The Alpha Factory: How GP-Led Secondaries Pocket Returns That Never Appear in the Model

The industry has settled on a neat framework: GP-leds are private markets alpha, LP-leds are private markets beta. The framework is useful. What it understates is where the alpha actually comes from.

Analysis based on Ares Management: "Why Now for GP-Led Secondaries"

The secondaries market has, over the past decade, developed a working vocabulary for itself. LP-led transactions, fund stake sales driven by limited partners seeking liquidity, are described as diversified, discount-driven, and reliable. GP-led transactions, continuation vehicles through which general partners transfer assets into new structures, are positioned as concentrated, compounding, and return-driven. The shorthand that has taken hold: LP-leds are private markets beta. GP-leds are private markets alpha. It is a framework Ares Management lays out explicitly in a recent perspective piece on the GP-led market.

But the framework papers over a structural mechanic in GP-led deals that the alpha/beta analogy doesn’t fully capture, and that may be one of the more underappreciated sources of return in the asset class.

The Framework, and Why It Holds

The alpha/beta distinction maps reasonably well onto how the two deal types actually work. In LP-led secondaries, a buyer acquires a diversified portfolio of fund stakes, often dozens to hundreds of underlying companies, at a discount to net asset value. Returns are driven primarily by that entry discount, the passage of time, and the realization of assets already in the ground. The buyer is not selecting individual companies; they are acquiring exposure to a broadly constructed portfolio and capturing the gap between purchase price and fair value.

GP-led continuation vehicles work differently. A general partner selects one or multiple assets, typically those it views as having substantial remaining upside, and transfers them into a new vehicle, giving existing LPs the choice to roll their position or take cash. New secondary buyers enter at a price set to the current NAV. There is no diversification by design. The return is driven by the long-term compounding of the underlying asset, not the entry discount. The buyer is making a concentrated, underwritten bet on a specific business.

LP-leds give you exposure to what private equity has already built. GP-leds give you exposure to what a GP still believes it can build. One is a claim on the past. The other is a wager on the future.

The distinction matters for portfolio construction. An LP allocating to both segments is not doubling down on secondaries, they are accessing two structurally different return profiles that happen to sit within the same asset class label. Combined, they offer multiple drivers of return that can be weighted depending on where the market environment favors entry discounts versus compounding.

The Mechanic the Model Misses

Within the GP-led segment, there is a specific structural feature that distinguishes continuation vehicles from both LP-led secondaries and direct private equity investments, and that is only recently beginning to receive consistent attention from buyers.

In a conventional M&A transaction, there is a gap between the date a deal is signed and the date it closes. During that period, which can run from weeks to several months, the target company continues to operate. Revenue is generated, EBITDA accumulates, contracts are signed. The company keeps creating value. In a standard M&A deal, the seller retains the economic benefit of that interim value creation: the purchase price is fixed at closing, and the seller captures whatever happens between signing and close.

Continuation vehicles are structured differently. In a GP-led deal, the purchase price is set to the net asset value at signing, not at closing. Any value created between signing and closing, operating performance, multiple expansion, debt paydown, accrues to the buyer. It is a built-in return enhancement that does not appear in the initial underwriting model, because it cannot be predicted with precision at the time of signing.

HOW THE MECHANIC WORKS

In M&A: Purchase price locked at closing → seller keeps interim value creation → buyer starts from zero on day one.

In a GP-led CV: Purchase price locked at signing → buyer captures all value created between signing and close → return is higher than the model projected at the time of underwriting.

The gap between signing and closing is not a rounding error. For complex transactions involving multiple limited partners, regulatory approvals, or cross-border structures, it can extend to six months or longer — a meaningful window in a business generating EBITDA growth.

This is not a theoretical benefit. It is a systematic structural advantage that accrues in every GP-led deal where the underlying business performs during the closing period. The buyer does not need to underwrite it — it arrives automatically. The only scenario in which it cuts the other way is if the business deteriorates between signing and closing, in which case the loss also accrues to the buyer. The mechanic is bilateral, but in a portfolio of assets selected for their growth trajectory, the asymmetry historically favors the buyer.

