The CV Reckoning

ILPA's 2026 continuation vehicle guidance arrives at the exact moment the industry needs it most, and its standards are the strictest yet.

The numbers tell a clear story. The global secondary market hit a record $240 billion in 2025, a 48% jump from 2024. GP-led transactions claimed 48% of that total, with continuation vehicles representing between 86% and 89% of all GP-led activity. Single-asset CVs alone accounted for 53% of GP-led volume. Twenty-nine transactions exceeded $1 billion, up from 21 the year before. Eighty-three percent of the top 100 global buyout sponsors have now completed at least one CV.

This is not a niche product anymore. CVs have become a structural feature of how private equity manages portfolios and delivers, or defers, liquidity. And yet, the market’s rapid expansion has outpaced the governance frameworks designed to protect the LPs who must decide, repeatedly and under time pressure, whether to sell or roll.

ILPA’s newly released 2026 Continuation Vehicle Guidance (open to comments until August 5th) is the industry’s most serious attempt yet to close that gap. It is also, notably, a document whose timing is not accidental.

Why the Market Got Here

The structural driver is not complicated: too much capital, held too long, generating too little cash. The stock of unrealized assets across global private equity portfolios has reached approximately $3.8 trillion, roughly 32,000 companies. Holding periods at exit are now hovering around seven years, up from five to six years in the prior cycle. For the critical 2018–2021 fund vintages, which should currently be in their peak harvest period, DPI levels are reportedly as low as 0.1x to 0.3x.

“DPI has overtaken IRR as the metric that drives LP re-up decisions. Managers who can’t show progress toward at least 1.5x paid-in capital by year eight face a difficult fundraising conversation, regardless of the unrealized value generated.”

Against that backdrop, the cumulative LP cash flow deficit has reached $260 billion since 2022, according to Carlyle AlpInvest’s analysis. Distributions have recovered somewhat from their 2023 lows but remain roughly half the levels investors became accustomed to in prior cycles. The practical consequence: LPs are capital-constrained precisely as they face a wave of GP fundraising asks and, increasingly, CV sell-or-roll decisions.

GPs, meanwhile, have found CVs to be a genuinely useful tool in this environment. They allow high-conviction assets to be held longer without forcing a distressed sale. They offer LP optionality, cash out or roll, rather than a binary fund liquidation. And, critically, they allow carry to crystallize and be redeployed into succession planning. According to Bain’s 2026 Midyear PE Report, GP-led CVs grew 62% year-over-year, and 37% annually since 2022. Roughly 25% of GPs have recently launched or completed a CV; about 40% expect to explore one in the next one to two years.

The problem is that growth at this speed and scale, in a product that is, by definition, a related-party transaction, has created documented friction between GPs and their LPs.

LP Sentiment: Structural, Not Cyclical

The Coller Capital Summer 2026 Barometer, the 44th edition of the survey, published June 24, provides the clearest read on where LPs actually stand. The findings are striking, and not in the way CV optimists would hope.

