Multi-Track or Bust: Asante's Pitch for Why Every GP Needs a Secondaries Arm

Asante's Q2 Pulse argues secondaries have become non-negotiable, and a fresh Hong Kong hire suggests the firm is staffing up to match its own thesis.

Every placement agent needs a narrative for why the market has changed just enough to require its services. Asante Capital Group’s Q2 2026 Market Pulse delivers exactly that: fundraising, the report argues, is no longer a single-track exercise anchored around a flagship vehicle. It is now an “integrated dialogue” spanning primaries, co-investments, secondaries, and continuation vehicles, and GPs that can’t offer all four are losing share of wallet to those that can.

The data agrees with the incentive

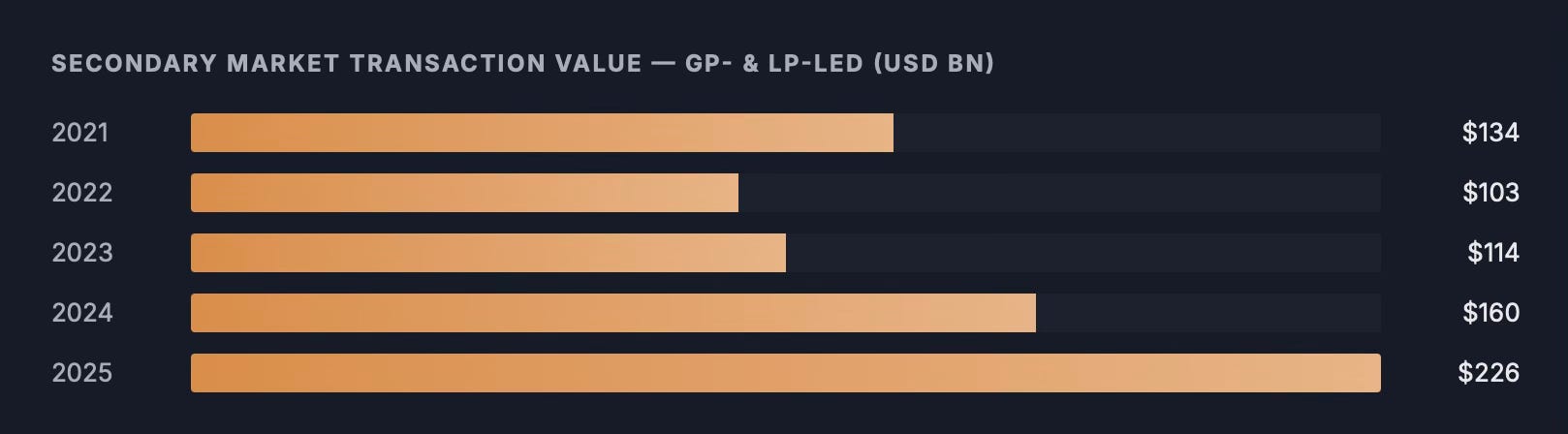

Asante puts 2025 secondary transaction value, combined GP- and LP-led, at an all-time high, citing Kroll’s March 2026 assessment of continuation funds as a viable exit alternative. That figure represents 69% cumulative growth since 2021, a roughly 14% compound annual rate. Co-investment capital raised followed a choppier path, peaking above $30 billion in 2021 before dropping to $15.9 billion in 2024 and rebounding to $25.3 billion in 2025, a reminder that “multi-track” has not meant uniform growth across every track, only that the tracks have become interdependent.

What is more interesting than the volume figure is what Asante says is driving it. The report identifies DPI as having “firmly overtaken IRR and TVPI as the metric of primary focus” in re-up conversations, no longer a preference, but a prerequisite. That is a significant claim from an advisor embedded in live fundraising processes across three continents, and it aligns with what Secondary Scoop has argued since this platform’s founding: secondaries are not a distress signal. They are the mechanism by which a DPI-starved LP base gets paid, and increasingly the mechanism GPs build into fund strategy from day one rather than reach for defensively.

