The Secondaries Market Has a Discount Obsession. That May Be the Wrong Instinct.

Discount to NAV is secondaries' most cited metric. According to Lexington Partners, it may also be its most misleading.

Ask most LPs what they look for in a secondary fund manager and discount to NAV will appear early in the answer. It is the shorthand the industry has settled on: a simple expression of how much protection a buyer is getting relative to reported asset value. The wider the discount, the safer the entry. That is the conventional logic.

Lexington Partners, one of the largest dedicated secondary buyers with over $84 billion in total capitalization, takes a different view. In a June 2026 research note on secondary transaction underwriting, the firm makes a direct argument against over-indexing on discount, and makes the case that the metric, applied without context, can actively mislead investors evaluating secondary funds.

WHY “MORE DISCOUNT” DOES NOT MEAN “BETTER VALUE”

The core of Lexington’s argument is straightforward: discount is the inverse of price, and price is a reflection of projected returns and asset quality. A very high discount, in their framing, frequently signals that an asset has limited upside, potentially low-quality, structurally challenged, or already fully valued at current NAV. These transactions offer fewer ways to win: the initial price is doing most of the work, and there is little appreciation potential to carry the investment forward.

“When I see a very high discount, it can often mean that there’s little or no upside in the assets and probably lower asset quality. As the initial price is driving most of the return, these types of transactions inherently have fewer ways to win.”

TAYLOR ROBINSON, PARTNER, LEXINGTON PARTNERS

The firm’s position, developed over 35 years of secondary investing, is that the vast majority of value generated in secondary deals comes from asset appreciation, not from the entry discount itself. Discount, in their view, functions as an “insurance policy” against value erosion and a mitigant of private equity’s initial J-curve, but it should not be the primary driver of investment selection.

This distinction matters most when evaluating what Lexington calls the reliability of reported NAV. A uniform discount applied across a portfolio assumes that all NAVs are equally conservative, that valuation timing is consistent, and that growth prospects are comparable. In practice, none of those conditions reliably hold. Paying 90 cents on the dollar for a conservatively marked, high-growth portfolio may generate better outcomes than paying 80 cents for one that is fully valued or structurally challenged, even though the second deal looks “cheaper” on a headline basis.

WHAT LEXINGTON LOOKS FOR INSTEAD

The framework Lexington articulates in the paper centers on bottoms-up underwriting: starting from the underlying companies in a portfolio, assessing growth trajectory, leverage, exit optionality, and sponsor quality, before arriving at a price. The discount emerges from that process; it is not the input.

SECONDARY PRICING: WHAT ACTUALLY GOES INTO IT

Asset underwriting and GP quality assessment

Portfolio company growth outlook and leverage levels

Exit optionality and capital markets receptivity

Vintage year dynamics and sector cyclicality

Unfunded commitment obligations

Transaction structure, including deferred pricing mechanics

Capital availability and competitive dynamics

The practical implication for investors evaluating secondary managers: Lexington suggests asking what unlevered returns a manager is presenting at investment committee, not what average discount they are targeting. The question reorients the conversation from entry mechanics to forward return expectations, which is where actual value creation is measured.

THE STRUCTURAL SHIFT BEHIND THE ARGUMENT: GP-LEDS AND DEFERRED PRICING

The discount debate does not exist in a vacuum. Two structural trends in the 2025 secondary market give it additional urgency.

First, GP-led transactions, which now represent a significant share of total secondary volume, price differently from LP-led deals. According to Lexington’s data, high-quality GP-led continuation vehicles are generally priced at or near par, sometimes at a premium. A CV pricing at a significant discount, in this framing, is more likely to reflect a challenged asset or a riskier value creation profile than a seller in distress offering a bargain. This inverts the assumption that discount equals safety in the GP-led segment specifically.

Second, deferred pricing structures have become widespread enough to distort headline discount figures. An estimated 23% of secondary transactions completed in 2025 included a deferred pricing component, according to the Jefferies Global Secondary Market Review. These arrangements, where a portion of the purchase price is paid at close and the remainder at a later date, allow sellers to show better optical pricing while buyers retain capital deployment flexibility. The effect is that reported “prices” in any given quarter may not reflect the economics that actually cleared.