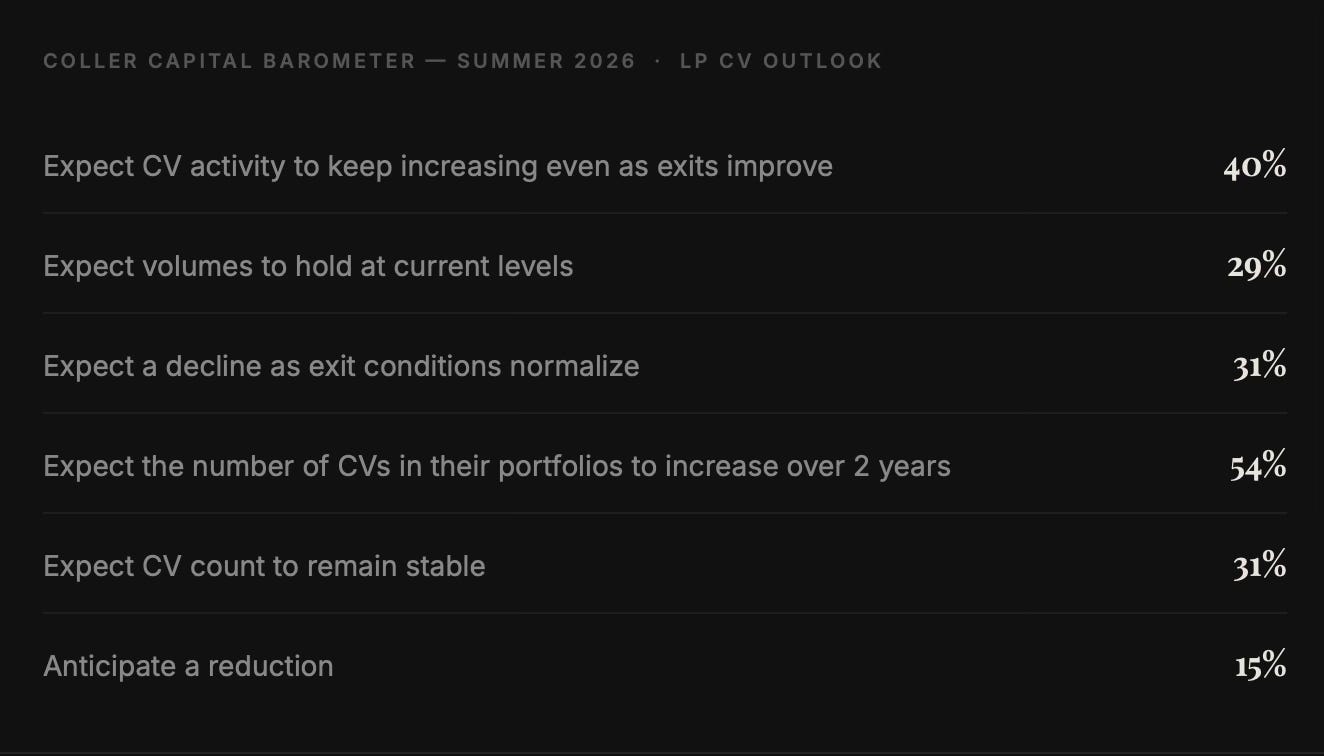

The data point that matters most: 69% of LPs expect CV activity to either increase or hold at current levels, even as traditional exits recover. This is not a temporary workaround. It is a permanent feature of the private equity landscape. LPs know this, which is precisely why governance matters so much. CVs are not going away. The question is whether the processes around them will be made fair.

The same Barometer documented mounting LP concerns about process quality: inconsistent and late disclosures, compressed election windows, and transactions initiated without credible commercial rationale. A separate April 2026 ILPA poll found that a majority of LPs begin to lose confidence in a GP when the discount to the last reported mark exceeds 5% on a full exit — a threshold that many CVs have tested. These are not abstract complaints. They are the conditions that created demand for exactly the kind of framework ILPA has now produced.

The ILPA Response: From Principles to Enforcement

ILPA’s 2023 guidance established principles. The 2026 update operationalizes them. The shift in tone is deliberate and significant.

The document opens with a statement that sets the frame for everything that follows: CVs are “perceived overuse or misuse as an exit mechanism, often initiated with little to no disclosed commercial rationale, coupled with inconsistent and late disclosures, and processes that fail to represent a commitment to GP alignment with existing fund limited partners.” This is not a hedged observation. It is an indictment of a pattern of behavior that has become common enough to require a structural response.

The guidance is organized around three non-negotiable principles:

CORE FRAMEWORK

The Three Principles GPs Must Prove

1. CVs must be deliberate, not default. GPs must demonstrate that a CV was chosen because it best maximizes value for existing LPs, not because it was the most convenient path. This requires presenting the LPAC with a clear commercial rationale alongside the alternatives genuinely considered: trade sales, NAV facilities, mid-life co-investments, strip sales.

