Secondaries Aren't the Symptom of PE's Slowdown, They're the Adjustment Mechanism

Ropes & Gray's midyear global private capital report frames 2026 as a market in "recalibration," not recovery.

Ropes & Gray’s Cautious Optimism: How Private Equity Is Navigating a New Era of Uncertainty, a midyear update to the firm’s 2025 European private capital research, built on partner and client interviews conducted between April and June 2026, lands on a single word to describe the state of the market: recalibration. Not retreat, not recovery. A market where capital is available and confidence holds, but where the mechanisms for deploying and realizing that confidence have become slower, more selective, and more structurally complex.

Read the report’s six themes side by side, and secondaries stop looking like a standalone chapter. They show up as the load-bearing element connecting regulatory drag, LP/GP tension, and the exit environment into a single story. That’s worth unpacking on its own terms, because it’s a cleaner articulation of the “secondaries as portfolio tool, not distress signal” thesis than most sell-side research manages, coming, notably, from a law firm rather than a placement agent or GP.

The Causal Chain the Report Draws, Whether It Means To or Not

The report’s own throughline is explicit in its regulation section: as regulatory regimes overlap and slow deal execution, the EU’s Foreign Subsidies Regulation now “actively enforced” alongside antitrust and FDI screening, U.S. antitrust posture shifting under new FTC/DOJ leadership even as SEC enforcement pulls back, the practical challenge stops being just getting deals done and becomes realizing value at all. That, the report argues, is precisely why the industry has turned “with greater conviction to secondaries and continuation vehicles.”

That’s a meaningful sentence to get from a law firm. It reframes secondaries not as a workaround born of weak exit markets, but as the direct downstream consequence of a regulatory environment that Ropes & Gray’s own partners describe as adding cost and complexity to deal execution across jurisdictions.

EXPLAINER — WHY REGULATION FEEDS SECONDARIES VOLUME

Every layer of regulatory review — antitrust, FDI screening, subsidy control — adds time and uncertainty to a traditional M&A or IPO exit. When timelines stretch and outcomes become harder to underwrite, GPs holding high-conviction assets increasingly choose to extend ownership through a continuation vehicle rather than force an exit into unfavorable conditions. The CV isn’t a consolation prize; it’s a way to keep control of the value-creation story while sidestepping regulatory friction on a sale to a third party.

Structural, Not Cyclical, But Worth Stress-Testing

The report’s most load-bearing claim is that secondaries growth is structural rather than cyclical: GP-led continuation fund volumes hit record levels in 2025 despite an M&A and IPO environment that was, by the report’s own account, improving. Global secondaries transaction values reached $240 billion in 2025, up 48% year over year, and that growth held even as traditional exit routes opened up somewhat.

That’s the crux of the “portfolio tool, not distress signal” argument in data form, volume kept climbing precisely when it should have softened if secondaries were purely an exit-of-last-resort mechanism. It’s a genuinely useful data point for the thesis. It’s also an interpretive claim doing a lot of work on the back of one law firm’s client interviews rather than a broad market dataset, and it’s worth checking against Coller Capital’s Barometer or Jefferies’ own volume data before treating it as fully settled.

“If GPs still see strong growth potential, it is a sector and theme they still have conviction in, and they don’t believe there’s a better asset to acquire in that space — then it makes sense to retain that asset within their platform... rather than exit.”Elizabeth Todd, Partner & Co-Lead of European Private Equity Transactions Practice, Ropes & Gray

That’s about as direct a practitioner articulation of the conviction-driven CV as you’ll find outside a GP’s own investor letter, and it comes from the deal lawyer sitting across from the negotiation, not from a party with an economic stake in the transaction itself.

Where the Report Puts Secondaries Under the Microscope

The report doesn’t let secondaries off easy, either. Its LP/GP tensions section is the sharpest part of the analysis, and it’s where the “mainstream tool” framing meets its most serious friction: the GP frequently sits on both sides of a continuation vehicle transaction, and that structural conflict is drawing heightened LP scrutiny on process, pricing, and disclosure. The report notes this has, “in a handful of cases,” already produced litigation, a detail that deserves its own follow-up rather than a passing mention.

WHAT “GOOD PROCESS” LOOKS LIKE, PER STEVE ZAORSKI (ROPES & GRAY, NEW YORK)

A competitively priced GP-led process run through a formal auction led by a reputable placement agent

Independent validation by a third-party valuation provider

True optionality for LPs, a genuine choice between selling out or rolling into the new vehicle, not a soft push toward rolling

A meaningful GP commitment: typically a full roll of the GP’s own capital and carry on the asset into the CV

A specific value-creation plan and timeline for the asset’s next phase

An LP Advisory Committee genuinely empowered to vet conflicts of interest, not a rubber stamp

That checklist is a useful diagnostic for any LP or GP trying to benchmark a process against what institutional investors are now treating as table stakes. It also implicitly signals where the market’s next governance fight is heading: the report flags early discussion of “CV squared” structures, assets rolled repeatedly across successive continuation vehicles without a clear ultimate exit — as a point where LP sensitivity is likely to increase. Worth watching as 2020–21 vintages hit extension windows over the next 12–18 months.

