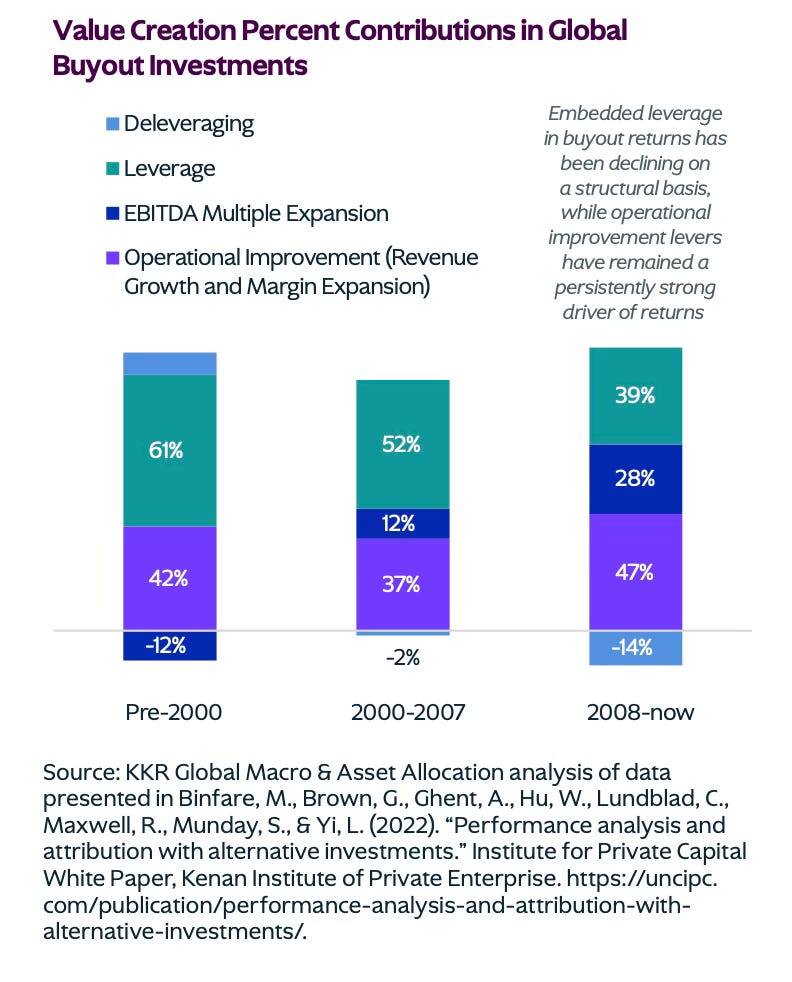

KKR’s mid-year outlook for 2026 — an 89-page macro report — doesn’t mention secondaries once. But buried in its asset allocation calls is one of the cleaner arguments we’ve seen for why GP-led volume should keep growing through 2027.

The setup is the 2021 vintage.

KKR flags it explicitly, and repeatedly, as the market’s most structurally compromised cohort. Deals underwritten at peak multiples, unusually low base rates, loose documentation, and revenue growth assumptions that no longer hold. Their words: transactions “structured for a world that no longer exists.” They expect fewer sponsor-to-sponsor deals from this vintage, and they’re watching defaults in private credit — by Fitch’s definition, which includes PIK and extensions — running around 5% since mid-2024.

This is the feedstock for the GP-led market.

When a GP holds a 2021-era asset that can’t trade at original underwriting assumptions, and traditional exit routes — IPO, strategic sale, sponsor-to-sponsor — are either closed or value-destructive, the continuation vehicle becomes the rational tool. Not distress. Portfolio management. The secondary market’s core thesis, playing out in real time.

KKR adds another layer. Their macro framework — what they call the “Divergence Conundrum” — describes an environment where growth and capital access are increasingly concentrated in fewer sectors. AI, national security, high-end services. Everything else faces what they characterize as rolling recessions. In that environment, a GP with a mixed 2021-era portfolio has a legitimate structural problem: some assets are compounding well, others are stranded. The continuation vehicle lets them separate the two. It’s not a workaround. It’s the correct answer.

There’s also a rate context worth noting. KKR expects the Fed on hold through 2026, with only one cut in 2027. Higher-for-longer isn’t the crisis scenario anymore — it’s the base case. For any sponsor still waiting for rate normalization to unlock exits or refinancing, the wait is getting longer. That pressure redirects toward solutions that don’t depend on a rate tailwind: NAV facilities, GP-leds, structured equity.

None of this is speculative. The conditions KKR describes — concentrated earnings, stalled exit markets, bifurcated credit, 2021 overhang — are the same conditions secondaries advisors have been navigating for the past 18 months. What the report provides is macro confirmation from one of the largest PE firms in the world, written for LPs and allocators.

The secondaries market doesn’t need KKR to validate it. But when a firm of that caliber publishes a 89-page outlook that inadvertently describes the structural case for GP-led supply growth, it’s worth reading between the lines.

The pipeline isn’t slowing down. The macro is building it.