Schroders: Continuation Vehicles Aren't Just Growing Anymore. They're Displacing Secondary Buyouts.

For most of the last three years, continuation vehicles have been described the same way: a fast-growing addition to the private equity exit toolkit, expanding alongside traditional sales rather than at their expense. Schroders Capital’s latest annual research paper on the segment, published in June, breaks with that framing. For the first time, a major CV-focused study puts a specific figure on displacement: how much deal flow continuation vehicles are pulling directly away from secondary buyouts, the sponsor-to-sponsor sales that have anchored mid and large buyout dealmaking for two decades.

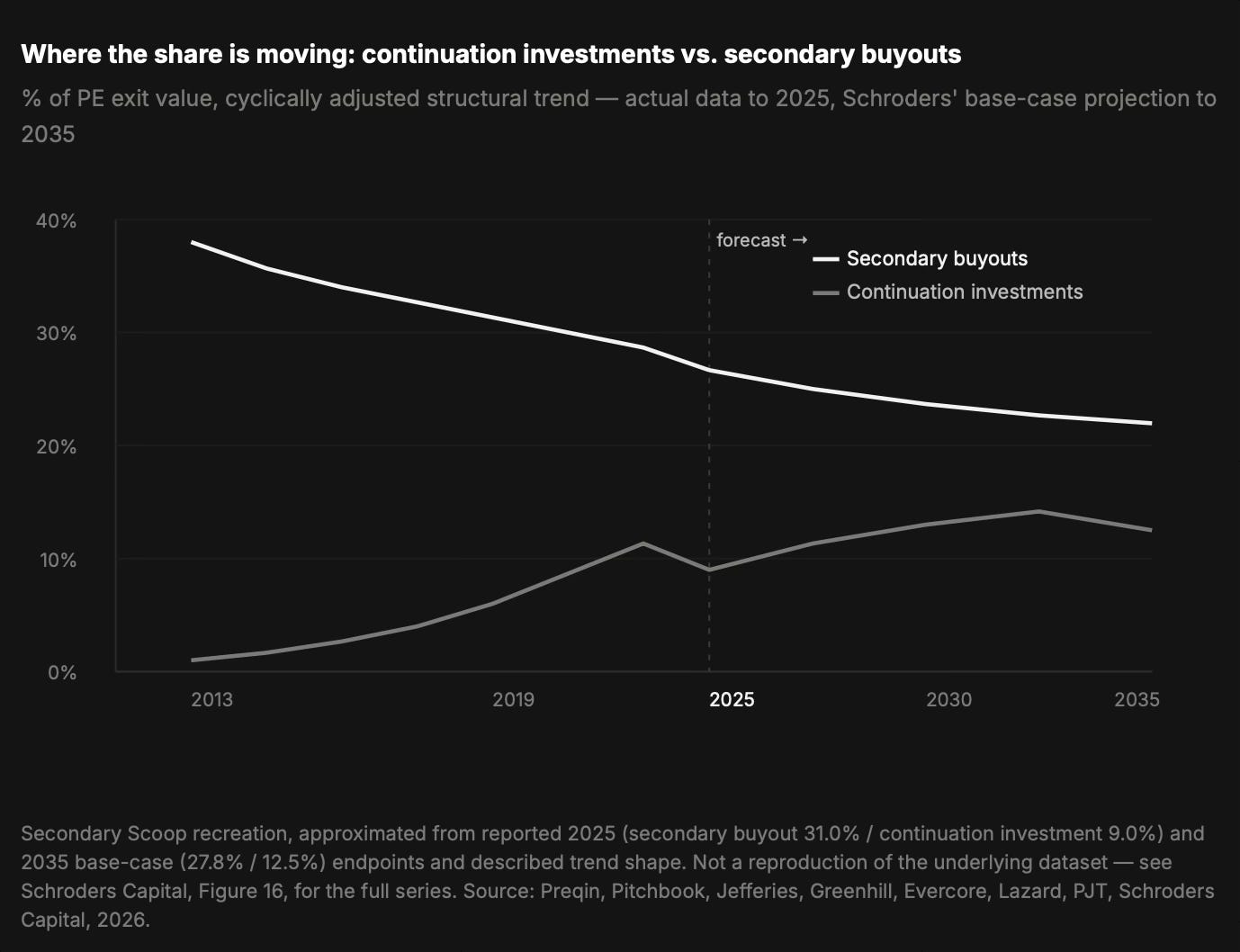

The number: 5% of mid/large buyout deal flow, gone within a decade

Secondary buyouts, one fund manager selling a portfolio company to another, have averaged 36% of exit value over the past 20 years and sat close to 40% in 2025. Schroders’ base case has continuation investments rising from 9% of total private equity exit value in 2025 to 12.5% by 2035. Critically, the firm models that entire increase as coming directly out of the secondary buyout share, which it forecasts falling from 31% to 27.8% over the same period. Since secondary buyouts have represented roughly half of new deal sourcing for mid and large buyout managers over the past decade, Schroders translates that shift into a headline estimate: about 5% of total mid/large buyout deal flow will be displaced over the next 10 years, relative to where it would otherwise sit.

“The most significant disruption is not in the concept of holding companies for longer under private equity ownership, but rather in who retains ownership.”

SCHRODERS CAPITAL, KEY TAKEAWAYS, JUNE 2026

That reframes the competitive stakes considerably. Companies staying in private equity hands for longer isn’t new, sponsor-to-sponsor deals have done that for two decades. What’s being modeled now is a reallocation of control: away from the buyer-side manager who would previously have won the next auction, and toward the incumbent GP working alongside a lead underwriter instead. It is the first time this has been expressed as a number rather than a general trend.

HOW THE ESTIMATE IS BUILT