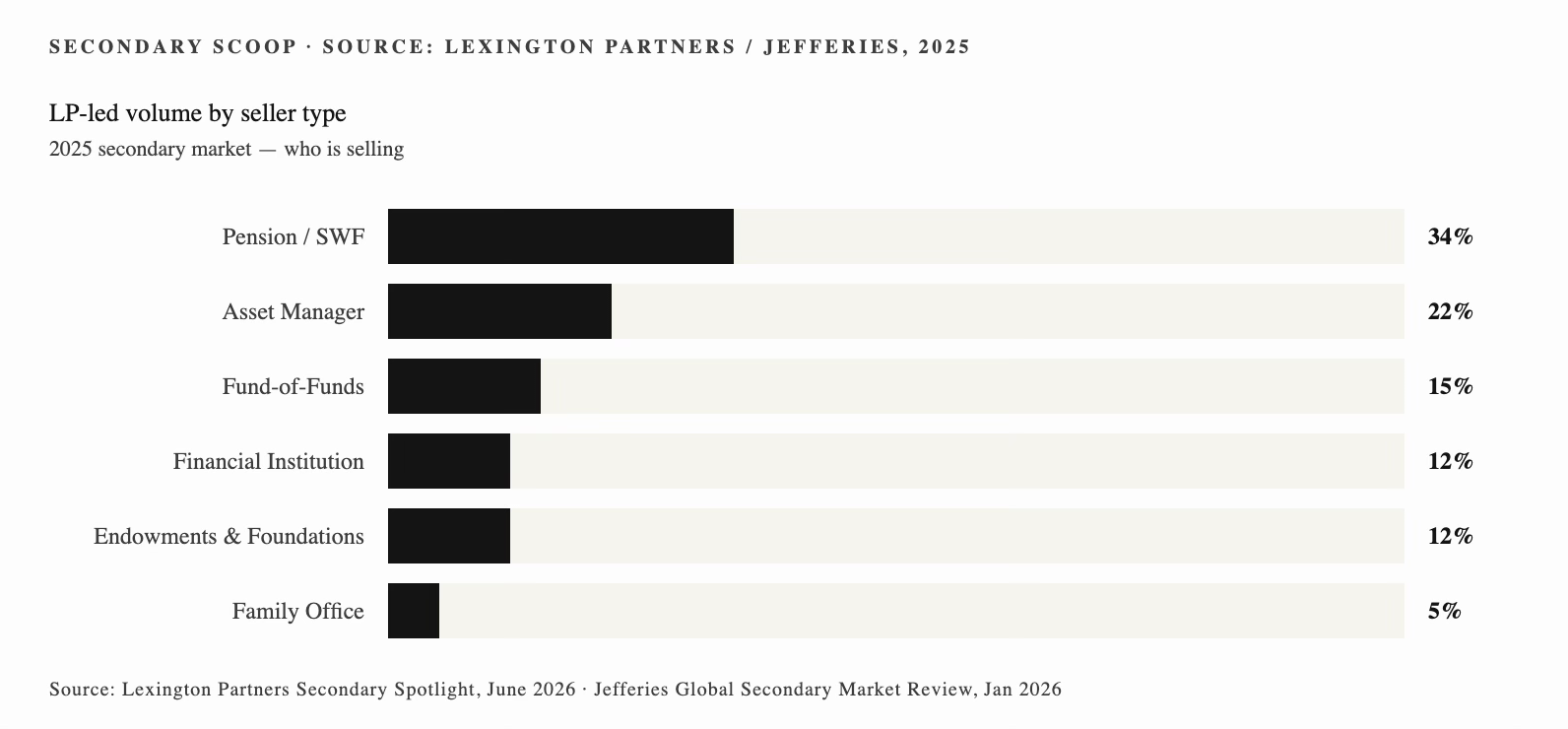

THE NORMALIZATION SIGNAL: 60% OF 2025 SELLERS WERE REPEAT PARTICIPANTS

Alongside the discount argument, the paper contains a data point that speaks directly to how the secondary market has structurally evolved. In 2025, approximately 60% of LPs who sold in the secondary market were repeat sellers, and Lexington observed a meaningful increase in sellers accessing the market as part of a systematic, active portfolio management program rather than in response to a discrete liquidity need.

This matters for how buyers underwrite supply. A market where the majority of sellers are repeat, programmatic participants behaves differently from one driven by distress or opportunistic liquidations. It is more predictable, more efficiently priced, and increasingly competitive. It also reinforces the broader industry thesis, one that Secondary Scoop has tracked closely, that secondaries have moved from a niche liquidity mechanism to a standard portfolio management tool for institutional investors.

THE AI QUESTION

Lexington’s note also weighs in on AI’s role in secondary underwriting, with a framing that resists both dismissal and hype. The firm’s view is that AI meaningfully accelerates tops-down processes, aggregating information, scenario modeling, memo drafting, but does not substitute for the bottoms-up relational work that generates actual informational edge. The critical last mile of secondary underwriting, in their assessment, depends on direct dialogue with PE sponsors and the accumulated pattern recognition that comes from decades of repeat exposure to the same managers and assets.

The implication is pointed: firms that have recently entered the secondary market and are positioning AI as a core underwriting differentiator may be overstating what the technology can do in an environment where the most valuable information is not in any database.