Adoption Has Made This a Structural Feature, Not a Cycle

The practical significance of both the alpha framing and the signing-to-closing mechanic depends on whether GP-led secondaries remain a meaningful part of the private equity exit landscape. The data suggests they have become one.

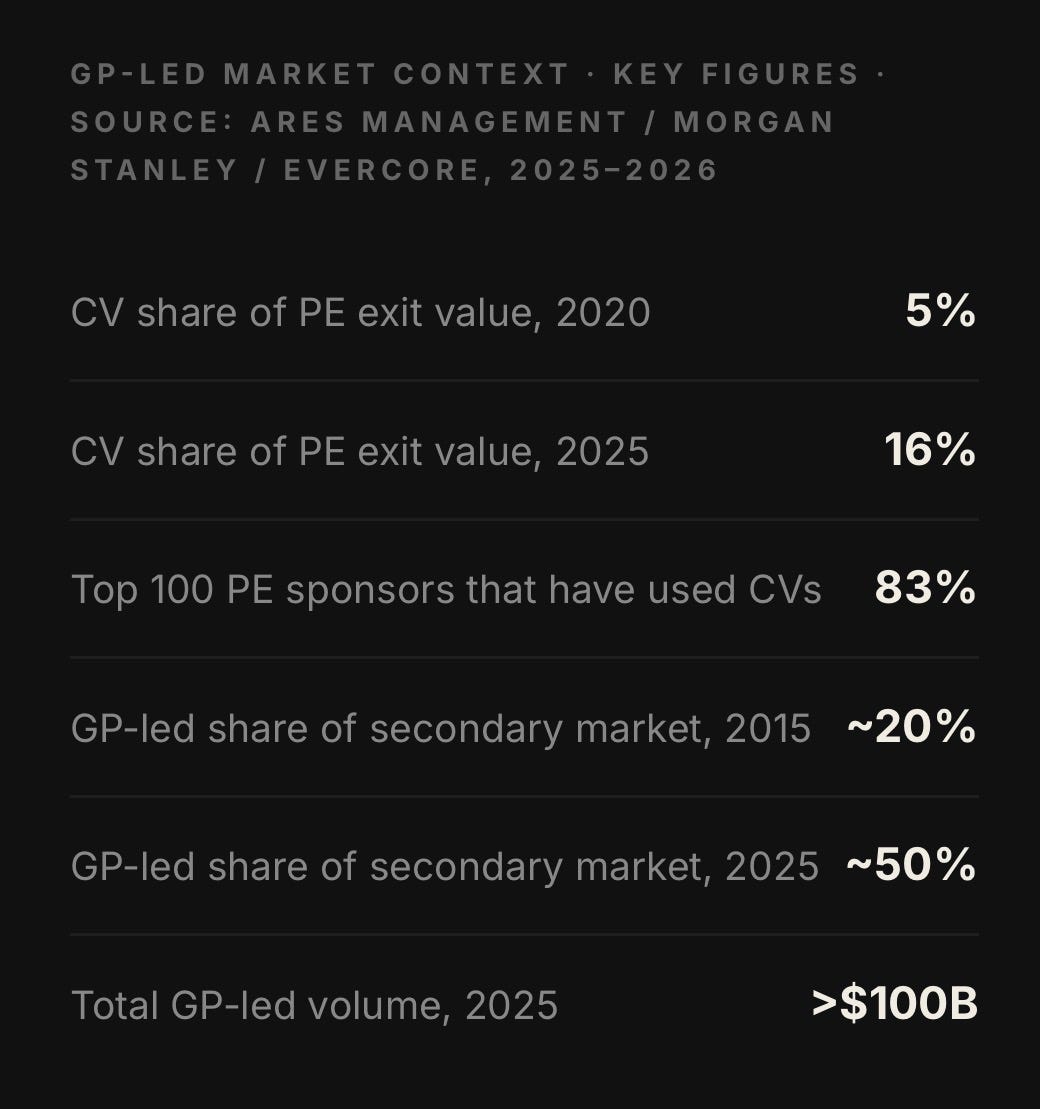

These numbers tell a story about normalized adoption rather than cyclical demand. Continuation vehicles initially expanded in 2022–2023, when traditional exit routes (IPOs, M&A) contracted sharply and GPs needed alternatives to generate LP liquidity. The intuitive expectation was that CV volume would recede once conventional exits recovered. It has not. Even as global M&A activity surpassed $5 trillion in 2025, GP-led secondaries continued to grow. When 83% of the top 100 global buyout sponsors have accessed the CV market at least once, it is no longer reasonable to describe the instrument as niche or opportunistic.

The exit market share figure is particularly significant. CVs now account for 16% of total private equity exit value, up from 5% just five years ago. That is not a rounding error in the PE exit landscape. It is a structural shift in how large private equity firms manage the tail of their portfolios and deliver liquidity to LPs without sacrificing positions they believe have room to run.

What the Alpha Label Gets Wrong

The alpha/beta framework is analytically useful but carries a risk of oversimplification. Alpha, in the conventional sense, implies skill-driven outperformance against a benchmark. Applied to GP-led secondaries, it suggests that buyers of CVs are generating returns through superior asset selection. That is partially true, underwriting a single-asset continuation vehicle requires genuine bottom-up diligence on a specific business, its management team, competitive dynamics, and exit path.

But the signing-to-closing mechanic is not alpha in that sense. It is a structural feature of how the transaction is priced. It does not require skill to access, it accrues automatically to any buyer who closes a GP-led deal. It is, in effect, a systematic return enhancement embedded in the structure of every continuation vehicle, invisible at the time of underwriting and unattributable to any particular analytical insight.

