The Zombie Fund Problem Has a Market Solution. The Industry Just Won't Say It.

Coller Capital's Summer 2026 Global Private Capital Barometer says 54% of LPs expect zombie exposure to grow. The secondary market is the most direct exit — but it barely gets mentioned.

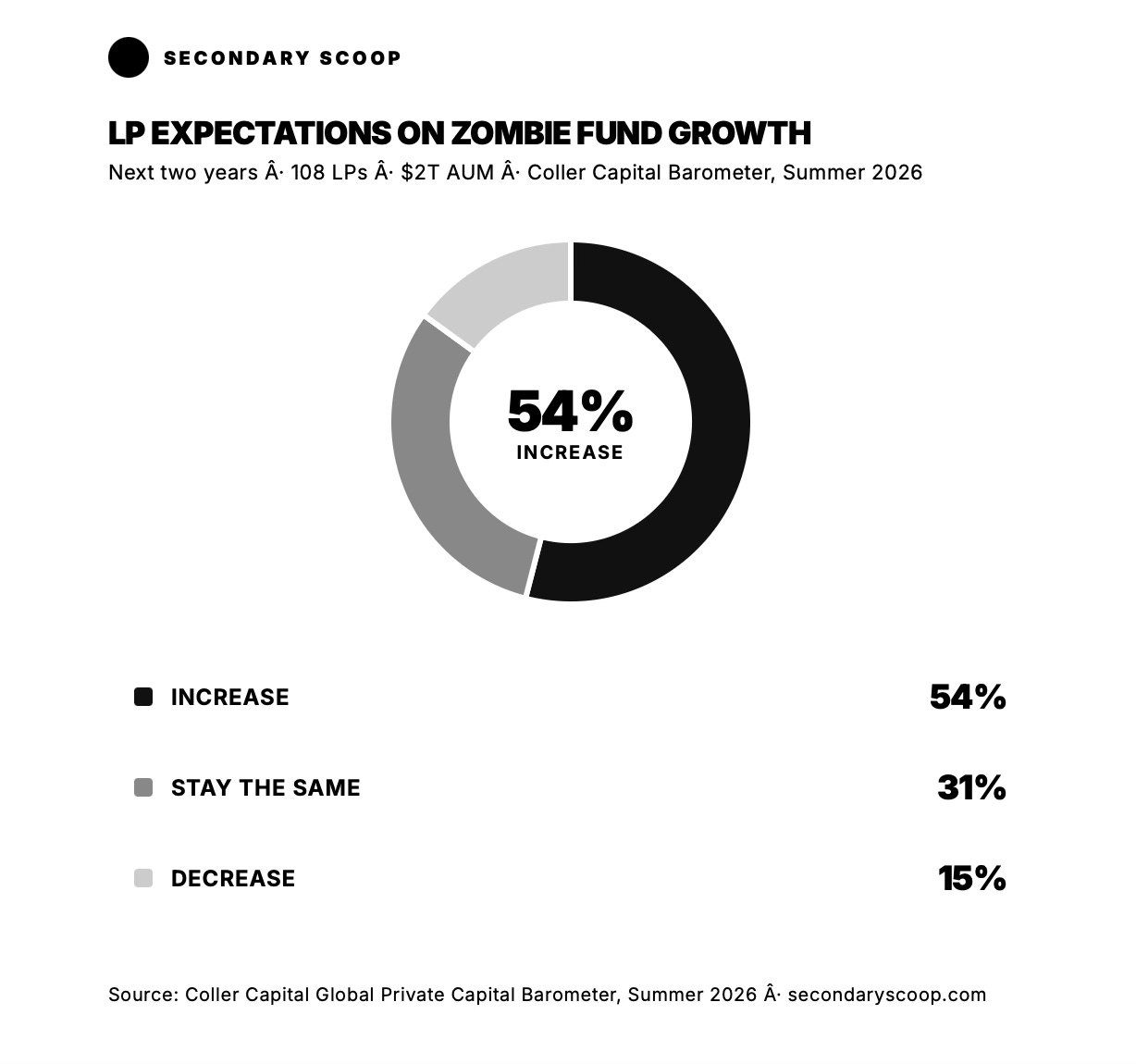

A new data point from Coller Capital’s Summer 2026 Global Private Capital Barometer deserves more attention than it’s getting: over half of limited partners — 54% — expect the number of zombie funds in their portfolios to increase over the next two years. That’s up sharply from 2024, when 28% anticipated an uptick.

