The venture market is not recovering evenly. It is becoming more concentrated around a small group of AI companies raising record amounts of private capital.

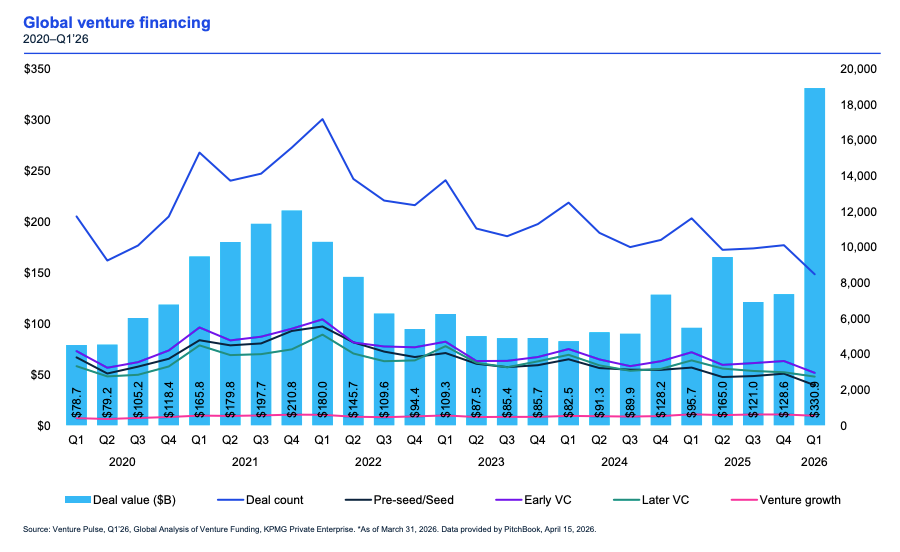

Global VC investment reached $330.9 billion in Q1 2026, but most of that came from a small number of big AI rounds, including OpenAI, Anthropic, xAI, Waymo, and Databricks. KPMG reports just five US companies accounted for $188.6 billion of total global VC investment during the quarter.

This also impacts secondaries, as private company valuations are rising much faster than liquidity. AI companies are raising huge rounds, staying private longer, and pulling in more and more capital.

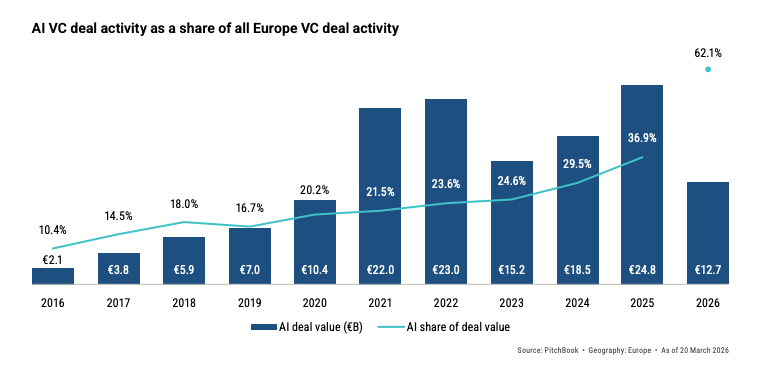

In Europe, PitchBook reports that AI accounted for 61.3% of all VC deal value in Q1 2026, with €13.4 billion invested in AI deals in a single quarter.

