Houlihan Lokey: The Secondaries Business That's Bigger Than You Think

Houlihan Lokey just posted a record $2.6 billion fiscal year. Its Capital Solutions platform has 200 professionals, $36 billion raised, and more than $19 billion in GP-led secondary experience.

Houlihan Lokey just posted a record $2.6 billion fiscal year. Its Capital Solutions platform has 200 professionals, $36 billion raised, and more than $19 billion in GP-led secondary experience. So why isn't it in every secondaries conversation?

What Is Houlihan Lokey?

For readers encountering the firm for the first time: Houlihan Lokey (NYSE: HLI) is a pure advisory investment bank founded in Los Angeles in 1972. Like Moelis, it has no balance sheet deployed in transactions, no proprietary funds, and no AUM. It earns fees exclusively from advice.

The firm went public in 2015 and has grown into one of the most recognizable independent advisory platforms in the world. As of March 31, 2026, it employs 2,776 people across 33 offices worldwide, has 354 Managing Directors, and generated $2.6 billion in revenue for the fiscal year ending that date — growing at an 11% five-year CAGR. In nine of the ten years since its IPO, it has delivered annual revenue growth.

Its three business segments are Corporate Finance (67% of revenue), Financial Restructuring (20%), and Financial and Valuation Advisory (13%). Within Corporate Finance, the two product lines are Mergers & Acquisitions and Capital Solutions — the latter being where the secondaries business lives.

Houlihan Lokey is also the most acquisition-active boutique bank in this peer group, having completed 20 acquisitions over the last 15 years, including Audere Partners (France, February 2026), Mellum Capital (European real estate, January 2026), and Waller Helms Advisors (insurance and wealth management, December 2024).

The Record Year in Numbers

Fiscal year 2026 — April 2025 through March 2026 — was a record by nearly every measure:

Total revenues: $2.618 billion, up 10% year-over-year

Adjusted EPS: $7.56, up 20%

Adjusted pre-tax margin: 25.9%, flat versus FY2025 but among the highest in the peer group

Adjusted net income: $518 million, up from $434 million the prior year

Managing Directors: 354, up from 339 in FY2025, growing at an 8% CAGR over 20 years

Revenue per MD: $7.6 million, up from $7.3 million

Corporate Finance — the segment that contains Capital Solutions and therefore secondaries — grew 14% for the year to $1.745 billion, with a 17% five-year revenue CAGR. That makes it by far the fastest-growing segment, outpacing Financial Restructuring (0% five-year CAGR) and Financial and Valuation Advisory (13% five-year CAGR).

The Q4, ending March 31, 2026, was more complicated: revenues of $635.6 million were down 5% year-over-year, reflecting two large restructuring transactions that slipped past quarter-end, geopolitical disruption from the Middle East conflict, and software-sector volatility hitting CF deal timing. CEO Scott Adelson was clear-eyed about it — but equally clear that the pipeline heading into fiscal 2027 is at record levels.

Capital Solutions: The Hard Numbers

The Capital Solutions Group comprises 200 dedicated professionals across 18 offices in eight countries as of March 31, 2026. In FY26 - it has raised $36 billion in capital and closed more than 140 transactions. The group explicitly describes itself as one of the largest capital solutions groups at non-balance-sheet banks.

The secondaries piece sits within a sub-group called Secondary Solutions, which covers continuation vehicles, fund tender processes with stapled capital, and sale of LP interests and strip sales. Surrounding it are related capabilities that are highly relevant to secondaries activity: GP Advisory (strategic advisory for asset managers, firm-level equity stake sales, fund-level NAV loans and preferred equity), Directs & Co-Investments (LP-style capital for single-asset transactions, mid-life co-investments), and Primary Capital Advisory (placement for control buyout, growth equity, and alternatives strategies).

The investor presentation also formally lists “Continuation Vehicles and Other Secondaries” as one of the three connecting bridges between its M&A, Capital Solutions, and Financial Restructuring platforms — confirming that HL sees GP-led secondaries as a product that sits at the intersection of all three of its core business lines. That integration is the key differentiator.

On the revenue size question: during the earnings call, CFO Lindsey Alley confirmed that Capital Solutions is 20% of Corporate Finance revenues and that percentage has been growing over the last couple of years. With Corporate Finance at $1.745 billion for the year, that implies Capital Solutions contributed at least $349 million in FY2026 — a nine-figure business growing faster than the M&A segment it sits alongside.