“Liquidity is no longer a preference. It is the prerequisite that frames every allocation decision.”, Asante Capital Group, Q2 2026 Market Pulse

Reading the advisor’s arithmetic

Asante’s own “unforgiving arithmetic” chart is worth sitting with. GPs and strategies in market are rising; available LP capital is tightening. That gap is precisely the gap an advisory platform is paid to help GPs navigate, and it is also precisely the gap that has pushed fundraising timelines from an average of 14 months in 2000 to 30 months through 2026 year-to-date, per the Buyouts Fundraiser Report data Asante cites. A GP staring down a 30-month close has every incentive to diversify its capital-raising toolkit, and every incentive to pay an advisor to help it do so.

None of this makes the underlying liquidity constraint fictional. Distributions remain below historical norms; LPs are holding aged, unrealised portfolios; and the denominator effect has left many overcommitted relative to their own pacing models. Asante’s report is honest about naming secondaries as a “core liquidity management instrument” rather than an opportunistic one, language that mirrors, almost exactly, how GPs and LPs alike have described the shift over the past eighteen months in earnings calls and barometer surveys across the market.

The advisor is staffing up to match the thesis

Asante’s own hiring backs up the argument, if not always the framing. The firm has just added Robin Seng as a Managing Director in its Hong Kong office, joining the Secondaries team after more than a decade advising on secondary transactions across Asia, most recently as part of the senior team at Evercore. His mandate covers GP- and LP-led transactions, with particular depth in continuation funds and LP-led liquidity solutions, the same two structures the Market Pulse names as central to its “multi-track” thesis.

PERSONNEL MOVE

Robin Seng joins Asante Capital Group as Managing Director, Hong Kong, on the firm’s Secondaries team. He previously spent over a decade advising on secondary transactions across Asia, most recently with the senior team at Evercore, working with institutional investors on complex GP- and LP-led deals with a focus on continuation funds and LP-led liquidity solutions.

Read alongside the Market Pulse, the hire is less a footnote than a data point in its own right: an advisor betting headcount on the same regional growth story it is telling clients. Asia-based continuation fund and LP-led activity has been thinner than the North American and European markets Secondary Scoop covers most closely, and a senior Evercore hand relocating to build out that coverage is a reasonable signal that the region’s deal flow is catching up, regardless of what the accompanying quarterly commentary chooses to emphasize.

Where the framing gets ahead of the evidence

The claim that multi-track strategies will become “standard practice, not optional” is a forecast, not an observed outcome; Asante’s own co-investment fundraising data shows meaningful volatility year to year, not a smooth institutionalization curve.

“Seeded and warehoused portfolios” are presented as a third emergent pillar alongside secondaries and co-investment, but the report offers no volume data for this category, an asymmetry worth noting when the other two pillars are quantified in detail.

The report’s framing treats intermediated access as an unambiguous LP benefit (”curation and diligence... difficult to replicate internally”) without acknowledging that intermediation also layers additional fees onto an already fee-sensitive LP base focused on net DPI.

Some Extra Thoughts

Placement agent research occupies an odd space in the secondaries commentary landscape. It is closer to the ground than most bank research, Asante is in fundraising rooms, not just modelling from Preqin data, but it is also structurally incapable of concluding that GPs should do less capital-raising, or that fewer intermediaries would serve LPs better. Treat the pattern-recognition as useful and the prescription as self-interested.

The more durable takeaway sits underneath the advisory framing: DPI has become the currency LPs actually transact in, and secondaries are how GPs mint it when the traditional exit channel won’t cooperate. That is not a new observation on this platform. What is new is watching a placement agent build its entire quarterly pitch around the same thesis, which suggests the “secondaries as portfolio management tool” argument has moved from contrarian to consensus faster than even we expected.

Sources: Asante Capital Group, “Q2 2026 Market Pulse” (July 2026), citing Kroll (”Secondary Market Evolution: Continuation Funds Emerge as a Viable Alternative to Traditional Exits,” March 2026), Preqin (May–June 2026), and Buyouts’ Fundraiser Report. Secondary Scoop’s analysis and framing are its own.