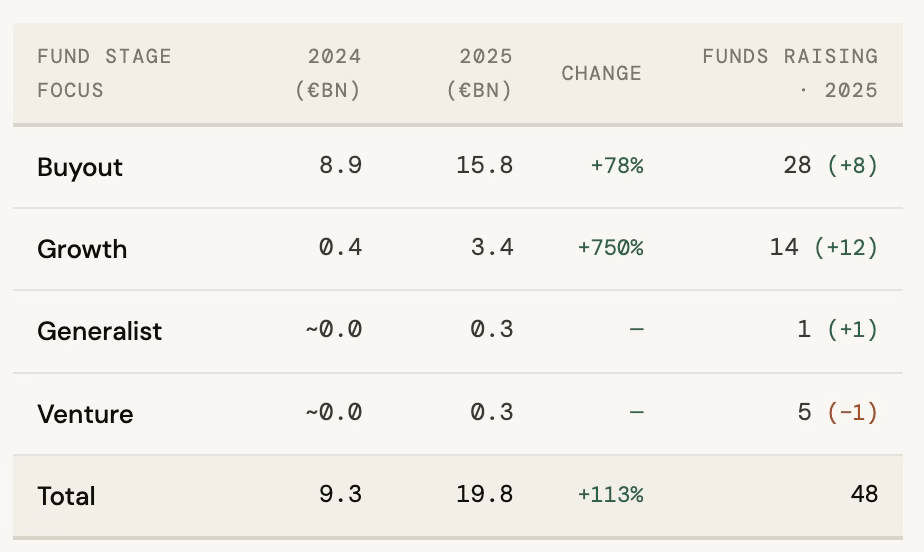

01- Fundraising: €19.8 billion and +113%

European PE/VC continuation funds raised €19.8 billion in 2025 — more than double the €9.3 billion recorded in 2024, and representing the strongest year on record by a significant margin. The number of funds completing a capital raise rose to 48, up from 28 the year prior. The increase was not concentrated in a single segment: buyout, growth and generalist continuation funds all expanded, while venture-backed CVs contracted slightly.

The growth segment surge is the most analytically significant number in the fundraising data. Growth continuation funds raised just €0.4bn in 2024 — an effectively nascent category. In 2025, they raised €3.4bn across 14 funds, adding 12 new fund closes in a single year. This is a direct reflection of the European growth equity ecosystem maturing past its first generation of funds: managers who backed digitally-enabled businesses in the 2014–2018 vintage years are now running continuation vehicles rather than forcing exits in a depressed M&A market.

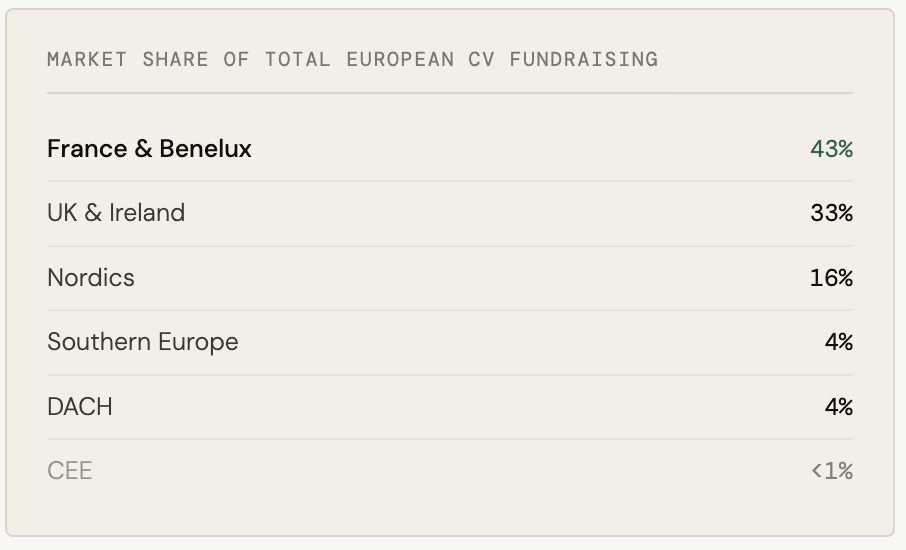

CV Fundraising by region: France & Benelux leads

Geographic concentration is striking. France & Benelux accounted for €8.6 billion — 43% of all European CV fundraising in 2025 — more than the entire market raised just two years prior. UK & Ireland followed at €6.5 billion, with the Nordics at €3.2 billion, Southern Europe at €0.8 billion and DACH at €0.7 billion. CEE recorded no material CV fundraising.