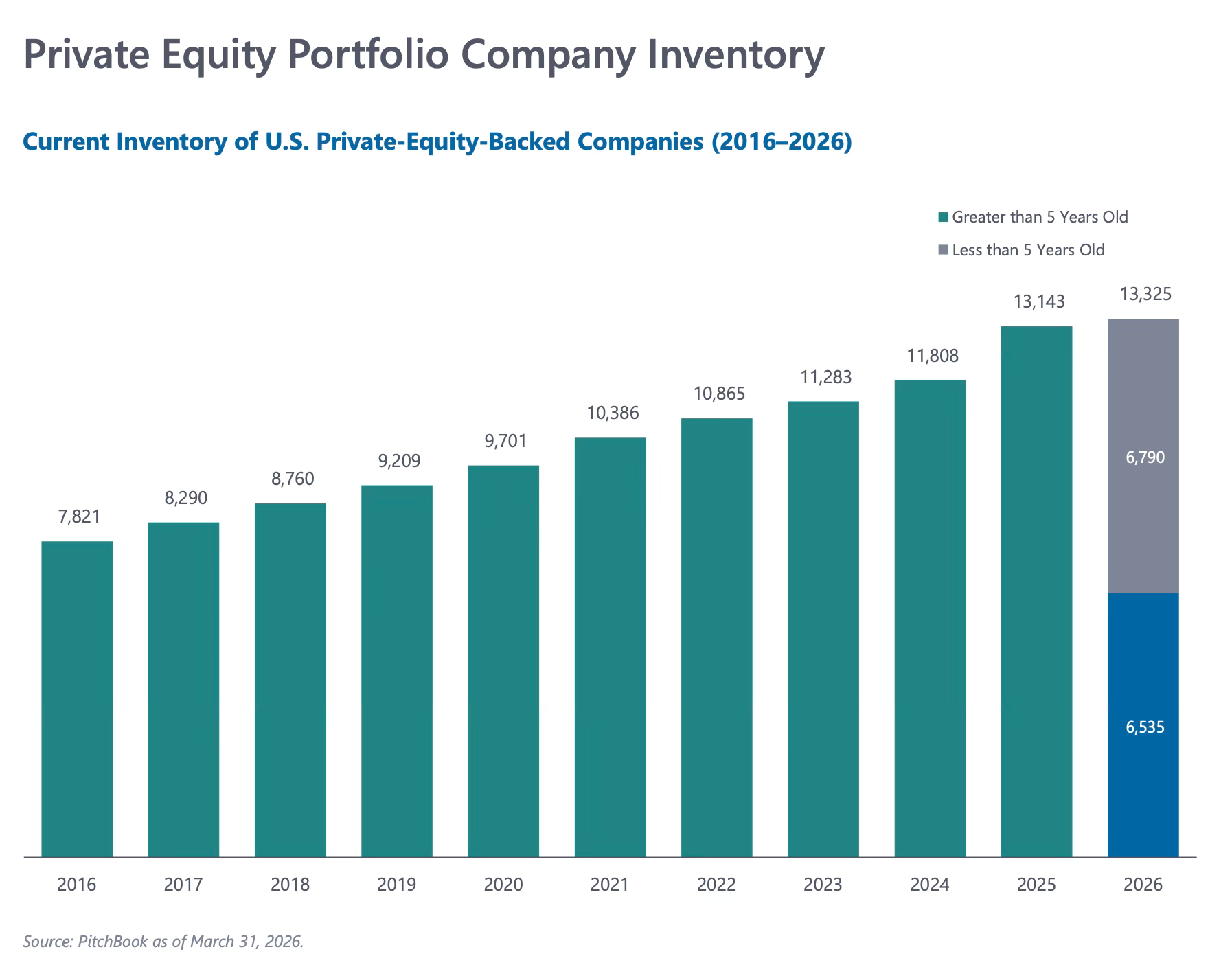

The Pent-Up Demand Chart That Explains Everything

The investor presentation contains a PitchBook chart that Adelson explicitly referenced on the earnings call — and it is arguably the single most important visual for understanding the secondaries opportunity at Houlihan Lokey right now.

The chart shows the inventory of U.S. private-equity-backed companies from 2016 to 2026. The total has grown from 7,821 in 2016 to 13,325 in 2026 — a 70% increase in a decade. More importantly, of those 13,325 companies, 6,790 are now more than five years old. That is over half the entire inventory past a typical hold period, sitting in portfolios waiting for an exit path that traditional channels — IPOs and strategic M&A — have not reliably provided since 2022.

Adelson summarized it directly on the call: there is a lot of pent-up demand. “Over half of them are over five years old. To answer your question with an exclamation point, there is a lot of pent-up demand.” That aging inventory is the structural engine behind the GP-led secondaries market, and Houlihan Lokey, as the most active advisor to private equity globally (286 PE transactions in 2025, per The Deal), is positioned directly in the middle of it.

The firm has 30 senior officers dedicated to the financial sponsor community in North America, Europe, and Japan, covering 1,900 financial sponsor firms across private equity, credit, family offices, and institutional investors. That network is the distribution engine for Capital Solutions mandates — every M&A engagement is a potential introduction to a GP who will eventually need a continuation vehicle.

GP-Led Secondaries and the Restructuring Overlap

One of the most interesting strategic angles from the earnings call is how explicitly Houlihan Lokey’s leadership described the connection between restructuring tailwinds and secondaries opportunity.

