The Rise of Continuation Vehicles in Private Credit

Continuation vehicles made up around 60 percent of credit secondaries volume in 2025. Here is what is driving the shift, and which deals are setting the pace.

Continuation vehicles have moved from the edge of private credit to its center. In 2025 they accounted for roughly 60 percent of credit secondaries transaction volume, and the first half of 2026 has brought a steady run of closings from Carlyle, Blue Owl, Pantheon, and Ares. The structure that private equity used to manage liquidity is now doing the same job for private credit, and it is scaling faster than the equity market did.

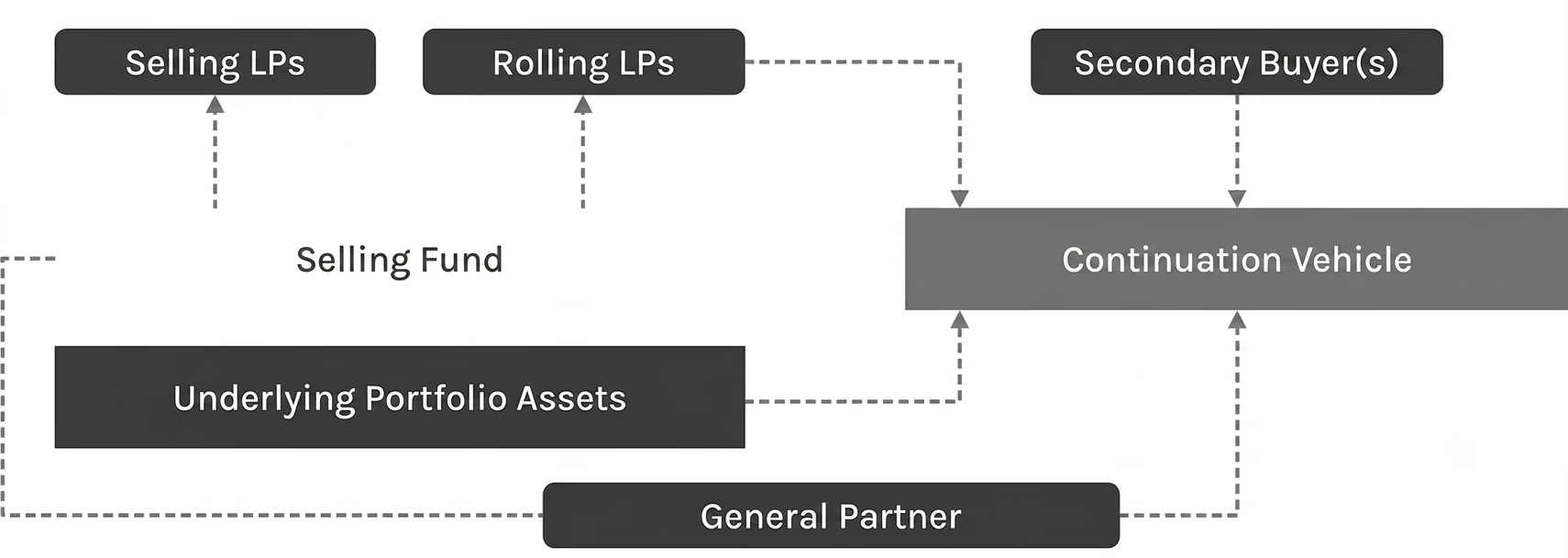

What is a continuation vehicle?

A continuation vehicle is a new fund a manager creates to buy assets out of one of its existing funds. Investors in the original fund choose to cash out at an agreed price or roll their interest into the new vehicle. The manager keeps running the assets and usually commits fresh capital alongside a lead secondary buyer.

In private credit, the point of the structure is liquidity. A continuation vehicle lets a manager return capital to investors who want it while holding performing loans for longer on behalf of those who stay in. Unlike private equity continuation vehicles, which tend to center on one or a few prized assets, credit continuation vehicles are usually diversified, full-fund pools of loans.

