How Apollo is using daily pricing and market-making to create the conditions for a liquid private credit secondary market

Apollo's Q1 2026 earnings call was not primarily a secondaries call. It was a broad update on a firm that just crossed $1 trillion in AUM, posted record fee-related earnings of $728M, and reaffirmed 20% FRE growth for the year. But inside CEO Marc Rowan's prepared remarks and the Q&A that followed was a sustained, pointed argument about where the secondary market is heading — and what practices it needs to leave behind.

Three themes emerged that every secondaries professional should sit with: the rollout of daily pricing across Apollo’s entire credit book, a direct attack on day-one markup accounting in evergreen funds, and a claim that the illiquidity premium — the spread investors demand for holding private assets — is set to narrow for anyone who doesn’t control origination.

DAILY PRICING: THE FULL ROLLOUT

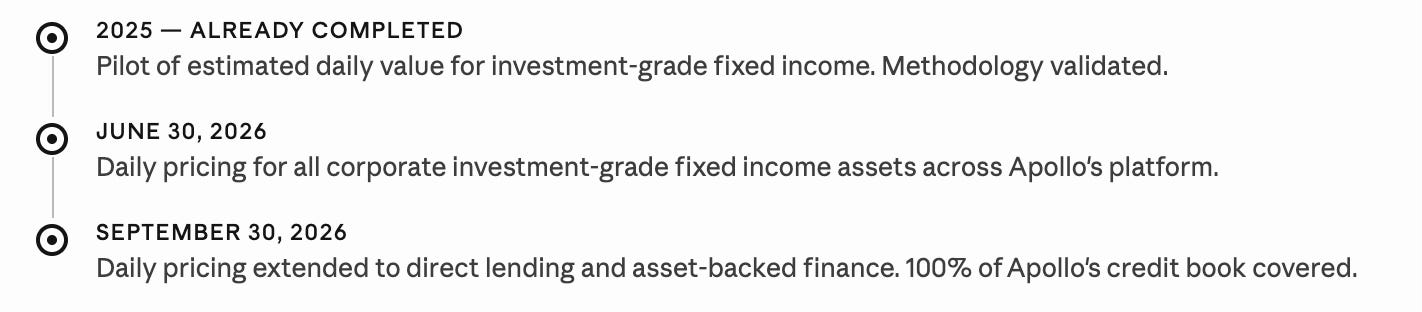

Apollo announced a concrete, dated schedule for daily NAV across its credit platform. This is not a pilot or a concept — it is a commitment with deadlines tied to the firm’s public reporting calendar.

The methodology mirrors how public asset managers set prices: observing actual trades, benchmarking against public market comparables, and incorporating broader market trends. Rowan was explicit that this is not an approximation — it is meant to produce prices equivalent to those seen in public securities markets.

“We will produce a price that is the same price in many instances that you see for public securities. And every day it gets better.”

— MARC ROWAN, CEO, APOLLO GLOBAL MANAGEMENT · Q1 2026 EARNINGS CALL

Why does this matter for secondaries? Because price discovery has always been the single biggest friction point in private credit secondary transactions. Buyers apply steep discounts not because they distrust the underlying credit — but because they distrust the valuation. Daily, observable, methodology-backed pricing compresses that uncertainty premium directly. Tighter uncertainty means tighter bid-ask spreads, faster deal execution, and higher volume.

MARKET-MAKING: $13B AND BUILDING

Apollo’s secondary trading platform for credit assets — launched from a cold start in 2025 — has now facilitated over $13 billion in trading volume with banks, asset managers, and institutional investors. Rowan described Q1 2026 as “exceptionally strong,” attributing the momentum to fund managers increasingly recognizing Apollo as the primary liquidity source for private credit assets.

Critically, Apollo is not trying to corner this market. Rowan said the firm created a shared data warehouse and made it available to all dealers — explicitly to create competition. The goal is not a captive marketplace but a standardized one,

“We’ve gotten the market going, but ICE IDs, data repositories, standardized data, and ultimately jealousy are going to cause market-making competition. No one wants to see Apollo earning widespread.”

