The pure-play advisory boutique reported record first-quarter revenues, with Private Capital Advisory (PCA) emerging as one of its two key growth drivers. Here's what it means for the secondaries market — and why a firm with no AUM might be one of the most important players in it.

What Is Moelis?

Moelis & Company (NYSE: MC) is a pure advisory investment bank. It has no AUM, no balance sheet deployed in transactions, no proprietary funds, and no debt. It earns fees exclusively from advice. Founded in 2007 by Ken Moelis — a veteran of UBS and the late Drexel Burnham Lambert — the firm went public in 2014 and has since grown into one of the most respected independent advisory boutiques globally, with 1,440 employees across 23 offices in 45+ countries and 179 Managing Directors as of March 2026.

That capital-light, conflict-free model is not incidental to its secondaries ambitions — it’s the whole point. When a GP selects an advisor for a continuation vehicle, they need someone who can credibly represent their interests to LP voters and secondary buyers without any competing agenda. Moelis has no fund on the buy side. No balance sheet taking a position. No asset management arm with its own carry dynamics. Just advice.

Its four business lines are:

M&A and Strategic Advisory — its largest product, covering sell-side, buy-side, divestitures, carve-outs, special committee advisory, and fairness opinions. Over $2.6 trillion in transaction volume and 1,500+ deals since IPO.

Capital Structure Advisory (CSA) — restructuring, liability management, debt exchanges, and balance sheet optimization. Ranked top 3 globally for completed restructurings between 2021–2025, with roughly $1 trillion in liabilities restructured since IPO.

Capital Markets — equity and debt capital raising, IPOs, PIPEs, convertibles, private placements, and direct lending advisory. Approximately $230bn raised for clients since IPO.

Private Capital Advisory (PCA) — the newest and fastest-growing unit, covering GP-led secondaries, LP liquidity solutions, tailored capital raise (co-investments, NAV loans, preferred equity), and primary fund placement.

In Q1 2026, the firm posted total revenues of $319.8 million — a record for any first quarter in its history. The business mix was approximately two-thirds M&A and one-third non-M&A, with that non-M&A third shared between CSA, Capital Markets, and PCA. Moelis does not break out revenue by product line, so the exact contribution of PCA — let alone secondaries specifically — is not publicly disclosed. What is clear is that secondaries represents a growing fraction of that non-M&A third, and management’s commentary suggests it’s punching above its weight in terms of strategic priority and pipeline momentum.

Last Twelve Months revenue through Q1 2026 stands at $1.53 billion, and the firm has returned approximately $3.2 billion to shareholders since its IPO through dividends and buybacks — all of it generated from fees, with no balance sheet risk.

Q1 2026: Private Capital Advisory as a Growth Driver

Moelis posted record Q1 2026 revenues of $319.8 million, up 4% year-over-year — and if you read between the lines of the earnings call and the investor presentation published alongside the results, the secondaries business had a lot to do with it.

CFO Christopher Callesano attributed the revenue increase to higher M&A and Private Capital Advisory revenue, partially offset by declines in capital structure advisory and capital markets. In a quarter where two of four product lines declined, PCA pulling in the same direction as M&A is a meaningful signal about where the firm’s growth is coming from.

GP-Leds at the Center

CEO Navid Mahmoodzadegan was explicit on the earnings call: the GP-led secondaries market is hitting record levels, driven by demand for liquidity solutions, the growing adoption of continuation vehicles, and an expanding base of institutional investors seeking exposure to seasoned assets. He said Moelis’s PCA “thesis is playing out as expected,” with live mandates and a rapidly building pipeline.

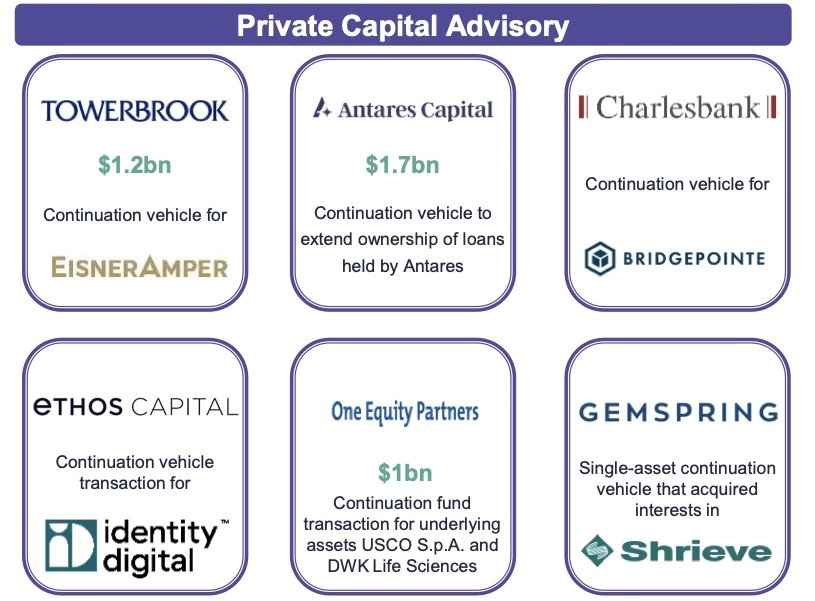

That thesis has been years in the making. The investor presentation shows the PCA team now maintains over 1,500 global LP relationships and has advised on more than $75 billion in private capital — a figure that includes experience at prior firms but reflects the caliber and network of the senior team. Average experience per Managing Director in PCA exceeds 20 years.