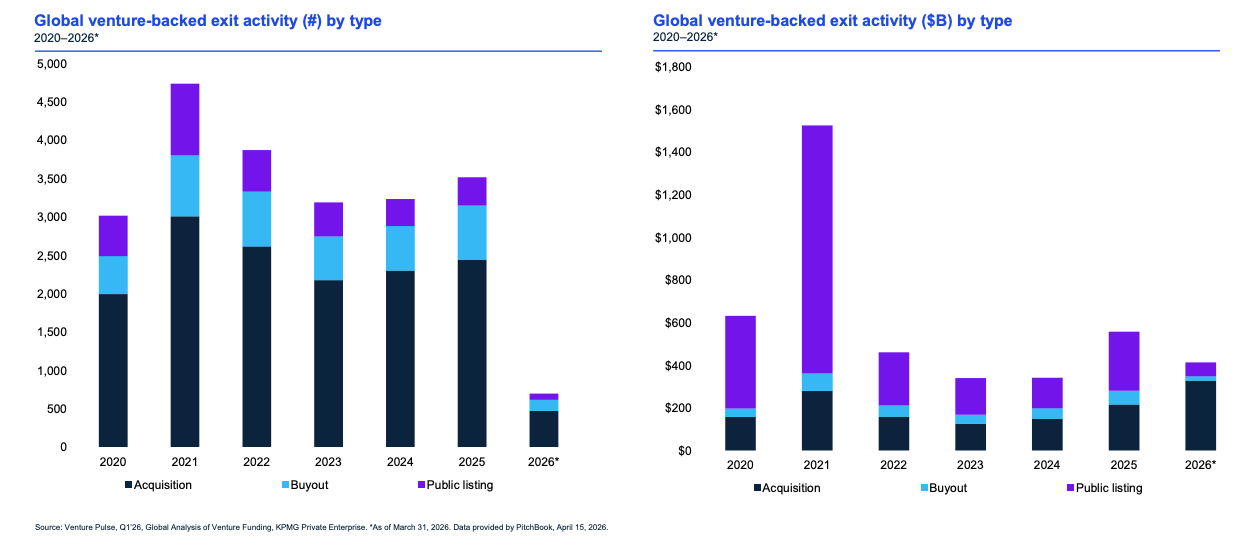

The problem is not that AI companies cannot raise money. The problem is that many investors still cannot exit. The IPO market was expected to improve in 2026, but the latest market reports show that the US IPO market came to a “grinding halt” after the conflict in the Middle East began. J.P. Morgan also noted that market volatility and concerns around AI disruption have made the IPO environment more difficult again.

This is where venture secondaries start to show their value.

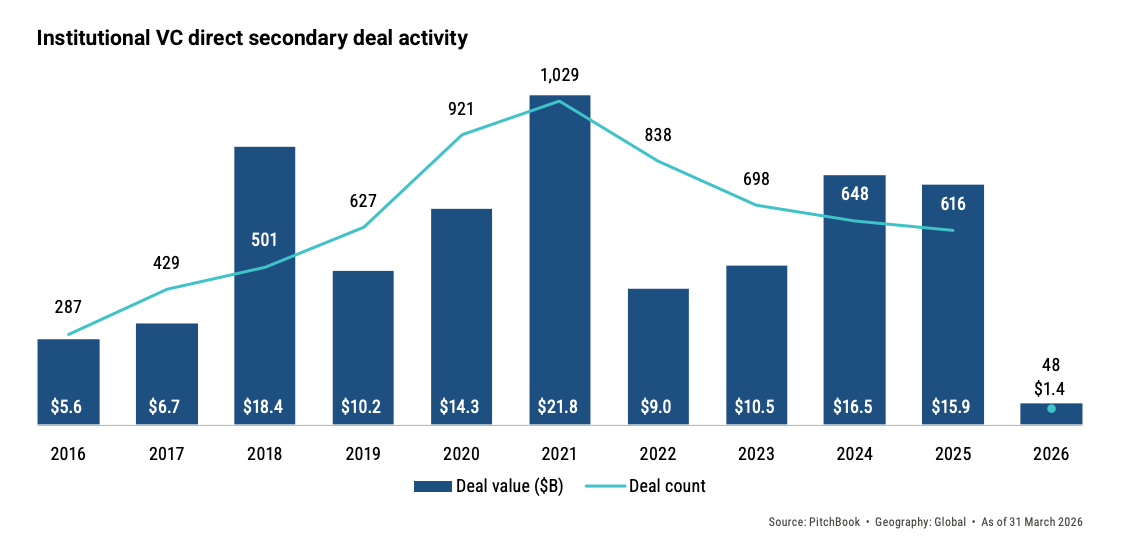

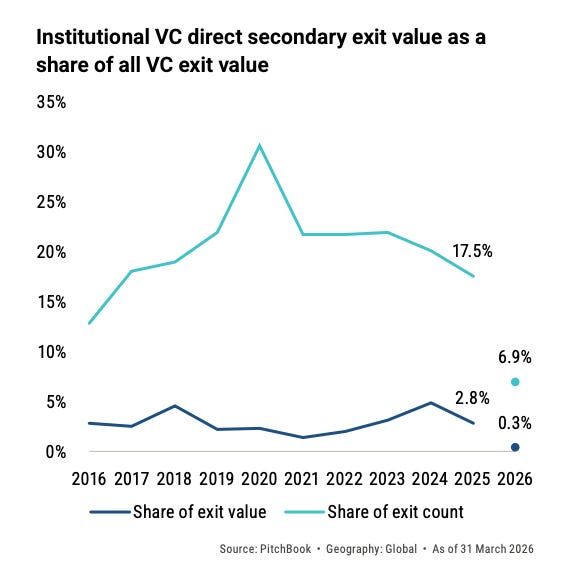

PitchBook also shows that global institutional VC direct secondary deal value stayed strong at $15.9 billion in 2025, even while broader exit markets remained uncertain. Europe accounted for about 15% of that activity.

The logic is simple. If the biggest AI companies keep raising private money and delay going public, early employees, angel investors, seed funds, and early VCs still need ways to turn paper gains into real cash. And if IPOs and M&A remain slow, LPs also need ways to rebalance portfolios without forcing companies to sell too early.

The next wave of venture secondaries won’t just happen because struggling investors need cash. It’ll also happen because some startups are doing so well that they’ve stayed private for a very long time and become extremely valuable.

AI companies are making this even more common. The hottest companies are raising huge amounts of private money, so they don’t feel pressure to go public anytime soon. But investors still want a chance to own part of them.

So instead of waiting for an IPO, people buy and sell existing shares privately through “secondaries.”