France & Benelux’s dominance reflects the depth and maturity of the French mid-market buyout ecosystem — the same ecosystem that produced the Seven2 and Latour Capital continuation vehicles tracked in our H1 2026 deal log, which will be released tomorrow. UK & Ireland’s position in second place, at €6.5bn, is consistent with the UK’s role as the historic home of European large-cap buyout, where continuation vehicles have been used for longer and at larger scale. The Nordics at €3.2bn — led largely by growth equity managers in Sweden, Norway and Denmark — is proportionally the most striking figure: Nordic managers produce a share of CV fundraising roughly double their share of overall European PE fundraising.

DACH’s apparent contraction (from €1.0bn to €0.7bn) is worth monitoring, though caution is warranted: the DACH market is historically less transparent in its reporting, and the category may be undercounted.

"France & Benelux accounted for 43% of all European continuation fund capital raised in 2025 — more than the entire European market raised in any prior year."— Invest Europe / EDC, Private Equity Activity 2025

02- Investments: €9.9 billion into 69 companies

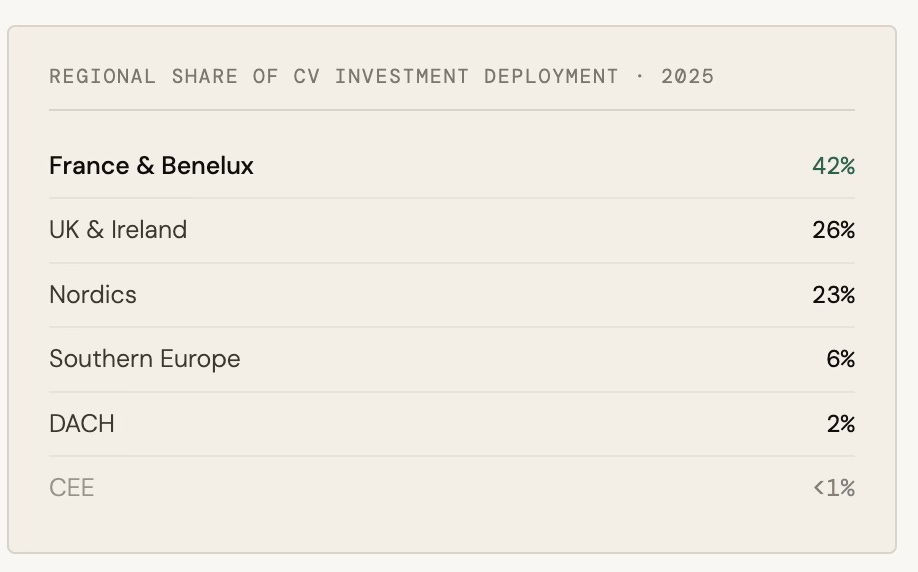

Continuation funds deployed €9.9 billion into 69 portfolio companies in 2025 — more than doubling the €4.7 billion invested across 32 companies in 2024. The buyout segment drove the expansion, with €9.3 billion deployed (94% of total) into 36 companies, up 19 companies from the prior year. Growth continuation fund investments reached €0.5 billion across 12 companies, and venture-backed CVs invested a negligible amount across 21 companies — declining slightly in company count but consistent with the very early stage of venture CV development in Europe.

The UK & Ireland investment figure deserves careful reading. The jump from €0.8bn to €2.6bn in portfolio company location — a 225% increase — is disproportionately large relative to UK & Ireland's fundraising growth. This reflects cross-border CV activity: French and Nordic managers structuring continuation vehicles that hold UK-based assets. The TDR Capital Titan (David Lloyd Leisure) transaction from late 2025 is the clearest example — a UK-domiciled portfolio company held in a vehicle structured by a UK GP, but with secondary capital mobilised from a global buyer group. Geographic mismatch between where CVs are raised and where the underlying assets sit is becoming a defining feature of the European market.