The framing in most coverage, including a Bloomberg piece published this week, lands on fee negotiation. LPs prefer management fee step-downs. Some want economic term resets. A minority would push for manager removal. The story gets told as a governance problem with a governance solution.

That framing is incomplete.

What a zombie fund actually is — and why it’s getting worse

A zombie fund is a private equity vehicle where the GP has extended the fund’s life beyond its original term, typically to preserve management fee income, rather than to pursue genuine value creation. The underlying assets haven’t been sold. The clock has stopped. And the LP is stuck.

The conditions that created today’s zombie cohort are well-documented. Private equity firms deployed capital aggressively between 2019 and 2022, often at elevated entry multiples, into a low-rate environment that no longer exists. When the Federal Reserve began raising rates in 2022, the exit environment seized up. IPO markets closed. Strategic buyers pulled back. Sponsor-to-sponsor deals slowed. The assets stayed on the books.

Bain & Company’s 2026 midyear private equity report is direct about what that means: a growing number of companies are essentially trapped in portfolios. Global deal count has decreased in the first half of 2026, and the deal comeback that many expected this year has not materialized — market uncertainty, combined with concerns about AI disruption to software valuations, has kept buyout activity muted.

The result: funds that should have wound down are still running. And according to Coller’s survey of 108 LPs overseeing approximately $2 trillion in assets, Eric Foran, a partner at Coller, described the 54% figure as higher than he would have anticipated.

The governance framing misses the supply signal

When zombie funds proliferate, the standard LP response — as Coller’s data confirms — is to negotiate. Fee step-downs are the preferred tool for 54% of respondents. Economic term resets come in at 18%. Just 11% would push for manager removal, and only 6% would refuse a fund extension outright.

That preference for non-confrontational resolution makes sense in individual fund relationships. GPs control information flow, future fund access, and co-investment pipelines. LPs have structural incentives to stay cooperative.

But at the portfolio level, fee negotiation doesn’t solve the underlying problem. It reduces the cost of being stuck. It doesn’t unstick you.

The secondary market does.

An LP with zombie fund exposure has a limited set of options: wait for exits that may not come on any predictable timeline, apply governance pressure that most LPs are structurally reluctant to exercise, or sell the position. The secondary market is the only mechanism that converts an illiquid, fee-generating stranded asset into cash — at a price, but with finality.

This is a supply signal. When zombie fund exposure increases across LP portfolios at scale, the inventory available for LP-led secondary transactions increases with it. The discount may be steep — zombie assets carry uncertainty about exit timing, residual value, and GP motivation — but for an LP that has already written down its expectations for DPI from a given fund, a discounted exit is often preferable to an indefinite hold.

The secondary market’s role in the zombie cycle

The Coller Barometer makes the connection partially, noting that continuation vehicles provide one mechanism for GPs to avoid saddling existing LPs with aging assets — and that 40% of LPs expect CV activity to keep growing even when traditional exits improve. But CVs solve the GP’s problem: they create a new vehicle, raise fresh capital, and transfer the best assets forward. What they leave behind — the assets that didn’t make the cut for the CV — can become the core of a zombie fund.

The LP-led secondary market addresses the other side of that equation. Rather than waiting for a GP to propose a solution, LPs can take their own liquidity. Secondaries buyers have developed increasing sophistication around distressed and tail-end fund situations, and tail-end portfolios have become a recognized sub-segment of the LP-led market.

The irony in Coller’s data is worth noting explicitly: Coller is itself a secondaries buyer, and the survey is produced by the Coller Research Institute. The firm has a commercial interest in LP-led deal flow. That doesn’t make the data wrong — but it does make it notable that the report frames zombie funds primarily as a governance challenge rather than a liquidity one. The secondary market solution is present in the data. It just doesn’t make the headline.

What this means for secondaries volume

The practical implication is straightforward. If 54% of LPs are anticipating increased zombie exposure, and LP-led secondaries represent the most direct liquidity mechanism available, the pipeline for tail-end and restructuring transactions in 2026 and 2027 is likely to be larger than current market estimates reflect.

That volume won’t announce itself. Zombie fund sales tend to be quiet — LPs don’t publicize the fact that they’re selling stranded exposure, and GPs have little incentive to facilitate visibility into the process. But the underlying pressure is building, and it’s measurable. The Barometer just measured it.

The secondary market is not incidental to the zombie fund problem. For many LPs, it’s the solution. The sooner that connection gets named explicitly, the more efficiently capital will move.

Source: Coller Capital Global Private Capital Barometer, Summer 2026 (44th Edition). Bloomberg / Preeti Singh, June 22, 2026.