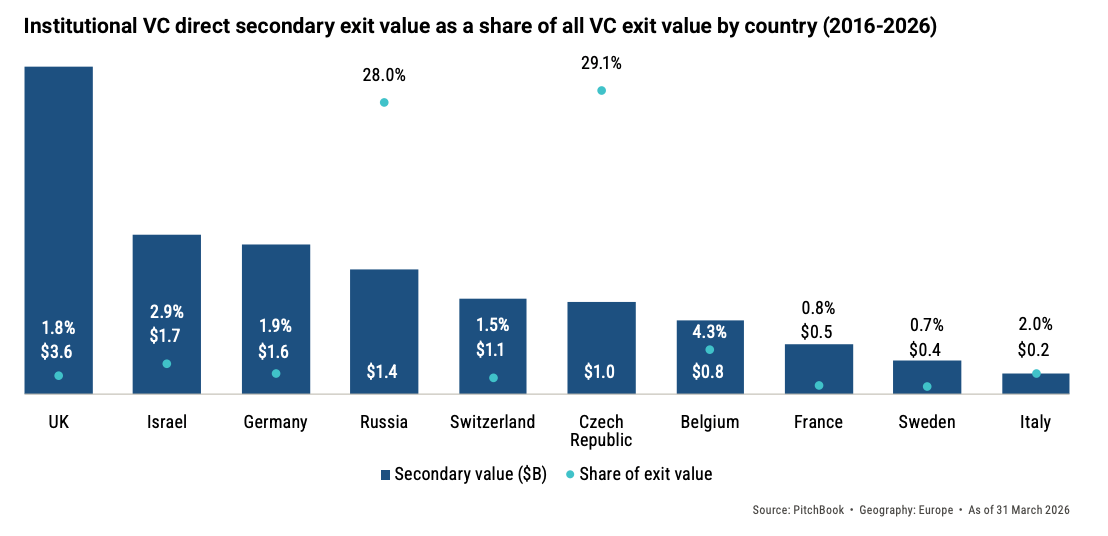

Europe Offers A Preview of Where the Market May Go

PitchBook estimates that the European institutional VC direct secondaries market could reach $47.5 billion in its base-case scenario. There are still obstacles around governance, transfer approvals, and pricing transparency, but the market direction is becoming clearer.

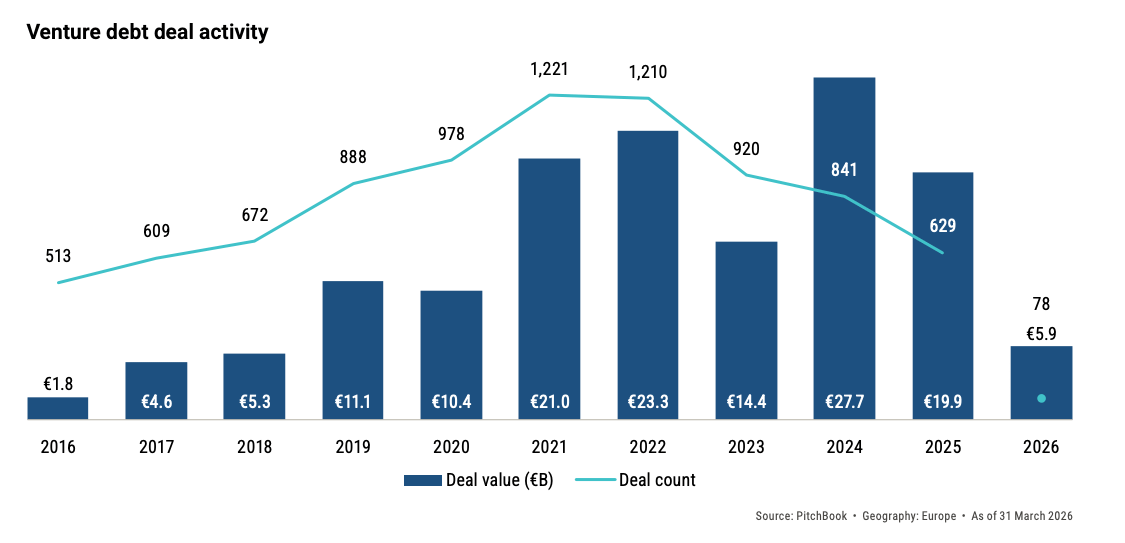

Another important piece of the story is venture debt.

The New Liquidity Mix: Equity, Debt, and Secondaries

European venture debt reached €5.9 billion in Q1 2026, while average deal sizes jumped from €35.9 million in 2025 to €90.5 million this year. AI companies represented 56.9% of total venture debt deal value.

Venture-backed companies are no longer depending on one liquidity path. They are raising mega-rounds, adding venture debt, delaying IPOs, and creating greater demand for partial-liquidity solutions along the way. Direct secondaries are becoming the pressure-release valve for the venture market.

The bottom line is that AI is not only changing how venture capital is invested. It is also changing how venture investors eventually get liquidity. The more money flows into a small number of private AI leaders, the more important secondaries become for founders, employees, early investors, and LPs.

In the past, when people sold shares in private startups, it often looked like they were losing confidence and wanted to leave.

Now it often means the opposite: they invested early in a company that became very successful, and their shares are valuable enough that others want to buy them.