The ICE partnership sits at the center of this standardization effort. Every private asset in Apollo’s portfolio will receive an ICE ID — potentially alongside a CUSIP — creating a common identifier layer that makes cross-platform comparison and trading possible at scale. This is the connective tissue that allows a fragmented secondary market to function like an actual market.

THE DAY-ONE MARKUP PROBLEM — ROWAN NAMES IT DIRECTLY

This is the passage most secondaries professionals will want to read twice. Rowan directly addressed the practice of marking up secondary positions on day one of acquisition — a common accounting approach where a newly acquired position is immediately written up to par or above, generating instant paper gains.

His argument is structural: in institutional closed-end funds, this practice was relatively harmless because investors couldn’t enter or exit on a short-term basis. In evergreen funds — where investors can receive liquidity quarterly — it creates real mispricing that affects the economics of everyone in the fund at the moment of any redemption.

“Across the totality of our one trillion dollar platform, secondaries that have been marked up round to zero. For the year of twenty twenty-five, revenue was sub three million dollars.”

— MARC ROWAN, CEO, APOLLO GLOBAL MANAGEMENT · Q1 2026 EARNINGS CALL

Apollo generated under $3M in revenue from day-one markups across its entire $1 trillion platform for all of 2025. Rowan called the practice economically incoherent for evergreen vehicles and said Apollo is part of an industry group actively working to change the accounting standard. The message to peers was unmistakable: this practice is ending, whether by consensus or by regulatory pressure.

THE ILLIQUIDITY PREMIUM — ROWAN’S MOST STRUCTURAL CLAIM

In the Q&A, Evercore asked the question that gets to the heart of the secondaries business model: if daily pricing and liquidity become standard, what happens to the illiquidity premium — the 150 to 200 basis points that investors currently demand for holding private assets?

Rowan’s answer was direct and worth reading in full context. He does not think the originator’s edge disappears. But he does think it migrates — away from the mere fact of illiquidity and toward the quality of origination and access to information.

“We do not view the illiquidity premium as the basis on which you get paid. It is what is currently demanded by investors for holding it. And yes, for the broader market that does not control origination, I expect that there will be a narrowing of spread.”

The implication for secondaries buyers is significant. If the illiquidity discount that creates the opportunity to buy at 70 narrows — because assets are priced more transparently and trade more frequently — then the return profile of secondaries funds that rely on that structural discount changes. The firms that will continue to generate alpha are those that can underwrite better, not just those that can absorb illiquidity longer.

THE END OF BUYING AT 70 AND WRITING UP TO PAR

Rowan’s closing statement on secondaries in the Q&A was the most pointed of the call. Asked whether daily pricing would eventually extend to hybrid and private equity assets, he said it would — but focused his answer on what daily pricing does to the secondary market’s traditional business model.

“In the secondaries market, I believe the days of buying something at seventy and writing it up to par are nearing the end. Ultimately, good investors should be able to make money in the secondaries market by superior underwriting and superior access to information.”

This is not a statement about the death of the secondary market. It is a statement about where the edge in the secondary market is moving. The structural discount — the gap between purchase price and theoretical par — has historically been as much a function of opacity and illiquidity as of genuine credit risk. As daily pricing erodes that opacity, the discount compresses, and the only durable source of alpha is what Rowan calls “superior underwriting and superior access to information.”

For the large secondaries platforms with deep sourcing networks and proprietary data — Ardian, Coller, Lexington, Pantheon — this framing is not a threat. It is a validation of their model. For smaller or less differentiated players who have relied on structural discount rather than genuine underwriting edge, it is a warning worth taking seriously.

WHAT TO WATCH

The June 30 and September 30 deadlines are now public commitments. If Apollo delivers, the pressure on competitors to follow — whether from LPs, regulators, or distribution channels — will be real. Rowan acknowledged that some peers are already “resisting this transparency,” which suggests the industry is not moving as a block. The gap between transparent and opaque managers is about to become observable in real time. That gap is, itself, a secondary market opportunity.

| A guest post by

|