The implication is that part of what the market labels as "GP-led alpha" is better understood as structural return-return that derives from transaction architecture rather than from picking the right asset. That distinction matters for how buyers should think about the asset class: the floor of expected return in a well-selected GP-led portfolio is higher than the model suggests, not because the underwriter was conservative, but because the structure delivers value the model cannot fully price.

Part of what gets labeled GP-led alpha is structural, not analytical. The deal architecture delivers returns that the underwriting model never counted.

Some Extra Thoughts

The alpha/beta framework gives secondaries investors a useful shorthand for portfolio construction. It captures something real: LP-leds and GP-leds are not the same instrument, and treating them as interchangeable because both sit inside "secondaries" misses the different risk/return profiles on offer.

But the framework is incomplete as a description of where GP-led returns actually originate. The signing-to-closing mechanic is a structural return source that sits below the analytical layer, it does not depend on picking the right asset, only on being a buyer in a correctly structured GP-led transaction. Combined with the normalized adoption of CVs as a mainstream PE exit tool (16% of PE exit value, 83% of top-100 sponsors), the structural dimension of GP-led returns is likely to compound over time as deal volumes grow and the mechanic repeats across a larger pool of transactions.

The better mental model is this: GP-led secondaries offer two return streams: one analytical (asset selection, growth underwriting, exit timing) and one structural (the signing-to-closing enhancement). The alpha label captures the first. It misses the second entirely.

Sources. Market data and the signing-to-closing mechanic described in this article draw on Ares Management's June 2026 perspective "Why Now for GP-Led Secondaries." GP-led market share and volume figures cited from Evercore Private Capital Advisory 2025 Secondary Market Highlights (January 2026). CV share of PE exit value from Morgan Stanley FY 2025 Investor Survey and LSEG sponsor-backed exit data (May 2026). Top-100 sponsor adoption figure references Private Equity International rankings, as cited by Ares Management. Return projections and loss ratio comparisons are Ares Management's own figures and carry standard forward-looking statement disclaimers; they are cited as market color, not as independently verified benchmarks. All analysis and editorial framing are Secondary Scoop's own.