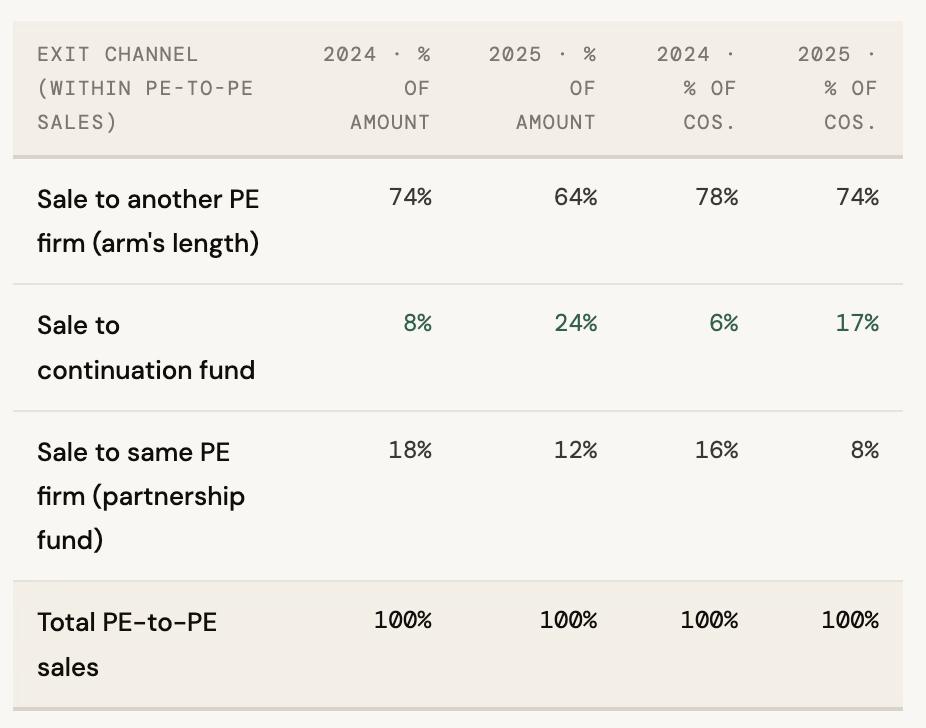

03- Divestments: the 8% to 24% shift

The divestment data is the most structurally significant section in the Invest Europe CV report, and the one most likely to reshape how institutional LPs think about private equity exit modeling. In 2025, European private equity firms divested €19.7 billion worth of assets through sales to another PE firm. Of that total, 24% was sold to a continuation fund — up from 8% in 2024. By number of companies, 17% of PE-to-PE exits went via a continuation fund, up from 6%.

The 8%-to-24% move in a single year is not a rounding error or a statistical outlier. It is the result of a structural pipeline maturing simultaneously across three generations of European buyout funds: the 2012–2015 vintages nearing or exceeding their natural hold periods, traditional exit routes remaining subdued, and a secondary buyer universe that has spent two years accumulating dry powder and developing underwriting infrastructure for complex GP-led transactions.

The simultaneous fall in “sale to same PE firm / partnership fund” (from 18% to 12% of value) is also meaningful. It suggests that internal recycling of assets — transfers between an old fund and a successor fund managed by the same GP — is being replaced by properly structured, third-party-anchored continuation vehicles, which offer genuine LP optionality, independent pricing, and a clean governance process. The market is maturing in exactly the direction ILPA guidance anticipated.

Importantly, this data covers only exits classified as “sale to a PE firm” in Invest Europe’s taxonomy. Continuation fund activity embedded in other exit categories — for example, recapitalisations, partial realisations, or structures involving both debt and equity — would sit elsewhere in the data. The 24% figure is almost certainly an undercount of the true share of European PE exits involving CV mechanics.

