The $13 Trillion Case Blackstone Didn't Mean to Make

Blackstone's 2026 mid-year CIO letter is macro, not secondaries, yet it's one of the cleanest third-party validations of the "secondaries as portfolio management" thesis this cycle.

Blackstone’s Office of the CIO publishes twice a year, and the mid-year edition is built to be a firm-wide statement: AI, growth, labor, inflation, capital markets, five factors shaping the whole portfolio. Secondaries get one page out of twenty-five. That’s the point. When a document with no reason to talk its own book on secondaries still lands on a $13 trillion exposure number and a sub-2% turnover rate, it’s worth reading closely, and worth checking against what Blackstone’s own secondaries platform has actually been doing with that opportunity.

The number that matters isn’t the growth rate

The headline stat is familiar to anyone who follows this market: annual secondary volume has gone from roughly $23 billion in 2010 to an estimated $250 billion in 2025, a tenfold increase in fifteen years. That’s the number every secondaries deck opens with, ours included.

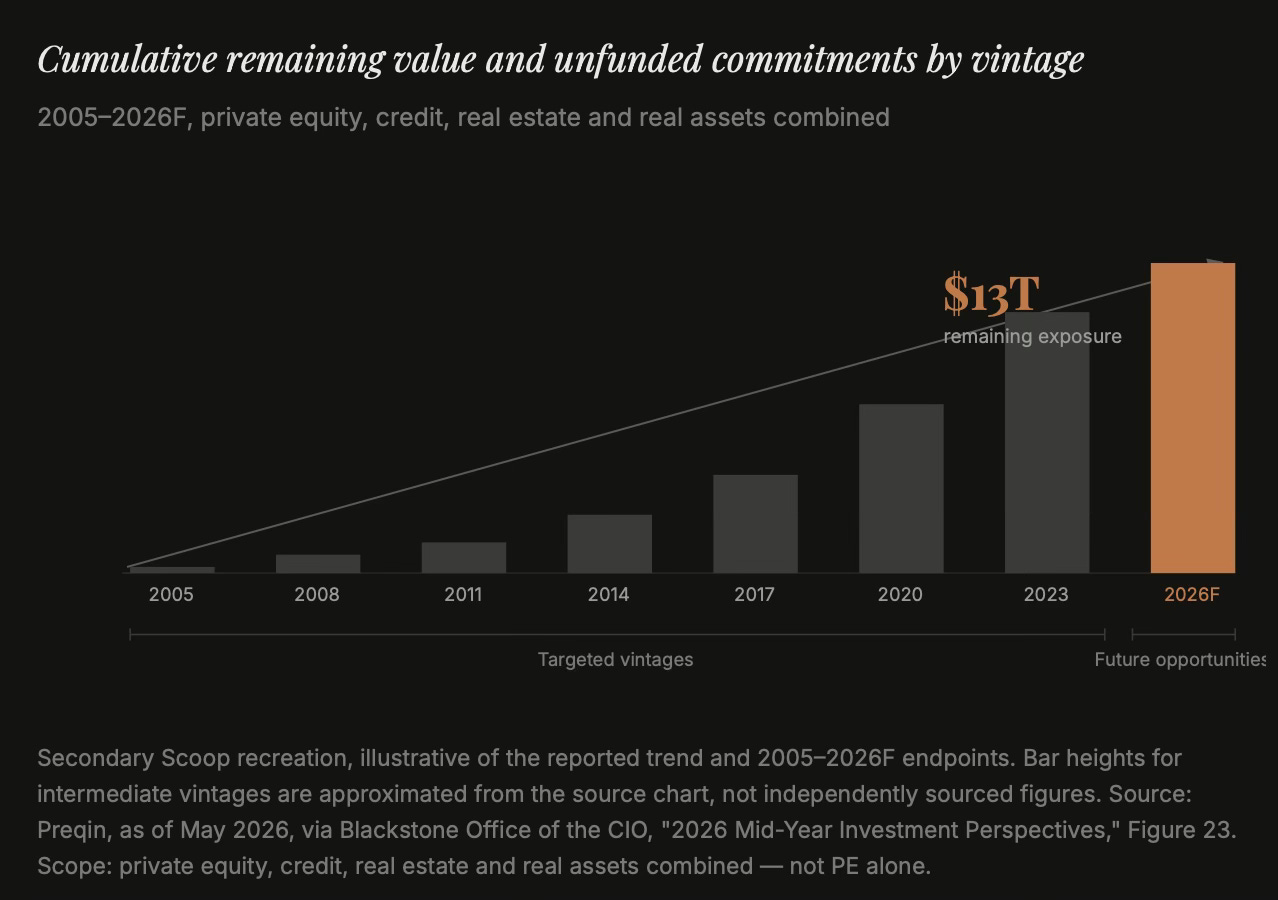

The more interesting number sits two sentences later. Blackstone’s own citation puts annual secondary turnover at less than 2% of total private markets AUM. Pair that with the report’s separate data point: $13 trillion in cumulative remaining value and unfunded commitments sitting across private market vintages back to 2005, and you get the actual argument, which isn’t about growth rate at all. It’s about denominator.

