Golding Capital Maps Seven Pitfalls in Small-Cap GP-Leds. The Upshot: Scale Is the Enemy of Alpha Here.

Munich-based private markets investor Golding Capital Partners has published a whitepaper laying out a seven-point risk framework for GP-led secondaries in Europe’s lower-middle market — continuation vehicles of €500 million or less, often involving companies with up to €50 million of EBITDA. The paper, co-authored with Linklaters on governance and process integrity, arrives as the broader GP-led market continues to set records but as capital concentrates ever more heavily among a handful of large-cap secondaries funds.

Golding’s core argument will be familiar to anyone who has tracked the small-cap buyout thesis: less standardization means fewer competing bidders, wider pricing dispersion, and — for managers with the underwriting muscle to do the work — the potential for outsized returns. The flip side is that the same lack of standardization is where lower-end CVs go wrong.

The framing shift: CVs as toolkit, not workaround

The paper opens by dispatching what it calls an “outdated” view — that continuation vehicles are primarily a release valve for weak exit markets. Citing Preqin’s Private Equity in 2026 survey, Golding notes that 52% of investors now consider the GP-led secondaries strategy attractive and 38% are active as buyers or sellers, with single-asset CVs dominating that activity. KPMG’s estimate that continuation vehicles already represent roughly a fifth of sponsor-led exits is presented as confirmation that the structure has moved from cyclical patch to permanent fixture of the private equity lifecycle.

That framing aligns closely with the editorial position this publication has taken repeatedly: secondaries, including GP-leds, are portfolio management tools rather than distress signals. Golding’s contribution is to push that argument down-market, where — the paper argues — the dynamics are structurally different from the large-cap CVs that dominate headline volume figures.

“The central risk in GP-led secondaries does not lie in the structure itself, but in the underlying transaction rationale.”