2. Rolling LPs must not be worse off. No overall increase in management fees (in absolute dollar terms). No overall increase in carried interest. All crystallized carry and GP sponsor commitment returns from the existing fund must be reinvested in the CV. Roll elections cannot be conditioned on minimum commitment sizes or stapled financing.

3. Information must be symmetric and timely. The ILPA Continuation Fund Disclosure Template, fully completed with all supporting materials, must reach all existing LPs no later than at the time of the sell-roll decision. Election period minimum: 30 business days, with unrestricted data room access throughout.

Each of these principles addresses a specific failure mode that has become common in practice. The “deliberate not default” standard targets CVs launched because the exit environment was difficult, not because the GP had a compelling case for continued ownership. The “no worse off” principle targets fee and carry structures that incrementally disadvantaged rolling LPs. The information symmetry standard targets the scenario, frequently reported by LPs, where new CV investors received better diligence access than the existing LP base being asked to make a sell-or-roll decision.

The Conflicts Section Is the Sharpest Part

On conflicts of interest, the guidance takes its clearest stand. The central problem of a CV is structural: the GP is simultaneously the selling agent (representing the existing fund) and the buying agent (managing the new CV). This cannot be eliminated. But, ILPA argues, it can be properly disclosed and managed, and the burden is entirely on the GP to do so.

The guidance’s most consequential line: “GPs should not rely on any pre-clearance conflict waivers in LPAs.” Every conflict must be identified, disclosed, and brought to the LPAC for explicit approval, regardless of what the fund documents technically permit. This is a direct rejection of the practice, increasingly common as CVs proliferated, of GPs treating LPA pre-clearance provisions as a shortcut around substantive conflict management.

“A GP should not assume its LPAC will always waive CV transactional conflicts. If processes are poorly managed, suffer from incomplete or delayed information, or overly compressed timelines, there is a greater risk that an LPAC will reject or condition its clearing of conflicts.”

The guidance also addresses an increasingly common conflict that has received little formal attention: LPAC members whose affiliated secondaries businesses are independently bidding on the CV. These members sit at the intersection of multiple conflicts, as LP fiduciaries, as potential buyers, and as LPAC gatekeepers for the very transaction they’re evaluating commercially. The guidance makes clear this must be managed separately, with full disclosure and appropriate recusal where warranted.

Regulators are watching. The SEC and the UK Financial Conduct Authority have both intensified scrutiny of GP conflicts in GP-led transactions. ILPA’s guidance effectively pre-empts regulatory intervention by setting an industry standard, but that standard now also serves as a reference point for regulatory expectations.

The Companion Documents: Where Principle Becomes Practice

Three supporting documents give the guidance operational weight in ways that prior ILPA publications did not achieve.

The GP Checklist for LPs converts the guidance into a yes/no disclosure framework that GPs are expected to complete at each stage of the CV process-covering commercial rationale, conflicts, pricing methodology, election mechanics, and LP rights. In practice, this is a document LPs can put in front of a GP at the outset of any CV process and request completed answers before the election clock starts.

The LP Evaluation Questionnaire structures the sell-or-roll decision across four dimensions: process integrity (was a competitive bid run? were advisors conflicted?), economics and valuation (does the price reflect a fairness opinion? how has the multiple trended quarter-over-quarter?), structure and terms (do existing side letters transfer? what are the carry and fee implications on an annualized basis?), and alignment (is 100% of crystallized carry rolling? is portfolio company management participating?).

The CV Transaction Timeline maps the ideal process from initial GP portfolio review through LPAC engagement, bid process, election, and closing. It establishes a critical sequencing principle: LP notification must begin at the moment the GP first incurs CV advisory costs, not once the transaction is substantially structured and the timeline is compressed.