Why continuation vehicles are growing in private credit

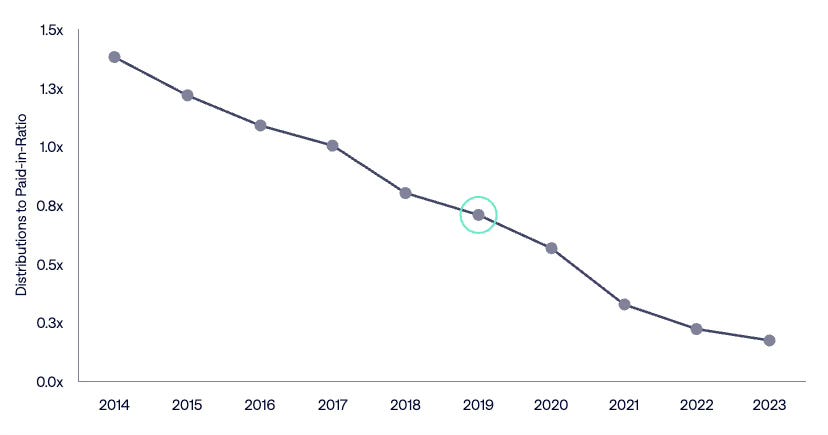

The driver is a gap between when loans mature and when investors expect their money back. Private credit funds typically run on an eight-year term with a four-year investment period. Loans written late in that window can outlast the fund, and slower repayment has pushed distributions down. Ares estimates that 2019-vintage private credit funds have returned only about 70 percent of invested capital so far, a DPI of roughly 0.7x.

Private Credit DPI Multiple by Vintage

When distributions slow, managers need another way to deliver liquidity. Continuation vehicles supply it without forcing a sale of good loans into a weak market. The same structure lets managers keep assets they still rate highly, and it can open conversations that feed the next fundraise.

Adoption has been fast. As Luca Salvato, Partner and Co-Portfolio Manager at Ares Credit Secondaries, put it:

“Private credit continuation vehicle transactions have been embraced at a significantly faster pace than we have historically seen in other secondary asset classes. The growth in capital formation now enables GPs to adopt this technology at scale and offer a new and attractive liquidity option to their LPs.”

How big is the credit secondaries market?

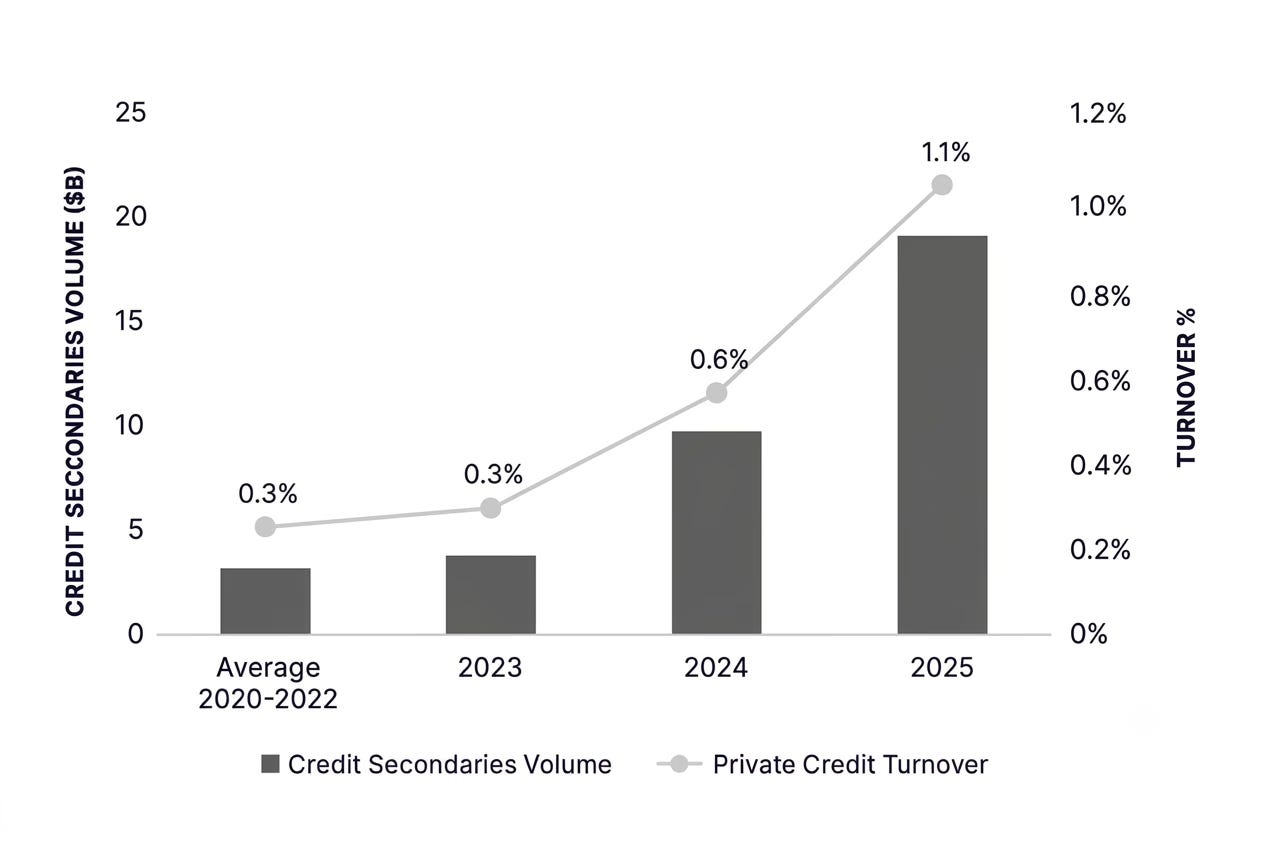

Credit secondaries are one of the fastest-growing segments of private markets, though they remain small next to the roughly $2 trillion private credit market behind them. Total credit secondaries volume reached about $20 billion in 2025, close to double the prior year, a figure that McKinsey, Carlyle AlpInvest, Apollo, and Ares all converge on.

