Asante Capital Group, Jasmin Capital and William Blair’s Private Capital Advisory team all published their Q2 2026 outlooks within weeks of each other, each with its own framing: Asante on the rise of multi-track fundraising, Jasmin on continuation funds specifically, William Blair on the state of LP- and GP-led pricing through the first half. None of the three set out to write the same article. Read side by side, though, their data lines up into a clearer picture of where the secondaries market actually stands at the midyear mark than any one report offers alone. Here are the six trends that picture leaves behind.

TREND 01

The records keep converging, not just compounding

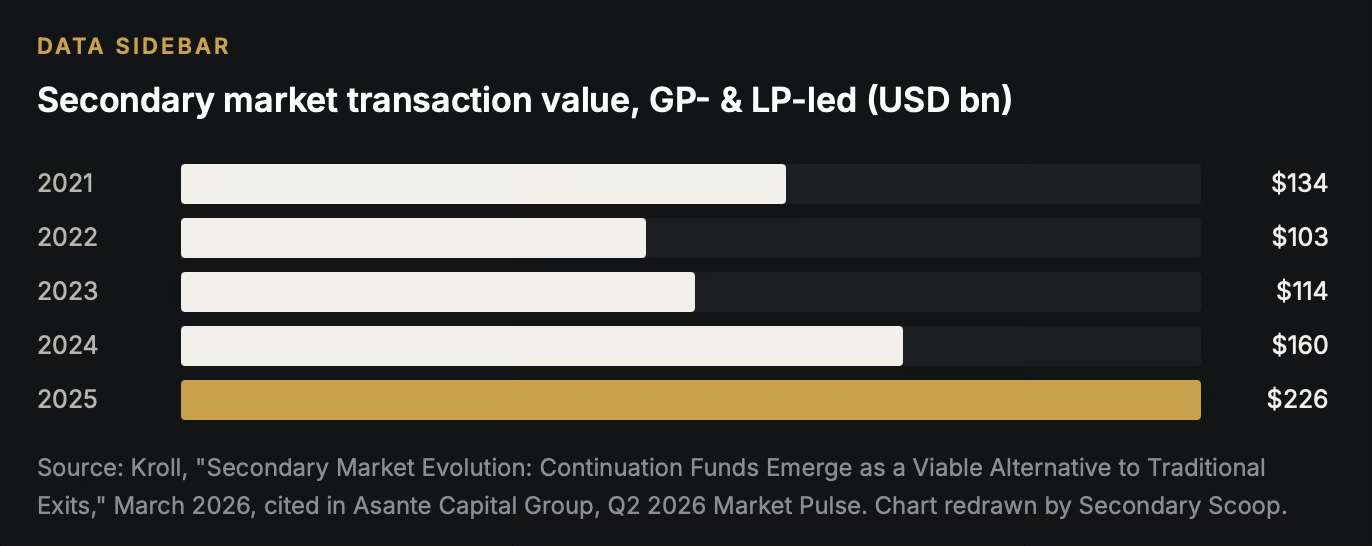

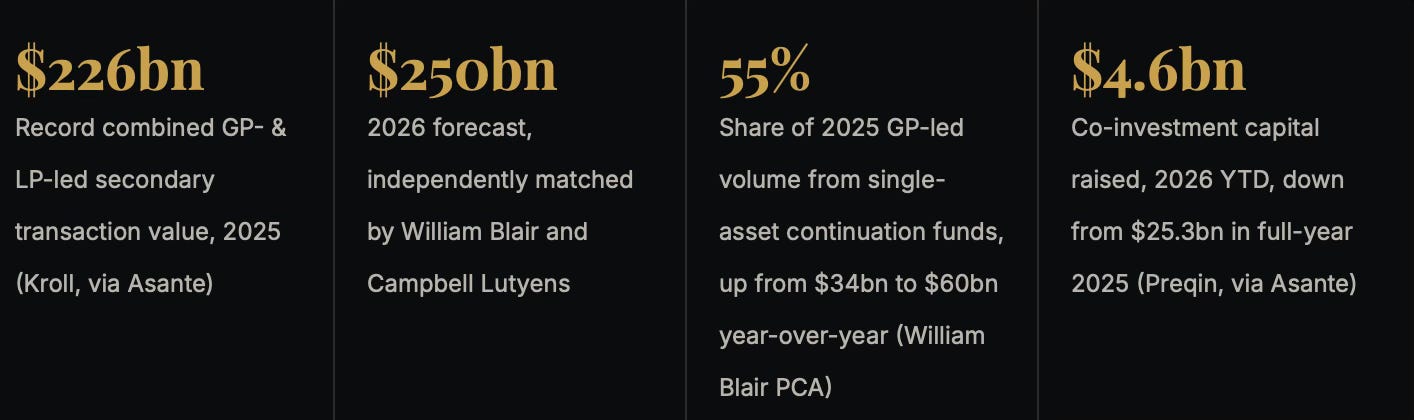

All three reports independently land in the same range for 2025, and it is worth pausing on how rare that kind of agreement is. Asante, citing Kroll, puts combined GP- and LP-led secondary transaction value at $226bn for 2025, an all-time high and a 69% increase since 2021. William Blair’s own tally puts 2025 at $220bn. Jasmin and Flexstone Partners’ David Arcauz cite GP-led volume alone as having “surpassed $100bn.” For 2026, the forecasts converge again: William Blair projects $250bn, matching Campbell Lutyens’ separate projection reported earlier this year.