LP MINIMUM STANDARDS - KEY TAKEAWAYS FROM THE GUIDANCE

Require the fully completed ILPA Disclosure Template before the election period begins

Demand no less than 30 business days for the election window, with unrestricted data room access throughout

Confirm that existing side letters transfer to the CV on equivalent or better terms

Verify that management fee and carry structures leave rolling LPs no worse off in absolute terms

Require an anonymized summary of all final-round bids, including pricing structure and key commercial terms

Confirm crystallized carry and GP sponsor commitment returns are reinvested in the CV

Ensure roll elections are not conditioned on minimum commitments or stapled financing

Request independent third-party price validation and a fairness opinion

What Changes and What Doesn’t

ILPA’s guidance is best practices, not regulation. No GP is legally compelled to follow it. But that framing understates its practical significance in several ways.

First, the document now serves as a reference standard in LPAC negotiations. LPs who arrive at an LPAC meeting with ILPA’s checklist and a list of gaps to fill have a credible, industry-endorsed framework behind them. GPs who deviate from it must explain why, which is a substantially higher bar than the prior norm of simply presenting a CV on whatever terms the GP preferred.

Second, LPAC dynamics have shifted. The guidance explicitly empowers LPACs to condition conflict approval on process remediation, on better information, longer timelines, clearer rationale. An LPAC that uses this authority is not being obstructionist; it is following published best-practice guidance. That changes the politics inside these transactions.

Third, the regulatory environment is moving in the same direction. Both the SEC and the FCA have signaled increased focus on GP-led transaction conflicts. ILPA’s guidance effectively creates an industry compliance baseline that regulators can reference, and that GPs ignore at their own risk.

For GPs, the practical implication is front-loaded investment. Early LPAC engagement, earlier LP notification, fuller documentation of alternatives considered, and a standing CV policy shared with LPs during fundraising. The guidance signals that the era of launching a CV with limited commercial context and a compressed election window is structurally over, not because it will always be stopped, but because the friction and reputational cost of doing so will increasingly outweigh the convenience.

For LPs, the guidance provides both a minimum standard and a negotiating tool. The side letter implications are particularly important: LPs should now incorporate minimum CV election periods, mirror reporting requirements, information-sharing floors, and mirror tax treatment into their standard side letter templates for future commitments. The time to negotiate these protections is during fundraising, not when the CV process is already underway.

The Structural Bet

The 2026 guidance arrives at a moment when the continuation vehicle market is, by most projections, still in its growth phase. Projections from multiple sources suggest CVs could represent 30% to 40% of all private equity exits within two years. The $3.8 trillion backlog of unrealized assets is not clearing quickly, and for the 2018–2021 vintages under the most LP pressure, CVs remain one of the few mechanisms that can return capital without forced sale conditions.

The Coller Barometer data points to why this matters beyond the immediate cycle: 69% of LPs expect CV activity to hold or increase even as exit markets recover. This is not a market expecting CVs to revert to a niche use case once conditions normalize. It is a market pricing in CVs as a permanent feature of how private equity works, and adjusting its governance expectations accordingly.

ILPA’s 2026 guidance is, in that sense, not just a response to current market conditions. It is the industry’s attempt to build the institutional infrastructure, standards, checklists, templates, timelines, that a permanent, high-volume CV market requires to function with genuine LP-GP alignment rather than the adversarial friction that has characterized too many transactions in the recent cycle.

The comment period closes August 5, 2026. Both LPs and GPs have until then to shape the final version. Given what’s at stake, the participation rate should be high.

Sources: ILPA 2026 Continuation Vehicle Guidance (comment period draft); Coller Capital Global Private Capital Barometer, 44th Edition, Summer 2026; Bain & Company Private Equity Midyear Report 2026; Carlyle AlpInvest, Global Private Markets Quarterly; Lazard 2025 Secondary Market Report; Ares Management secondaries research. Market volume data from Jefferies and Lazard annual secondary market reviews. All figures in USD unless otherwise noted. This article reflects analysis and editorial interpretation by Secondary Scoop; it does not constitute investment advice.