GP-led activity, which in credit is mostly continuation vehicles, did most of the work. McKinsey reports GP-led volume tripled year over year to about $12 billion in 2025, or 60 percent of the total. Dedicated capital has followed. Carlyle AlpInvest estimates around $20 billion of dry powder is now committed to credit secondaries, and Ares raised $7.1 billion for its credit secondaries strategy in January 2026, its largest inaugural fund to date.

What LP demand looks like

The clearest signal is deal size, and 2026 has produced a steady run of large closings. The year opened with Crescent Credit Solutions VII CV, a $3.2 billion vehicle led by Pantheon and announced in January 2026, which stands as the largest credit continuation vehicle closed to date. More have followed:

Carlyle and Content Partners closed a single-asset continuation vehicle on 16 June 2026, giving investors in Carlyle’s Credit Opportunities funds the choice of liquidity or continued exposure to a film and television catalogue.

Blue Owl led Veld Capital’s 355 million euro credit continuation vehicle, reported on 15 June 2026, one of a growing set of European credit CVs.

Pantheon led a $1 billion continuation vehicle for Audax Private Debt in May 2026, built around first-lien senior secured loans.

Ares led Antares Capital’s second continuation vehicle in March 2026, at more than $1.7 billion across 300 first-lien loans.

The European angle is worth watching. Ares has pointed to the activation of the European credit CV market, with several leading managers running scaled processes through 2025 and early 2026. The Blue Owl deal with Veld is a recent example.

Outlook

Forecasts vary but point the same way. Apollo expects credit secondaries to reach $50 billion or more within two to three years. Carlyle AlpInvest projects the market will pass $80 billion by 2030, with GP-centered deals, led by continuation vehicles, making up the larger share at around $55 billion. Every major house expects continuation vehicles to keep gaining ground as more managers treat them as a repeatable tool rather than a one-off fix.

Two things will shape how far the trend runs. The first is capital. At current deployment rates, Carlyle AlpInvest estimates only six to nine months of dry powder runway, so continued fundraising is needed to meet demand. The second is discipline. Because upside on credit is capped, returns are set largely at entry, which puts the weight on pricing and on underwriting the underlying loans rather than on a headline discount.

For now the direction is clear. Continuation vehicles have become the main engine of credit secondaries, and the deal flow of early 2026 suggests the market is still early in its growth.

Frequently asked questions

Are continuation vehicles a sign of distress? Usually not. In credit they are mostly used to manage fund life and provide liquidity around performing loans, not to offload troubled assets.

How is a credit continuation vehicle different from a private equity one? Private equity CVs tend to focus on one or a few assets. Credit CVs are usually diversified, full-fund portfolios of loans.

Who invests in these vehicles? Specialist credit secondaries funds lead most deals, often alongside the original manager, who rolls economics and sometimes commits new capital.

Sources:

Ares Management, “The Rise of Continuation Vehicle Transactions in Credit Secondaries” (March 2026)

Carlyle AlpInvest, “Credit Secondaries: Stepping into the Spotlight” (June 2026)

Secondaries Investor, “Blue Owl leads Veld Capital’s 355m credit CV” (15 June 2026)

Antares and Ares (March 2026); Crescent and Pantheon (January 2026)

Strong synthesis of where the market is Tomas, and the right frame on CVs as infrastructure and not just a liquidity fix.

The structural point worth adding: as continuation vehicles become a repeatable, standard tool rather than a one-off, the frictions that follow aren't just commercial; they're operational.

Settlement cadence, cap-table transparency, NAV reporting across multi-counterparty closings, and LPAC-ready audit trails all become the operational surface area that determines whether a CV program scales or collapses under its own complexity.

The same dynamic is why the programmable-liquidity layer being built beneath this market matters. Tokenized of CV interests (with immutable cap tables, automated distribution waterfalls, on-chain settlement) doesn't change the economics of the deal. It changes whether the operating model can handle volume without bespoke, manual workflows on every transaction.

The firms that solve that layer first will have a structural advantage in how fast they can deploy CV capital relative to peers. We believe that's the inflection point to watch in 2026–2027.

Full disclosure, this is exactly the problem our new Programmable Liquidity practice at NextFi Advisors is designed to help secondaries advisors and GPs solve.

--> nextfiadvisors.com/programmable-liquidity

Would love to know your thoughts.