PJT Park Hill: The Secondary Market as a Relief Valve in an Uncertain Environment

GPs cannot rely exclusively on IPO exits or sponsor-to-sponsor M&A processes to return capital to their LPs. They need what Chairman and CEO, Paul Taubman, called a “third way.”

PJT Partners’ Q1 2026 results left little room for doubt: revenues of $418 million, up 29% year-over-year, with expanding margins and a mandate pipeline at record levels. But beyond the headline numbers, what is truly revealing for those of us who follow the secondary market is the narrative that Paul Taubman, Chairman and CEO, constructed throughout the earnings call.

The Secondary Market as a Necessary “Third Way”

Taubman was unequivocal in describing the current market moment: GPs cannot rely exclusively on IPO exits or sponsor-to-sponsor M&A processes to return capital to their LPs. They need what he called a “third way.” And that third way, in the current context, has a name: the secondary market.

The argument is as mathematical as it is strategic. The capital distribution plans that managers set at the start of 2026 have had to be revised. Assets that were on the monetization list have come off it, and in order to maintain their targeted pace of capital returns to LPs, managers are increasingly turning to alternative liquidity solutions.

GP-Leds as the Primary Driver, LP Secondaries Growing

On the earnings call, Taubman was direct about where the traction is right now: the real growth driver in the current environment is on the GP side. Continuation vehicles and other GP-led structures are the most immediate response to the liquidity pressure facing asset managers with positions that are difficult to monetize, particularly in the software sector.

That said, the firm is also pointing to growth in LP portfolio sales, driven by a different dynamic: LPs themselves are rethinking how to manage their commitments and rebalance their portfolios in a more volatile environment. Taubman confirmed growing interest in LP sales as well, though he was clear that the GP side remains the primary engine for now.

