Lazard Acquires Campbell Lutyens: A New Giant in Secondaries Advisory Is Born

The deal reshapes the competitive landscape of the private equity secondaries market and cements a new era of integrated advisors at global scale

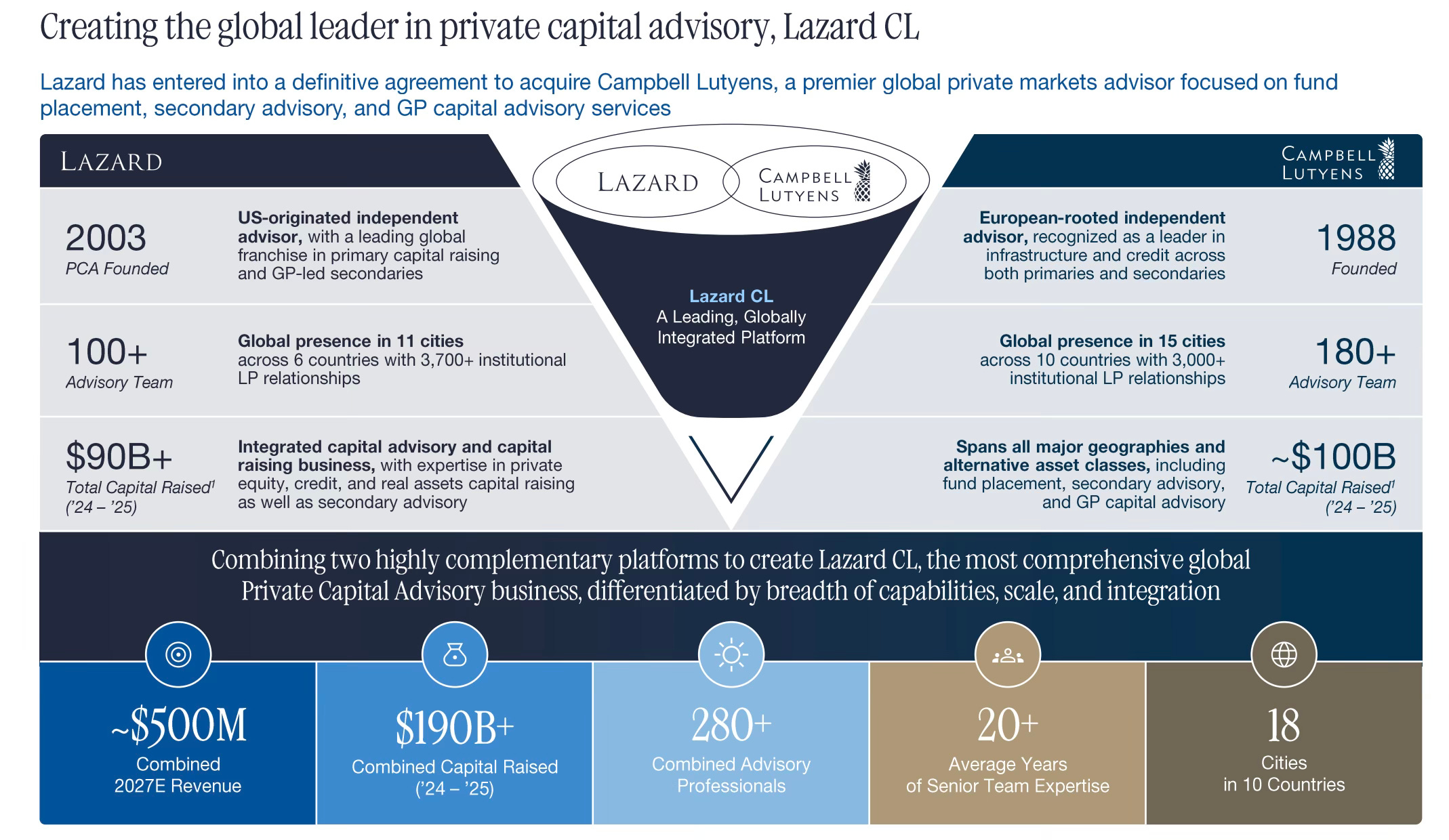

Lazard announced the acquisition of Campbell Lutyens for total consideration of approximately $575 million. The headline might read like a straightforward corporate consolidation play. But for those of us who follow the secondaries market closely, the significance runs much deeper: this is the clearest signal yet that secondaries have graduated from a specialized niche into one of the central pillars of the private markets industry.