One correction worth flagging on that $13 trillion figure: it isn’t purely a private equity number. Blackstone’s own footnote defines it as remaining value and unfunded commitments across “private equity, credit, real estate and real assets”, the full private markets complex, not PE alone. That doesn’t weaken the argument. If anything, a $13 trillion pool spanning multiple asset classes is a larger and more durable overhang than a PE-only figure would suggest, and it matches the direction Blackstone’s own secondaries platform has been expanding in.

A market moving $250 billion a year against a $13 trillion pool of remaining exposure isn’t a mature market clearing its backlog. It’s a market that has barely started. That’s the case Coller and Carlyle AlpInvest have both been making in their own barometers this cycle, the difference here is that Blackstone arrives at the same conclusion from the LP-commitment side of the ledger rather than the deal-volume side.

A market moving $250 billion a year against $13 trillion in remaining exposure isn’t clearing a backlog. It’s barely started.

Why the LP base itself is the story

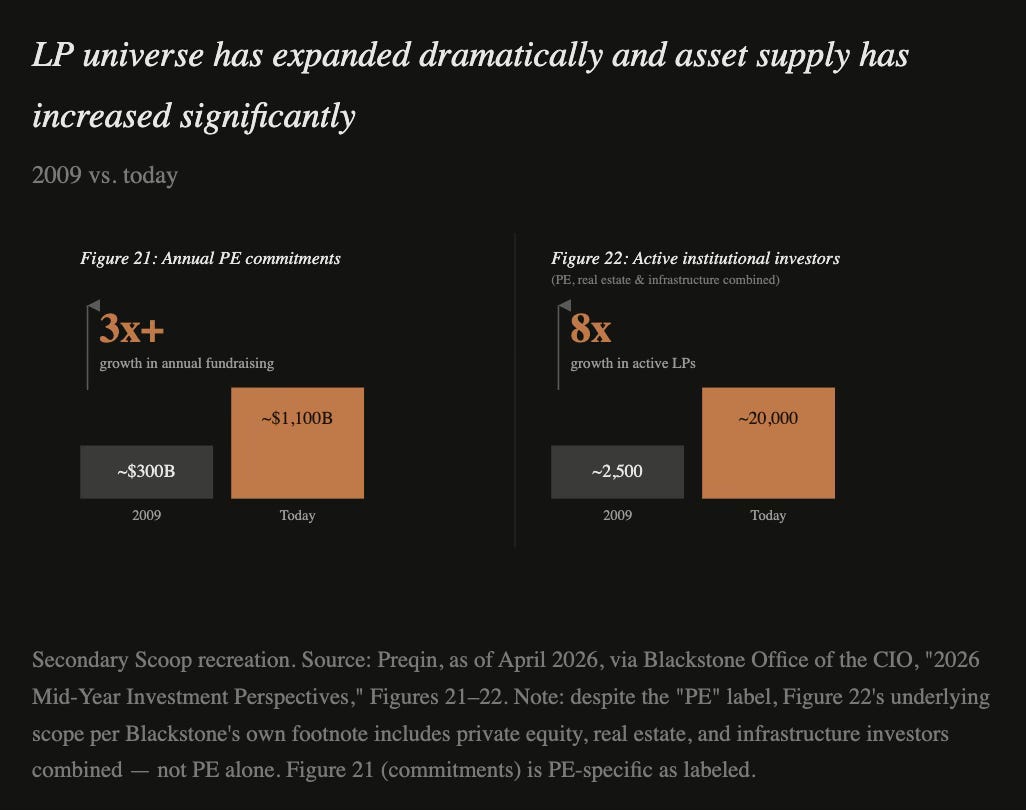

Blackstone frames this growth as a function of the buyer base, not just the asset pool. The number of active institutional investors across private equity, real estate and infrastructure has grown roughly eightfold since 2009, from about 2,500 to an estimated 20,000 today, while annual commitments across those same strategies have more than tripled to roughly $1.1 trillion. Every one of those LPs is a future secondary seller, buyer, or both, an expanding universe that didn’t exist when secondaries were still read as a distress signal rather than a liquidity tool.

That expansion is precisely why Blackstone’s own note on market structure lands the way it does: sourcing across “a fragmented global ecosystem” now requires GP relationships spanning strategies, vintages, and geographies, plus underwriting conviction across LP-led, GP-led, and GP-stakes transactions simultaneously. Scale isn’t a nice-to-have in that description, it’s positioned as the entire moat. As the final section below shows, that description happens to match Blackstone’s own secondaries business almost exactly.

The adjacent data that reinforces the thesis

Two other threads in the report matter for anyone tracking the CV and exit landscape, even though neither is filed under “secondaries.”