04 How CVs fit into the broader 2025 picture

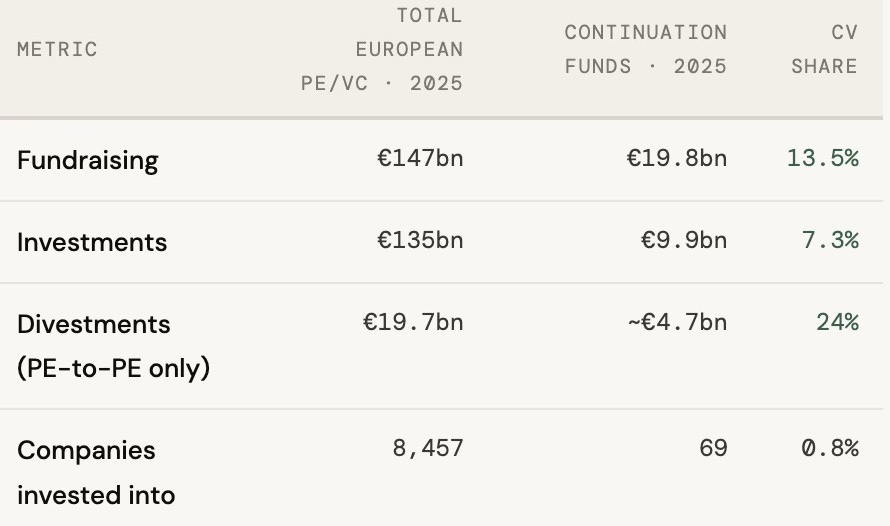

European private equity and venture capital raised a record-adjacent €147 billion in 2025 — the second-best year on record, behind only 2022’s €195 billion peak. Investments reached €135 billion into 8,457 companies, and divestments came in at €45 billion at historic cost across 3,324 companies. Buyout dominated as usual: €103 billion raised, €90 billion invested, €32.5 billion divested.

Within this overall picture, continuation funds represented 13.5% of total European PE/VC fundraising in 2025 — up from roughly 7% in 2024. On the investment side, the €9.9 billion deployed by CVs represented 7.3% of total PE/VC investment volume. These are not marginal percentages. CVs are now a double-digit line item in the European private capital budget.

The contrast between 13.5% of fundraising and 0.8% of company count is the core structural tension in the European CV market. Continuation funds raise enormous amounts of capital relative to the number of assets they deploy into — by definition, because each CV holds between one and a handful of companies. The average CV investment per portfolio company in 2025 was €144 million (€9.9bn ÷ 69 companies). For comparison, the average European buyout investment per company was €55 million (€90bn ÷ 1,629 companies). CVs are large-ticket, concentrated instruments — which is precisely what makes secondary underwriting them complex and LP governance so important.

What the 2026 data will tell us

Will growth CVs sustain the surge? The 750% increase in growth CV fundraising (€0.4bn → €3.4bn) and the addition of 12 new fund closes in a single year is either the start of a durable structural trend or a one-year catch-up from a cohort of overdue vintage funds. If the 2018–2021 European growth equity vintage is as large as it appears, there is a three-to-five-year pipeline of potential growth CVs still to come.

Will the 24% divestment share hold or accelerate? The jump from 8% to 24% in a single year is historically unprecedented in any segment of European PE exit data. Whether this normalizes at a new structural level around 20–25% or continues rising toward 30%+ will define how mainstream continuation vehicles become as a primary exit mechanism — and whether LPs begin discounting GP fundraising by the expected CV overhang.

Will Invest Europe expand the perimeter? The decision to exclude infrastructure and private debt from the CV data creates a growing blind spot as those asset classes increasingly use CV-style structures. Watch for whether the 2026 edition expands the methodology, which would produce an immediate and significant upward revision to European CV market size estimates.

Southern Europe watch. Southern Europe raised €0.8bn in CV capital in 2025 and received €0.6bn in CV investments — the smallest allocation of any major European region. With Alantra PE (Spain) completing its first CV in H1 2026, and several Italian and Portuguese growth managers approaching the end of their first fund generations, this may be the region with the largest relative catch-up potential heading into 2026–2027.

DACH contraction warrants explanation. DACH is the only European region to show a nominal decline in CV fundraising between 2024 and 2025 (€1.0bn → €0.7bn). The German, Austrian and Swiss mid-market is large and structurally underserved by continuation vehicle structures. Whether this is a data anomaly, a vintage timing issue, or a genuine structural lag will be important to assess as 2026 data accumulates.

COMING TOMORROW · SECONDARY SCOOP

European continuation vehicle deal log: H1 2026

From Verdane’s €635m growth CV anchored by Coller Capital to Meridiam’s €2.2bn infrastructure liquidity window and Alantra PE’s first-ever healthcare CV in Spain — a detailed deal-by-deal analysis of every significant European continuation vehicle announced or closed between January and May 2026, organized by asset class.

| A guest post by

|