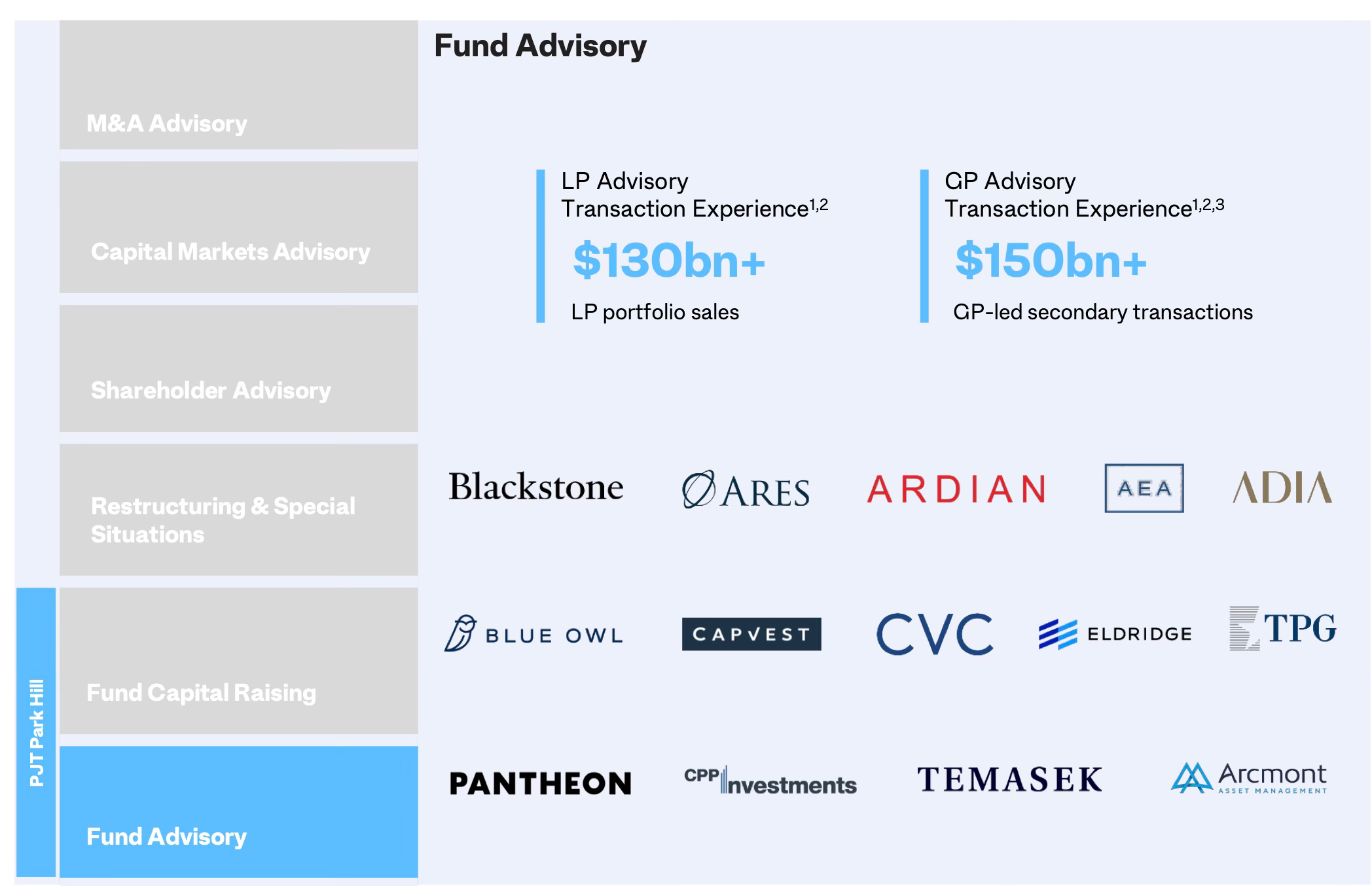

The cumulative volume that PJT Park Hill reports in its Fund Advisory division speaks for itself: more than $130 billion in LP portfolio sales and more than $150 billion in GP-led secondary transactions since 2010, according to the investor presentation.

Software: The Elephant in the Room for Continuation Vehicles

One of the most pointed questions of the call was whether the valuation challenges in the software sector were dampening GP-led continuation vehicles, where that segment had historically been very active.

Taubman’s answer was nuanced but revealing. The debate around software is no longer about short-term cash generation — it is about the terminal value of these businesses. GPs with significant software exposure are seeking liquidity in other parts of their portfolios where visibility is clearer, creating an interesting flow of secondary opportunities away from the software noise.

In a world where many of these companies were financed in the credit markets against a loan-to-value mindset, uncertainty about long-term value makes refinancing the entire capital stack more difficult without further equitization or other catalysts. This dynamic is already beginning to bleed into the credit markets through liability management activity — less about near-term fundamentals and more about quantum of debt and whether the existing capital structure is appropriate given the questions about long-term value.

The Virtuous Circle of Secondaries as an Asset Class

Perhaps the most significant takeaway for the secondary market community was Taubman’s long-term thesis. The biggest constraint on secondary market growth has not been lack of demand from GPs or LPs seeking liquidity — it has been the ability to execute transactions at scale with adequate competitive tension. And that requires more capital allocated to secondary funds as an asset class.

The investment case for LPs considering increased exposure to secondaries remains compelling: better matching of commitment and investment, no J-curve, a clear operating history and track record for the underlying asset, continued sponsorship from the manager, and historically strong returns. The more secondary investor appetite grows, the more secondary activity can be unlocked — and according to Taubman, that virtuous circle is already in motion.

The Macro Context: Volatility as a Catalyst

The primary fundraising market continues to face headwinds. PJT Park Hill’s revenues in that segment were down year-over-year, with the growth in Private Capital Solutions — the secondary advisory business — more than offsetting the primary fundraising decline, a dynamic Taubman described as likely to persist. For 2026, the firm expects primary fundraising revenues to broadly match prior high-water marks, while the secondary market is positioned for another year of robust growth as rising demand from both GPs and LPs for liquidity solutions is matched by growing secondary investor appetite.

When IPO markets are closed and strategic buyers are in a wait-and-see mode, the secondary market is not the backup plan. Increasingly, it is the primary one.

| A guest post by

|