EXIT MARKETS ARE REOPENING — BUT THAT CUTS BOTH WAYS

Blackstone forecasts roughly $160 billion in US IPO proceeds in 2026, about 4x 2025’s total, across an estimated 100 listings, about 2x last year’s count: two different multiples worth keeping separate, since the average deal size implied by that math is meaningfully larger than in 2025. Alongside that, corporate PE fund realizations exceeded $25 billion across 2025 and Q1 2026. A genuine exit recovery is good news for realized DPI and could, in theory, reduce the urgency behind LP-led selling. But it doesn’t touch the underlying overhang: assets that were never going to IPO in the first place, or GPs who want to keep compounding a winner past a fund’s natural life. That’s the CV case, and nothing in the IPO recovery narrative displaces it.

LONGER HOLD PERIODS ARE BEING BUILT INTO THE SYSTEM, NOT JUST OBSERVED IN IT

The AI infrastructure buildout that dominates the rest of the report, $100 billion in Blackstone’s own data center commitments by year-end 2026, a global data center platform Blackstone now values at $165 billion, plus a further ~$160 billion development pipeline, is capital-intensive, long-duration, and structurally incompatible with a standard 3-5-7 year fund life. If hard-asset and infrastructure-adjacent strategies keep pulling private capital toward longer holding periods, continuation vehicles stop being a workaround and start being the native structure for that kind of asset. Blackstone doesn’t make this connection explicitly. The data does it for them.

Inside Strategic Partners: what the growth actually looks like

The CIO letter’s one page on secondaries is written in the abstract — market size, LP count, structural argument. What it doesn’t do is describe Blackstone’s own position in that market, which is worth doing separately, because the numbers are large enough to be the story in their own right.

Blackstone’s secondaries platform, Strategic Partners, started outside the firm entirely. It was founded in 2000 as an independent secondary private equity shop, and by the time Blackstone came calling it had raised just over $11 billion of capital commitments and completed more than 700 transactions. Blackstone acquired it from Credit Suisse in August 2013, when it managed about $9 billion. Verdun Perry, who joined Strategic Partners at its founding in 2000, has run the business — and chaired the investment committee for every fund it has raised — for the entire 26 years since, through both ownership changes.

2000: Strategic Partners founded as an independent secondaries manager. Raises over $11bn and completes 700+ transactions before being acquired.

2013: Blackstone acquires Strategic Partners from Credit Suisse. AUM at acquisition: ~$9bn.

2022: AUM reaches $67bn (as of Sept 30), across private equity, real estate, infrastructure and GP-led strategies.

2023: Closes Strategic Partners IX at $22.2bn — the world’s largest dedicated secondaries fund raised to that date — alongside its inaugural dedicated GP-led continuation fund strategy, Strategic Partners GP Solutions, at $2.7bn.

2025: SP IX is nearly fully committed ($19.7bn of $22.2bn by year-end). Strategic Partners Infrastructure IV closes at $5.5bn in September — the largest dedicated infrastructure secondaries fund ever raised. Platform AUM reaches ~$91bn.

2026: Strategic Partners crosses $100bn in AUM in Q1, per Jon Gray on the April 23 earnings call. Its flagship successor fund, Strategic Partners Fund X, holds an initial close of $5bn, then adds $6bn more in the same quarter — $11bn raised so far toward a still-undisclosed target.

The platform now spans four distinct secondary strategies — private equity, GP-led/continuation vehicles, infrastructure, and real estate — with more than 2,350 transactions completed since 2000. A fifth is reportedly being built: trade press has reported that Blackstone is developing a dedicated private credit secondaries strategy to sit inside Strategic Partners, though the firm hasn’t confirmed this publicly. If it materializes, it would put Blackstone in the same race as Ares, which closed a $7.1bn dedicated credit secondaries fund in January, and would track an industry-wide shift — 2025 was the first year fund manager-led (GP-led) secondary volume overtook allocator-led (LP-led) volume industry-wide, with more than $7bn of dedicated credit continuation vehicles closing across the market that year.

Put the CIO letter’s abstract argument next to this timeline and the connection is hard to miss. “Deep GP relationships,” “a broad view across strategies, vintages, and geographies,” underwriting “quickly and with conviction across LP-led, GP-led, and GP stakes transactions” — that isn’t a general description of what wins in a fragmented market. It’s a fairly literal description of what Strategic Partners has spent four fund families and 13 years under Blackstone’s ownership building. The CIO letter frames scale as the moat. Strategic Partners is the moat.

The takeaway

None of the market-level data is new information. What’s notable is where it’s coming from, and what it lines up with once you look past the one page it’s written on. A firm-wide CIO letter, written for LPs, allocators, and internal audiences well beyond the secondaries desk, independently arrives at the same structural argument this publication has been making all year: the overhang is enormous, the clearing mechanism is still tiny relative to it, and the buyer and seller base underpinning both sides of that trade keeps getting deeper. That’s not a market waiting for a catalyst. It’s a market whose catalyst already happened — and the firm that wrote this letter has spent over a decade and four flagship fund families positioning itself to be the one clearing it.

Secondary Scoop · Source: Blackstone Office of the CIO, “2026 Mid-Year Investment Perspectives,” June 2026. Data and charts redrawn by Secondary Scoop; original figures and endnote sourcing available in the source document.