The recent deal track record in secondaries skews heavily toward GP-led structures, specifically continuation vehicles:

Every one of these is a GP-led, and several are single-asset or concentrated structures — the most complex and highest-fee end of the secondaries spectrum. Notably absent from the list: LP-led portfolio sales. Moelis is not positioning itself as a portfolio brokerage shop. Its secondaries identity is firmly in the GP-led, structurally complex, advisor-as-fiduciary lane.

How Big Is the Secondaries Business at Moelis?

The honest answer: we don’t know precisely, and Moelis doesn’t tell us.

The firm reports a single consolidated revenue line with no product-level breakdown. In Q1 2026, total non-M&A revenue was approximately $106 million (one-third of $319.8mm). That bucket is shared by Capital Structure Advisory, Capital Markets, and PCA. Within PCA, secondaries competes for revenue with primary fundraising and tailored capital solutions like co-investments and NAV loans. So secondaries is a fraction of a third — real and growing, but not yet a standalone reportable segment.

What we can infer from the hiring data is instructive. Mahmoodzadegan confirmed on the earnings call that Moelis is building toward seven senior bankers dedicated specifically to GP-led secondaries — with a recent MD hire focused on private credit secondaries and another expected to join later in 2026. For context, the investor presentation shows that PCA led all product categories in recent MD additions: six new managing directors between 2023 and year-to-date 2026, ahead of M&A (six), Capital Markets (five), and Capital Structure Advisory (four).

Building Into Private Credit Secondaries

The expansion into private credit secondaries deserves its own paragraph. Moelis’s PCA platform already covers GP-led equity continuation vehicles across buyout, growth equity, and real assets strategies. Adding a dedicated MD for credit secondaries signals that the firm sees the next wave of secondary activity moving beyond PE portfolio management and into credit portfolios — direct lending books, CLO equity, private credit fund stakes — a market that remains earlier-stage but is attracting serious capital from buyers globally.

The timing makes sense. As direct lenders face increasing pressure from portfolio concentration, vintage clustering, and the AI-driven repricing of software credit (a theme Mahmoodzadegan discussed at length on the call), the secondaries market for credit assets is likely to deepen. Having a dedicated banker in place before that wave fully arrives is a classic Moelis move — patient, talent-forward, organic.

The Macro Backdrop Is Working in Their Favor

The conditions Mahmoodzadegan described on the earnings call are essentially a structural tailwind for GP-led secondaries advisory. Sponsors are sitting on a large backlog of investments that need to be monetized, but the traditional exit channels — IPOs and strategic M&A — remain partially constrained by macro uncertainty, public equity volatility, and geopolitical friction. When the exit window is partially closed, continuation vehicles become the liquidity mechanism of choice for GPs who believe in their assets but need to give LPs an off-ramp.

Mahmoodzadegan also flagged that disruptions in private credit and AI-driven sector dislocation are creating near-term headwinds in parts of the market — while simultaneously noting that these forces “create new opportunities.” For secondaries advisors, that’s not spin. Dislocated GPs managing overlevered software portfolios, navigating lender selectivity, or simply trying to buy time for value creation need creative liquidity solutions, and Moelis is positioning itself as the firm that can structure them — especially when the same transaction might involve elements of capital structure advisory, a NAV facility, and a GP-led secondary all at once.

Why Independent Advisory Wins in GP-Led Secondaries

There’s a structural reason why a pure-play advisory firm is well-positioned to win in GP-led secondaries, and it comes back to Moelis’s fundamental business model.

Unlike bulge-bracket banks that might have asset management arms or proprietary funds competing for the same assets, and unlike secondary funds that are on the buy side, Moelis sits exclusively on the advisory side. Its PCA offering spans Secondary Market Advisory (continuation funds, LP liquidity, equity recaps, NAV loans and preferred equity), Tailored Capital Raise (co-investments, managed accounts, seeded fundraises, stapled primaries), and Primary Fundraise placement. The breadth of that platform means Moelis can advise a GP across the full capital lifecycle — not just when they need a continuation fund, but when they’re raising their next primary too. That continuity of relationship is where advisory firms build durable competitive moats.

The firm ended Q1 2026 with $354 million in cash, no debt, and a strong balance sheet. It returned approximately $171 million to shareholders in the quarter — $0.65 per share in regular dividend plus open-market buybacks. That capital discipline, combined with 400%+ total shareholder return since IPO, suggests the firm has the financial stability to continue investing patiently in PCA without needing the business to immediately carry its own weight.

What to Watch

The pipeline is near all-time highs across the firm, according to Mahmoodzadegan. If a meaningful portion of that pipeline reflects GP-led secondary mandates — and the hiring trajectory suggests it does — then Q2 and Q3 2026 could be the quarters where Moelis’s PCA bet starts showing up more visibly in the revenue line.

The private credit secondaries buildout is the longer-dated but potentially larger opportunity to track. And the question of whether Moelis will eventually break out PCA as a disclosed revenue segment — giving the market a clearer view of the business — is worth watching as the unit scales.

For those tracking the secondaries advisory landscape, Moelis is no longer a peripheral player experimenting with the product. With seven dedicated senior bankers in GP-led secondaries, a string of marquee continuation vehicle closes, an expansion into private credit secondaries, a $75bn+ advisory track record in PCA, and explicit CEO commentary that the thesis is playing out — Moelis has made its position clear.

The question now is execution at scale. And the ingredients — talent, relationships, platform, and conflict-free positioning — are all in place.

Secondary Scoop covers the global market for private equity, venture capital, and private credit secondaries, including GP-led transactions, LP portfolio sales, and fund restructurings.

| A guest post by

|