The 5% figure rests on three assumptions holding simultaneously: that trade sale and IPO share of exits stays roughly flat, that continuation investment share keeps climbing from 9.0% toward 12.5% by 2035, and that secondary buyouts continue to represent about half of mid/large buyout deal sourcing. None of those assumptions are unreasonable on their own, but none are independently stress-tested, worth treating as a modeled estimate rather than an observed trend.

Why the growth looks structural rather than cyclical

Schroders’ own data shows 2025 volumes coming in ahead of what the firm projected a year earlier, $109bn against a revised 2024 base of $76bn, while the cyclical share of that growth actually fell, to 9% in 2025 from 14% in 2024. In other words, even as exit markets show early signs of recovery, continuation investment growth is becoming less dependent on distressed conditions, not more.

That lines up with what limited partners themselves are now saying. Coller Capital’s Summer 2026 Global Private Capital Barometer, surveying 108 LPs overseeing roughly $2 trillion in assets, found that 69% expect CV activity to hold or increase even if traditional exit channels fully recover; only 31% expect a decline. Coller’s data points to a structural mismatch behind that expectation: LPs disagree among themselves about the right holding period for any given asset, with 39% saying GPs aren’t providing liquidity early enough and 22% saying trophy assets are being sold too soon. Continuation vehicles resolve that tension by letting a single GP decision, hold the asset, accommodate LPs who want to exit and LPs who want to keep their exposure, simultaneously.

The “GP-led secondaries” label is a misnomer, Schroders argues

The paper also makes a pointed case against a piece of market shorthand: the term “GP-led secondaries,” often used interchangeably with continuation investments. Schroders argues this creates real confusion, for three reasons: fund managers typically retain (and often increase) their interest in the underlying company rather than crystallizing carry the way a genuine exit would require; these deals usually include a primary component of fresh capital rather than being a pure ownership transfer; and it is the incoming lead underwriter, not the GP, who structures the deal and runs full due diligence.