What is notable is not the growth curve itself, which has been reported all year, but that three firms with different books of business, a placement agent, a European boutique, and an investment bank’s advisory arm, are no longer describing different markets. The estimates have converged. That is a signal the market has moved from “hard to size” to “sized, and still growing.”

TREND 02

The GP-led story is really a single-asset story

Inside that GP-led growth, William Blair’s data shows where the capital is actually concentrating: single-asset continuation funds (SACFs), vehicles built around one portfolio company rather than a diversified basket. SACF volume grew from $34bn in 2024 to $60bn in 2025 and now accounts for 55% of GP-led category volume, a share the firm says kept rising through the first half of 2026 even as multi-asset continuation fund (MACF) activity declined. William Blair points to its own $850m single-asset continuation fund for Ares Management’s Convergint Technologies, closed in February 2026, as an example, part of what it describes as more than $10bn of GP-led volume the firm closed or signed in the preceding two quarters.

That concentration pattern lines up with Jasmin’s own framing of the driver behind the CV boom: GPs using continuation vehicles “for the first time to retain some of their trophy assets.” SACFs are, structurally, the vehicle built for exactly that use case, and the data suggests it is where sponsors are increasingly putting their effort, not diversified multi-asset vehicles.

TREND 03

Liquidity is the only conversation, but not every channel is benefiting from it

Across all three reports, liquidity has displaced returns as the central topic. Asante states plainly that DPI has overtaken IRR and TVPI as the metric LPs scrutinize in re-up discussions, a point Reverence Capital’s Milton Berlinski independently corroborates in his Jasmin interview, noting that five-year DPI across the industry has run below historical norms. Fundraising timelines have stretched accordingly: Asante’s data, citing Buyouts’ Fundraiser Report, shows the average span from first to final close reaching 30 to 32 months in 2024 to 2025, up from roughly 14 months in 2000.

Liquidity innovation, particularly in secondaries and GP-led transactions, is becoming more institutionalized.

Milton Berlinski, Co-Founder and Managing Partner, Reverence Capital Partners; interview, Jasmin Capital Newsletter N°13/2026

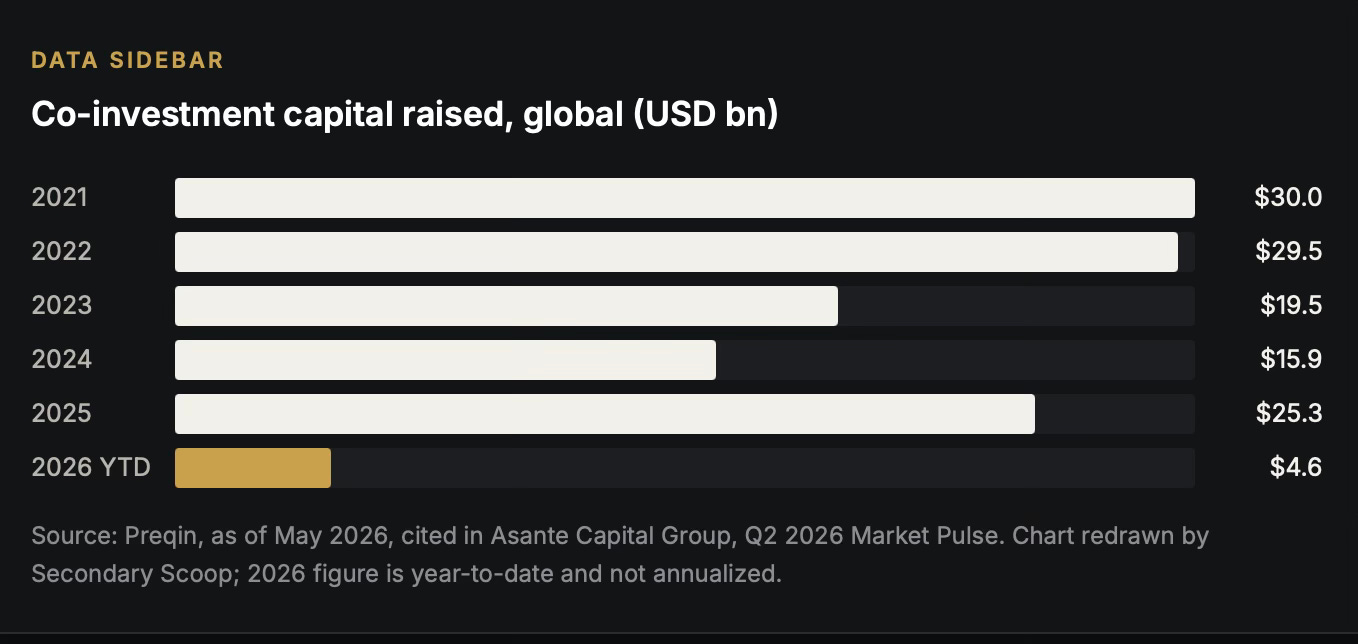

But the liquidity story is not evenly distributed across the tools built to deliver it. Asante’s own co-investment chart shows capital raised falling to $4.6bn year to date in 2026, against $25.3bn for full-year 2025 and a 2021 peak of $30bn. Annualized, that is a fraction of last year’s pace, even as secondaries and continuation funds keep setting records. If liquidity is the theme of H1 2026, secondaries specifically, not the broader “access” toolkit, is where the capital is actually landing.