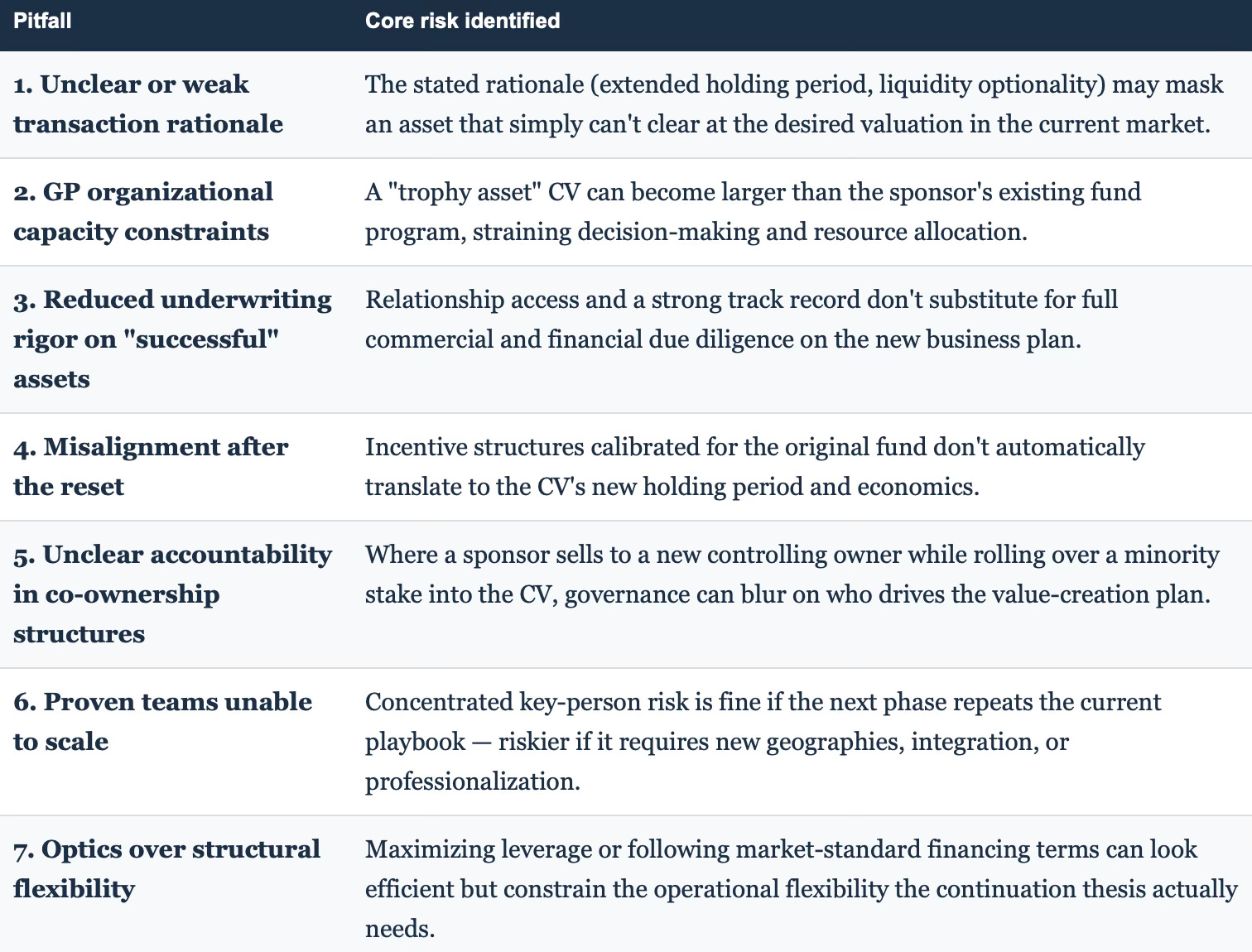

Seven pitfalls, one underlying theme

The bulk of the paper is organized around a framework of seven recurring failure modes that Golding says it sees across cycles and geographies in the lower end of the market. The through line across all seven is that smaller CVs are more “situation-specific” — fewer standardized data rooms, more concentrated investor groups, and managers whose organizational capacity may not scale with the size of the vehicle relative to their existing fund program.

The governance lens: why rationale drives conflict management

The Linklaters-authored governance sections — credited to Martin Mager and Zornitsa Chorbadzhiyska — make a structural argument that’s worth flagging separately from the investment framework. Their point is that the sponsor’s inherent conflict in a GP-led deal (representing both the selling fund and the buying vehicle) isn’t resolved by documentation alone. Where the transaction rationale is genuinely credible — a defined growth phase, an operational transformation — disclosure tends to be more comprehensive and LPAC engagement “more constructive,” even where investors disagree on price. Where the rationale is weak, the paper argues, governance mechanisms get asked “to do more than they can realistically deliver,” and tensions surface as compressed timelines and selective disclosure.

This is a useful framing for LPs evaluating CV consents: the quality of the process itself can be read as a signal about the quality of the underlying rationale.

WORTH NOTING

The paper references the ILPA Continuation Fund Disclosure Template (dated 27 January 2026) as an industry standardization effort — while cautioning that the added reporting infrastructure it implies “may also require additional processes,” particularly for smaller GP platforms. For a market where Golding’s whole thesis rests on smaller managers being less standardized by nature, that’s a tension worth watching: does ILPA-driven standardization compress the very inefficiency that creates the lower-market opportunity, or does it simply raise the operational bar for GPs to participate in CVs at all?

Practitioner notes: pricing, leverage, and the “bridge” toolkit

Beyond the seven pitfalls, the paper closes with three market-practice observations framed as neither risks nor opportunities in themselves, but as execution trends specialist investors are increasingly navigating:

Bridging valuation gaps — deferred consideration, earn-outs, and performance-linked instruments are described as most effective when negotiated early through trust-based GP dialogue, rather than bolted on late to win a competitive process.

Pricing convergence with M&A logic — Golding notes that GP-led pricing, historically anchored to discounts off last reported NAV, is increasingly converging with traditional M&A methodologies, including concurrent debt refinancings. W&I insurance use is rising but remains selective at smaller deal sizes, reflecting a cost-versus-risk-transfer trade-off.

Vehicle-level leverage as a value driver — or not — the paper is blunt that incremental structural leverage at the vehicle level “rarely enhances the underlying economics of the asset itself” in the lower-middle market, where value creation is operational rather than financial-engineering-driven.

The takeaway

Golding’s framework doesn’t break new conceptual ground for readers steeped in the GP-led literature — the tension between rationale and structure, the conflicted-sponsor problem, and the case for the small- and mid-market have all been made before by various secondaries platforms. What this paper does is package those arguments specifically around the European sub-€500 million segment, with a governance overlay from Linklaters that goes deeper on process design than most LP-facing secondaries marketing material typically does. For an audience increasingly asked to evaluate CV consent requests on tight timelines, the seven-pitfall checklist functions less as new insight and more as a structured diligence template — which may be exactly the point.