The Next Secondaries Boom: Infrastructure

That gap between asset life and fund life is obvious, and the continuation vehicles are the natural answer.

“We’re in the greatest infrastructure capital deployment environment in the history of time.”

That is not a line from a fundraising deck. It is what Connor Teskey, CEO of Brookfield Asset Management, said during the firm’s Q1 2026 earnings call. His reasoning is straightforward: AI adoption, digitalization, rising energy demand, and deglobalization are all creating sustained, simultaneous demand for capital. Data centers, power generation, transmission networks, fiber, cooling systems — the physical backbone of the modern economy needs to be built, and it needs to be built now.

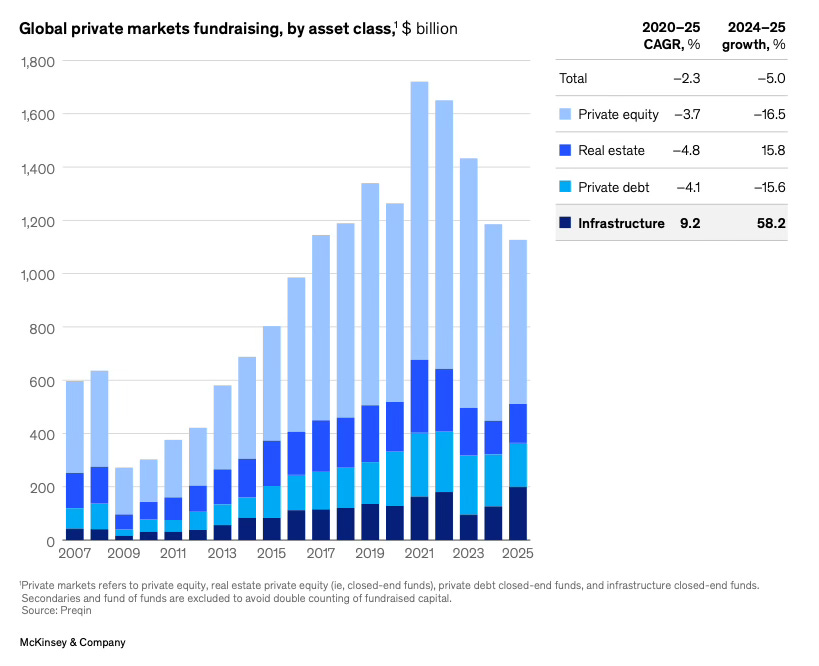

The numbers back him up. According to McKinsey’s Global Private Markets Report 2026, global infrastructure fundraising hit a record of nearly $200 billion in 2025, up 58% over 2024. In Europe alone, €491 billion has been raised across 679 funds since 2017, according to PitchBook. LP appetite is not slowing: 51% of LPs surveyed by McKinsey plan to increase infrastructure allocations over the next three years, more than any other asset class, ahead of buyout at 35% and real estate at 30%.

The primary market story is well documented. What is less discussed is what all that vintage capital means for the secondary market over the next five years.

The mismatch

Infrastructure funds run on a 10-year clock. The assets inside them do not.

Toll roads, energy grids, renewables, fiber networks, data centers — these are projects where large upfront capital takes 20 to 30 years to fully recover. Much of the value creation happens well after year ten. As Faraz Qureshi, head of infrastructure secondaries at BNP Paribas Asset Management, told PitchBook in May 2026: these assets have 10 to 15 more years of value creation ahead of them once a typical fund reaches maturity.

The funds raised in the 2017 to 2020 boom are hitting that wall now. And unlike software or buyout assets, you cannot simply sell a half-built renewable energy platform or a data center three years into a 20-year development cycle at a price that makes sense. Traditional exit routes are not designed for this.

Why continuation vehicles make sense here

A GP-led continuation vehicle lets a manager move assets from a maturing fund into a new structure. Existing LPs can cash out or roll their exposure. New capital comes in to support the asset through the rest of its development cycle.

The market is already reflecting that logic. According to PitchBook, infrastructure secondary deal volume hit $25 billion in 2025, more than double the $11 billion transacted in 2023. GP-led deals reached a record $14.6 billion in 2025, with EMEA accounting for roughly 30% of flow, according to Campbell Lutyens in its Q4 2025 Infrastructure Market Report. Dedicated infrastructure secondaries fundraising more than doubled to $11.5 billion globally last year. PJT Partners, in its FY 2025 Secondary Market Insight, projects the market will reach $45 billion by 2030.

Worth noting: the motivation behind GP-leds is also shifting. According to Qureshi, portfolio rebalancing is largely done. What is driving continuation vehicles now is portfolio growth.

The demand side

Pressure is building from both directions.

GPs with maturing funds need structures that fit assets with long development cycles. On the buy side, appetite is growing for different reasons. As Qureshi told PitchBook, investors still ramping up their infrastructure portfolios are turning to secondaries to deploy capital, access distributions, and build diversified exposure that is simply not available on day one in the primary market.

With primary fundraising at record levels and LP appetite still growing, the pipeline of funds that will eventually need secondary solutions is only expanding. The 2017 to 2020 vintage wave is the first chapter. Funds raised in 2021, 2022, and 2023 have not arrived yet.

What to watch in 2026

That gap between asset life and fund life is not going away. If anything, as infrastructure mandates expand into more complex, capital-intensive verticals, it is getting wider.

$25 billion in infrastructure secondaries in 2025 looks less like a ceiling and more like a starting point. 2026 is shaping up to be a significant year for GP-leds, with strong appetite from both GPs needing liquidity solutions and LPs looking to build infrastructure exposure through the secondary market. And the funds from the next wave of vintages have not even arrived yet.