TREND 04

Structural innovation is outrunning LP governance

Jasmin’s newsletter documents a genuine structural advance this year: the co-control continuation vehicle.

EXPLAINER: CO-CONTROL CVS

A co-control continuation vehicle sells 50% of a portfolio company to a new sponsor through a competitive M&A process, then transfers the remaining 50% into a CV managed by the incumbent GP, at the same valuation established by that process. It is pitched as a “third way” between a majority CV and a full trade sale: the GP secures a market-tested price for existing LPs and keeps an active stake, and the asset gains a second sponsor’s complementary expertise, at the cost of co-governance complexity between two firms now sharing control of one company.

Even as that kind of innovation spreads, Jasmin concedes that LP governance has not kept pace. “One of LPs’ most common criticisms of CVs is the lack of a genuine choice: either they take the cash option, or the roll-over option,” the firm writes, with no status-quo option to simply leave the asset in the original fund. The roll-over option itself is only realistic for LPs “equipped and accustomed to deciding on direct investment opportunities within a few weeks,” typically funds-of-funds, leaving institutions whose mandate is manager selection, rather than direct underwriting, with cash as their only practical outcome. Jasmin’s own forecast, drawn from its proprietary Secondaries Index, expects GPs to run 1 to 2 CVs per fund by 2030, which only sharpens the question of whether LP-side process has caught up with GP-side adoption.

TREND 05

Secondaries is expanding well beyond buyout

Flexstone’s Arcauz, interviewed in the Jasmin newsletter, describes GP-led transactions “expanding beyond buyout into infrastructure, credit and venture strategies,” alongside continued scaling of NAV financing and GP liquidity solutions. William Blair’s newsletter independently confirms the pattern from the LP-led and platform side, noting the emergence of sector-focused specialists, including venture LP secondaries, infrastructure-specific fundraises and secondary real estate practices, alongside large platforms building out credit-focused secondaries capabilities. Both firms frame this the same way: a signal that limited partners and secondary buyers are growing more comfortable moving outside the traditional buyout strategy that has anchored the market historically.

TREND 06

The firms selling this narrative are consolidating around it

The clearest cross-report theme is one none of the three highlights as their lead story: the advisory and placement-agent layer sitting on top of the secondaries market is itself consolidating. Asante notes that capital is concentrating toward the top of the market, with mega-funds and established franchises capturing a disproportionate share of commitments. Flexstone’s Arcauz states outright, in the Jasmin interview, that “consolidation across asset managers is accelerating as firms seek to broaden capabilities and increase AUM.” William Blair goes furthest, naming platform consolidation as an explicit 2026 theme in its own right, with insiders expecting the trend to continue over the next couple of years and “increasing pressure to grow faster.”

That is not an abstract observation this quarter. It is the same window in which Lazard agreed to acquire secondaries placement agent Campbell Lutyens for roughly $575m to form “Lazard CL,” and Houlihan Lokey agreed to acquire energy-focused boutique Intrepid Financial Partners. Three placement agents and advisory teams independently naming consolidation as a defining feature of the market are writing from inside a peer set that is, in real time, consolidating.

Heading into H2

None of this reads as a market losing momentum. If anything, the opposite: a market absorbing this much capital, this consistently, across GP-led and LP-led structures alike, is functioning as the private markets’ primary portfolio-management tool, not a peripheral or opportunistic one. What the first half actually shows is where that growth is concentrating: into secondaries specifically, then further into single-asset continuation funds, expanding into new asset classes, built on structures LP governance has not fully caught up with, and sold by an advisory market that is consolidating around fewer, bigger players even as it describes the trend to clients. Whatever H2 brings on the AI and tariff fronts both reports flag as live risks, those are the six threads worth tracking against.

SOURCES

Asante Capital Group, Q2 2026 Market Pulse: It’s More Than Just Primary Fundraising These Days, June 2026.

Jasmin Capital, Newsletter N°13/2026: Continuation Funds, Market Trends and Outlook, including interviews with David Arcauz (Flexstone Partners) and Milton Berlinski (Reverence Capital Partners), June 2026.

William Blair Private Capital Advisory, Continued Bullishness Across Secondaries Despite More Macroeconomic Changes, Q2 2026 Quarterly Newsletter, June 2026.

Kroll, “Secondary Market Evolution: Continuation Funds Emerge as a Viable Alternative to Traditional Exits,” March 2026.

Preqin, co-investment and global deployment data, as of May to June 2026.