Adelson flagged four converging factors driving an improved restructuring outlook for fiscal 2027: widening credit spreads, dislocation in private credit, software sector stress, and energy volatility. He described “several notable recent wins” and used the phrase “elevated levels” — the same language the firm has deployed for three consecutive years of strong restructuring performance.

For secondaries readers, this matters because GP-led secondaries and restructuring increasingly serve adjacent constituencies. A PE firm managing an overleveraged portfolio company in private credit or a repriced software asset may simultaneously need a restructuring advisor for the capital stack and a secondaries advisor to give existing LPs liquidity while bringing in new capital. Houlihan Lokey, with 59 restructuring MDs and one of the largest Capital Solutions teams in the market, is one of the very few advisory firms that can handle both sides of that situation in-house.

The investor presentation formalizes this: “Liability Management” is one of the connecting bridges in the firm’s service diagram between Financial Restructuring and Capital Solutions. GP-led secondaries that involve distressed or out-of-favor assets are precisely the transactions where that integration creates genuine competitive advantage.

The European Buildout

The investor presentation maps Houlihan Lokey’s Capital Solutions team across 18 offices, including London, Paris, and Zurich — the last of which was added with the September 2025 hire of Sandro Galfetti, formerly Head of EMEA Secondary Advisory at UBS Investment Bank. He joined Michael Pilson, who relocated to London, to co-lead GP-led secondary advisory in Europe.

The European expansion matters for three reasons. First, the European GP-led market is at an earlier adoption stage than the U.S. and growing faster. Second, Houlihan Lokey’s acquisition of Audere Partners in France gives the Capital Solutions team direct access to a market where GP-led transactions have historically been underserved by dedicated advisors. Third, EMEA already represents 26% of HL’s total revenue — the largest international region — and CF revenues outside the U.S. grew significantly faster than domestic revenues in both Q4 and the full fiscal year. The infrastructure is there; the Capital Solutions team is now being layered on top of it.

HL’s own research supports the timing. Its LP Compass survey, published in March 2026, found that 86% of active secondary buyers expect 2026 volumes to exceed last year’s record of $225 billion, with European deal flow cited as a meaningful growth contributor. The survey also found that 85% of investors say GP-led deal quality has held firm or improved despite rapid market expansion — an important signal that the market is maturing, not degrading.

The Valuation Advisory Second Derivative

A question on the earnings call surfaced a secondaries angle that is easy to overlook: the connection between Houlihan Lokey’s Financial and Valuation Advisory business and the growing demand for independent marks on private credit and PE portfolios.

Adelson’s response was enthusiastic. The portfolio valuation group, he said, has been growing through all cycles, private credit dislocation is driving more frequent and more rigorous marking, and if private equity exits open up broadly, the Total Addressable Market for valuation services could double.

The investor presentation confirms the scale of this business: 2,500+ annual valuation engagements, the #1 global M&A fairness opinion advisor for 25 consecutive years, and the Best Valuations Firm for Hard to Value Assets globally for seven straight years. As secondary transaction volumes grow — and as buyers and sellers of GP-led and LP-led positions increasingly require independent valuation support — HL’s FVA segment becomes a natural adjacency to the Capital Solutions team. The same firm that advises on the continuation vehicle can provide the independent mark on the underlying assets. That is a meaningful cross-sell and a genuine service differentiation.

What to Watch in Fiscal 2027

Three things to track for Secondary Scoop coverage:

Capital Solutions’ revenue trajectory. With Corporate Finance growing at a 17% five-year CAGR and Capital Solutions above 20% of that — and growing — the absolute revenue figure is likely approaching $400 million or beyond in FY2027 if momentum holds. Watch for any decision by management to break out Capital Solutions as a separately disclosed segment. The business is large enough to warrant it.

The European GP-led pipeline. The Galfetti hire in Zurich, the Audere acquisition in France, and the relocation of Michael Pilson to London all point to a deliberate push to build deal flow in EMEA continuation vehicles. The first marquee European GP-led closes from this team would be a significant signal.

Private credit secondaries. Adelson’s comments on private credit dislocation, combined with the valuation advisory tailwind and the firm’s explicit GP Advisory capabilities (NAV loans, preferred equity, fund-level debt), suggest HL will increasingly be in the room when credit-focused GPs need liquidity solutions. That market is early but directionally important.

Houlihan Lokey enters fiscal 2027 as the #1 global M&A advisor by transaction count, the #1 global restructuring advisor for 11 consecutive years, and — based on the data now available — the operator of what may be the largest secondaries advisory team among non-balance-sheet banks. The record backlog, the aging PE portfolio inventory, the European buildout, and the restructuring tailwinds all point in the same direction.

For GP-led secondaries, the setup has rarely looked better. And Houlihan Lokey is squarely in the middle of it.

| A guest post by

|

The enthusiasm for HL, combined with no questions about anything HL says and the lack of comparison to competitors (including, not excluding competitors who use their balance sheets), reduces the impact of the analysis.