Campbell Lutyens: A Secondaries Institution

Founded in 1988, Campbell Lutyens spent decades building a singular reputation in secondary transaction advisory. With more than 400 secondary advisory mandates and total transaction volume exceeding $175 billion, the firm became one of the first calls any GP or LP would make when navigating the complexity of a secondary transaction — whether a portfolio sale on the LP side or a GP-led process such as a continuation vehicle.

It is precisely in GP-led transactions — one of the fastest-growing segments across the entire industry — where Campbell Lutyens built its most distinctive edge. Its ability to structure these processes, manage the inherent conflicts of interest, and access the right institutional buyers gave it a differentiated position that few rivals have been able to match.

Add to that its track record in fundraising for secondaries strategies, advising some of the world’s most prominent funds in raising capital from institutional LPs across every major geography, and you have a firm that has shaped the secondaries market as much as it has served it.

What Lazard Brought to the Table

Lazard’s Private Capital Advisory (PCA) business, founded in 2003, arrived at this combination with its own secondaries credentials: more than $115 billion in total secondary transaction volume advised and over 130 mandates, with a particularly strong focus on GP-led secondaries. Lazard PCA stood out for its integration with the firm’s M&A and restructuring business, allowing it to offer GPs liquidity solutions as part of a broader strategic conversation.

What Lazard lacked, however, was meaningful capability in LP-led secondaries — the other major pillar of the market. That was, in a sense, the missing piece.

The Combination: Full Coverage of the Secondary Market

The capabilities matrix in the investor presentation says it all: while Lazard had an established presence in GP-led secondaries but no meaningful LP-led offering, Campbell Lutyens covered both segments with depth. The resulting entity, Lazard CL, will be one of the few advisors in the world capable of offering clients complete coverage across the secondary spectrum — LP portfolio sales, GP-led transactions (continuation vehicles, tender offers, strip sales), fund restructurings, and secondary advisory in infrastructure and private credit, two of the most dynamic asset classes in today’s secondary market.

In terms of combined scale, Lazard CL will be backed by more than $100 billion in secondary volume transacted over the past two years and a team of more than 280 professionals across 18 cities in 10 countries.

Why This Matters Right Now

The timing is no coincidence. The secondary market has been growing at an extraordinary pace for several years, with global annual volume estimates now exceeding $150 billion. The combination of a more normalized interest rate environment, a historic backlog of unrealized assets in LP portfolios, and the proliferation of continuation vehicles has elevated secondaries to a strategic priority for both GPs and investors alike.

In that context, specialized independent advisors have experienced extraordinary demand. But the market is also evolving: buyers are more sophisticated, transactions are more complex, and GPs increasingly demand advisors with genuine global distribution capacity — not just nominal offices in a handful of cities. Scale matters.

With this acquisition, Lazard CL positions itself to compete head-to-head with the biggest names in secondaries advisory — Evercore, Jefferies, Rede Partners — from a platform of capabilities, LP relationships, and geographic reach that would be nearly impossible for any independent boutique to replicate organically.

The Detail That Shouldn’t Be Overlooked: GP Capital Advisory

Beyond transactional secondaries, the combination adds another strategically important dimension: Campbell Lutyens launched its GP Capital Advisory practice in 2022, focused on advising managers on firm-level capital decisions — from minority stake sales to GP-to-GP mergers. With more than $200 billion in AUM advised and over 30 mandates, this practice reflects where the market is heading: GPs don’t just need liquidity solutions for their funds — they increasingly need capital solutions for their own balance sheets.

Pairing this capability with Lazard’s M&A network and restructuring advisory creates a genuine continuum of services across the complete GP lifecycle, from raising a first fund all the way through to a sale of the management company itself.

A Signal for the Broader Market

Consolidation among private markets advisors tends to anticipate major industry trends. This deal confirms that secondaries have matured into a business of sufficient scale to justify a $575 million bet by a firm of Lazard’s stature.

For LPs and institutional investors, Lazard CL presents itself as a one-stop advisor capable of addressing virtually any secondary liquidity need, regardless of the underlying asset class or geography. For GPs, the promise is even more ambitious: an advisor that can walk alongside them from primary fundraising through mid-life liquidity solutions and all the way to firm-level capital decisions.

The secondary market just had its corporate deal of the year. And it probably won’t be the last.

| A guest post by

|