“When continuation investments are described as ‘private equity selling to itself,’ this is exactly not what these transactions are about,” the paper states. Ares Management has made a related argument in its own recent research, framing GP-led deals as private markets alpha against LP-led “beta,” and pointing to a specific mechanical source of that alpha: continuation vehicle pricing is typically locked at the signing date rather than at closing, so any value the company creates in the months between signing and close, revenue growth, multiple expansion, debt paydown, accrues to the incoming buyer rather than the seller. It’s a structural return enhancement that doesn’t show up in the initial underwriting model.

New data points worth tracking

31% of realized buyout portfolio companies are statistical candidates for continuation investments, according to Schroders’ analysis of roughly 2,600 realized deals in its own database, using a return-multiple threshold (2x TVPI) typical of sponsor-to-sponsor and CV target returns.

$5.7bn in estimated annual fee savings for investors, based on 2025 volumes: continuation vehicle management fees run at roughly half the level of traditional buyouts, with more tiered carried interest.

A 1.5-year shorter holding period for continuation investments versus traditional buyouts, based on Schroders’ own sample of 91 completed CV exits against 72 buyout co-investment exits. Worth flagging: the paper’s executive summary describes this as “about 25% shorter holding periods,” while the body text calculates a 35% faster time-to-liquidity from the same underlying gap, the two figures aren’t quite consistent with each other.

A third-party return study from Evercore, covering 387 continuation funds formed between 2018 and 2024, found returns broadly comparable to traditional buyout funds but with lower dispersion, external support for the “more predictable returns” case that doesn’t rely solely on Schroders’ own deal data.

The case for the lower mid-market, updated for a more volatile world

Schroders continues to argue that small and mid-sized buyout companies, those with enterprise values below roughly $1bn, offer the most attractive continuation opportunities, citing lower entry multiples (up to 40% below large-cap buyouts, up to 55% below Russell 2000 peers), a wider set of exit routes, and greater potential for operational transformation. This year’s paper adds a timelier justification: geopolitical insulation. Citing “the latest conflict in the Middle East and related energy price shock,” the firm argues that smaller, more domestically-focused, services-weighted portfolios are less exposed to the trade and geopolitical tensions currently driving market volatility. Private equity-backed companies generate about 90% of revenue domestically compared with 60% for public companies, and PE portfolios run roughly 83% services versus 17% goods, compared with a near-even split for the MSCI index.

A STRUCTURAL IDEA ALREADY TAKING SHAPE ELSEWHERE

Schroders also floats what it calls “hybrid continuation investment” structures, an incumbent GP retaining control of a company’s transformation while a second fund manager takes a partial stake to contribute a specific capability, such as regional expansion or IPO preparation. Jasmin Capital’s most recent market newsletter describes a similar structure already in use, sometimes called a co-control continuation vehicle: 50% of a company is sold to a new sponsor through a competitive M&A process, and the remaining 50% is rolled into a continuation vehicle managed by the incumbent GP at the price set by that process. It’s a genuine innovation worth watching either way, the concept of splitting control between an exiting-price-setting sponsor and a continuing incumbent may be more consequential than either single research note suggests on its own.

THE BIGGER PICTURE

Taken together, the data points in the same direction: continuation vehicles have moved past the stage of proving they’re a permanent feature of private equity, and into the stage of reshaping who competes for deal flow and on what terms. The next fight isn’t over whether CVs are legitimate. It’s over governance standards that can keep pace with a market growing this fast, and over which managers — buyout sponsors, secondary buyers, credit specialists — end up controlling the assets that used to change hands through a simple sale.

Sources: Schroders Capital, "Continuation investments continue to grow – and to reshape the buyout market," In Focus, June 2026 (Nils Rode, Petr Poldauf, Eufemiano Fuentes Perez). Coller Capital, Global Private Capital Barometer, 44th Edition, Summer 2026. ILPA, 2026 Continuation Vehicle Guidance (comment period draft). Ares Management, "Why Now for GP-Led Secondaries," June 2026. William Blair Private Capital Advisory, Q2 2026 Quarterly Newsletter. Jasmin Capital, Newsletter N°13/2026. Underlying market data via Preqin, Pitchbook, Jefferies, Greenhill, Evercore, Lazard and PJT.