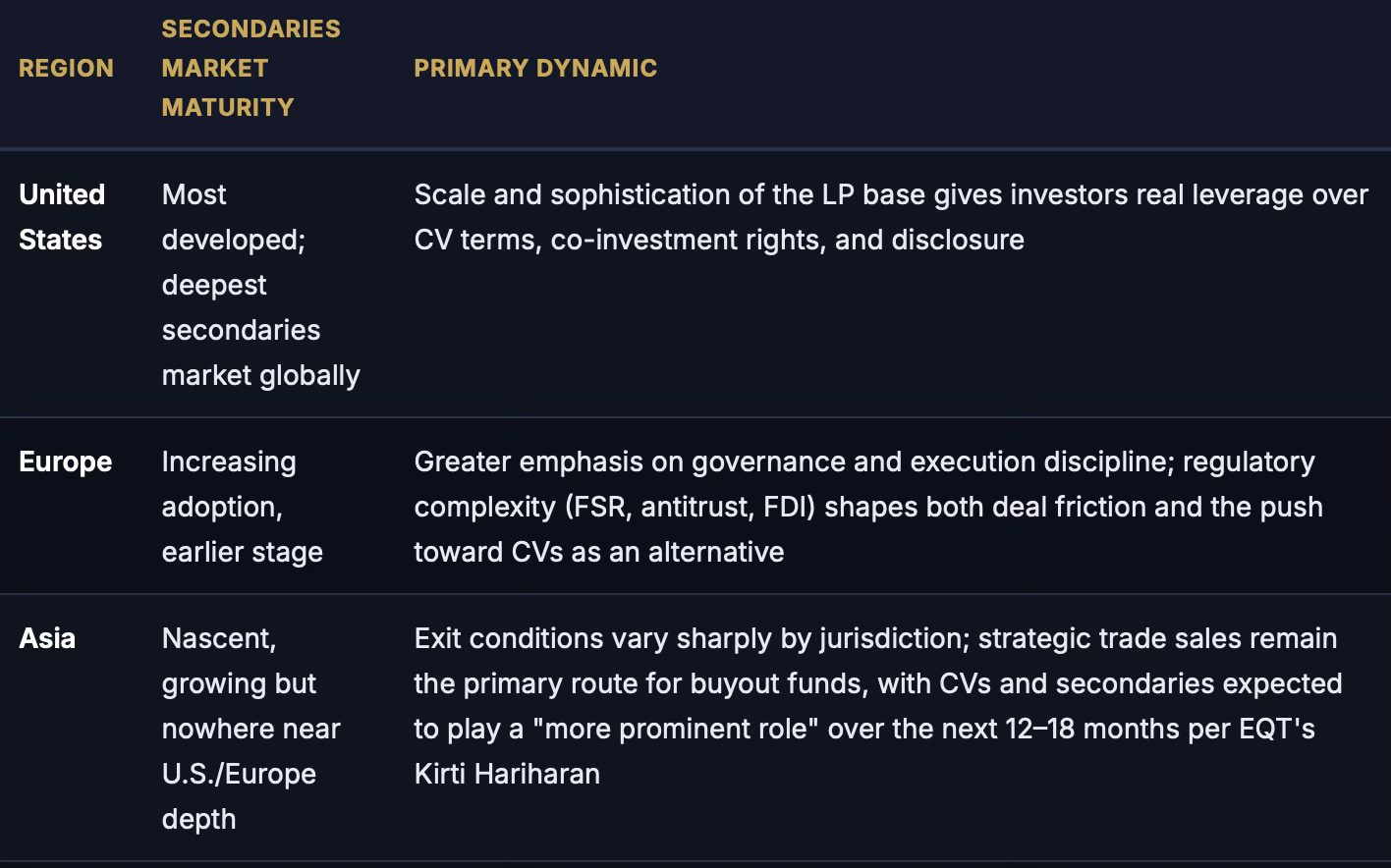

Regional Divergence: Where Secondaries Sit in Each Market’s Maturity Curve

That regional split is a useful corrective to any narrative that treats “secondaries going mainstream” as a single global phenomenon happening at the same pace everywhere. It isn’t. The U.S. market’s depth is precisely what’s generating the governance and litigation pressure described above, a more mature market produces more sophisticated LPs, which produces more scrutiny, which produces more process discipline. Europe is following the same trajectory a step behind. Asia is a different market altogether, where IPO windows and strategic trade sales still dominate and secondaries remain a supplementary tool rather than a default one.

The AI Wrinkle: A New Source of Assets Entering the Secondaries Pipeline

One connection the report doesn’t draw out explicitly, but that falls out naturally from reading the AI and exit sections together: AI-driven valuation uncertainty, particularly the repricing hitting SaaS and software assets exposed to obsolescence risk, is creating exactly the kind of asset that ends up in a continuation vehicle. A GP holding a software platform it still believes in, but that the public market or a strategic buyer is currently mispricing on AI-disruption fears, has a strong incentive to hold rather than sell into that mispricing. Expect this to show up as a growing category of CV rationale over the next few quarters, distinct from the more familiar “we still like this asset and don’t want to force an exit” logic.

About Ropes & Gray

Ropes & Gray is a global law firm with more than 1,500 lawyers and legal professionals across offices in New York, Boston, Chicago, Los Angeles, San Francisco, Silicon Valley, Washington, D.C., London, Dublin, Milan, Paris, Hong Kong, Seoul, Singapore, and Tokyo. The firm has been ranked in the top three of The American Lawyer’s “A-List” for nine consecutive years. Its practice areas include asset management, private equity, M&A, finance, real estate, tax, antitrust, life sciences, healthcare, intellectual property, litigation and enforcement, privacy and cybersecurity, and business restructuring.

Secondary Scoop | Analysis based on Ropes & Gray, Cautious Optimism: How Private Equity Is Navigating a New Era of Uncertainty (July 2026). Data points independently sourced to McKinsey’s Global Private Markets Report 2026, KPMG’s Pulse of Private Equity Q4 2025, and Secondaries Investor.