While Markets Wobbled, StepStone Quietly Assembled Its Biggest Secondaries Pipeline Ever

Record fundraising, a $2.5 billion PE secondaries pipeline awaiting activation, and €29 billion under management in Europe: StepStone's Q4 FY2026 results are not just a US story.

In a quarter characterized at the macro level by geopolitical shocks, AI disruption, and growing media scrutiny of private credit, StepStone Group reported its strongest financial results in company history — and placed secondaries at the center of its growth narrative.

Founded in 2007 by Monte Brem, Thomas Keck, and Jose Fernandez — veterans of Pacific Corporate Group — StepStone began as a conflict-free private markets advisory serving institutional investors seeking bespoke portfolio construction. It listed on Nasdaq in 2020 and has since grown into one of the largest private markets platforms in the world. As of March 31, 2026, the firm was responsible for approximately $885 billion of total capital, including $233 billion in assets under management. Its client base spans the world’s largest public and private pension funds, sovereign wealth funds, insurance companies, endowments, foundations, family offices, and private wealth clients. The firm operates across four core asset classes — private equity, infrastructure, private debt, and real estate — through a combination of separately managed accounts, commingled funds, and, increasingly, semi-liquid evergreen vehicles targeting the private wealth channel. It employs approximately 1,090 people across 31 offices globally.

The Washington-based firm generated nearly $14 billion in capital formation in Q4 alone, capping a full fiscal year of $38 billion in gross AUM additions — its best twelve-month period on record. Fee-related earnings surpassed $100 million for the first time, reaching $105 million at a 40% margin. For investors and managers watching the secondaries space, the numbers carry a clear signal: the market for private equity secondaries — both LP-led and GP-led — remains structurally robust, institutional demand is accelerating, and the largest platforms are expanding capacity accordingly.

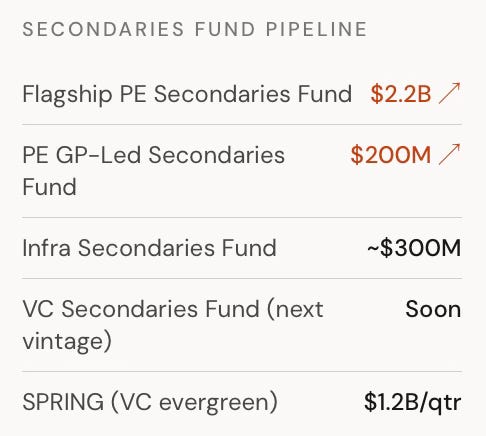

A wave of secondaries capital approaching activation

StepStone closed its flagship PE secondaries fund at $2.2 billion in initial commitments and its GP-led PE secondaries fund at $200 million in a first close. Together, these two vehicles account for $2.5 billion of the firm’s record $40 billion in undeployed fee-earning capital — and both are expected to activate within the next two quarters.

That activation matters beyond StepStone’s own income statement. When large secondaries funds of this scale move from fundraising into deployment mode, they become active buyers in the market, shaping pricing, deal flow, and the competitive dynamics for other secondaries managers. The infrastructure secondaries fund also saw approximately $300 million of additional closes, with retroactive fees already recognized this quarter.

On the venture side, StepStone’s SPRING fund — a semi-liquid evergreen vehicle giving individual investors access to late-stage venture secondaries — generated $1.2 billion in subscriptions in Q4, making March and April its two best months ever. CEO Scott Hart confirmed that May was tracking similarly.

The VC secondaries thesis: concentration and the AI tailwind

StepStone’s venture secondaries franchise is arguably the most strategically distinctive part of its secondaries business.

Head of Strategy Michael McCabe outlined a thesis built around the power law dynamics of venture capital: the top 100 venture-backed companies have driven close to 50% of total value creation over the past decade. StepStone’s response is to build deliberately concentrated secondaries portfolios targeting those assets — sourcing through LP-leds, GP-leds, and direct secondaries relationships with management teams and lead investors alike.

The portfolio composition reflects this approach. In the SPRING fund, the top 50 positions represent approximately 75% of total fund value. Of those 50 companies, roughly 75% carry direct AI exposure — spanning AI-native businesses, defense technology, space, cybersecurity, and fintech. For European LPs evaluating whether to allocate to US venture secondaries strategies, this concentration profile is both an opportunity and a risk to assess carefully.

The dedicated VC Secondaries Fund — StepStone’s institutional vehicle, which last raised over $3 billion — is returning to market “shortly,” according to the call. Its return will represent one of the larger VC secondaries fundraises in the market this year.

“We are looking to build reasonably concentrated portfolios in what we believe to be the best ideas and the biggest value drivers within the venture ecosystem.”

MIKE MCCABE, HEAD OF STRATEGY — STEPSTONE GROUP, Q4 FY2026 EARNINGS CALL

A fee structure change signals LP pricing power

Buried in the financial details was a disclosure worth noting for anyone tracking how secondaries fund terms are evolving. StepStone announced a prospective change to the fee structure of its flagship PE secondaries fund: lower management fees during the investment period, offset by higher fees after deployment is complete. The firm described this as aligning with “recent market practices” and mitigating the J-curve for LPs.

The isolated impact, according to CFO David Park, would be a three-to-four basis point reduction in the firm-wide blended commingled fund fee rate when the fund is fully raised and activated — expected to be offset by continued growth in higher-fee private wealth products. The present value of total fees is structured to be equivalent to the old terms.

The change is a small but meaningful data point. It suggests that LP pressure on fee structures in PE secondaries has reached the point where even the largest and most established managers are making concessions on investment-period economics. Whether this becomes the new market norm is worth watching across the next vintage of funds from peer managers.

The exit environment: secondaries as pressure valve

StepStone’s $936 million in net accrued carry — up 7% in the quarter — sits largely in mature, harvest-ready programs. Approximately 60% is tied to funds older than five years. Yet gross realized performance fees of $46 million were below recent quarterly paces, reflecting the continued drag from depressed M&A and IPO markets.

Management was candid about what is needed for a recovery: full exits, not just continuation vehicles or partial realizations. Both of those structures — which have become increasingly prevalent as GPs manage liquidity in the absence of traditional exit routes — allow capital to stay locked up even as some value is returned. The industry came into 2026 cautiously optimistic, only to face a fresh set of disruptions: AI uncertainty, concerns around private credit, and geopolitical instability. Full exit volume has not yet returned to historic norms.

In that context, StepStone was explicit that secondaries will continue to serve as a primary liquidity mechanism for both GPs and LPs. The logic is straightforward: as long as the exit environment remains constrained and LPs are focused on distributions, the demand side for secondaries transactions does not abate. The question for secondaries managers in 2026 and beyond is less whether deal flow exists and more whether pricing discipline and portfolio construction can hold through a period of macro volatility.

A European story, not just a US one

StepStone’s results are often read through a US lens — and understandably so, given that its private wealth platform and its venture secondaries franchise are predominantly American in character. But the firm’s European presence is substantial enough that its strategic priorities carry direct implications for the continent’s secondaries market.

StepStone has operated in Europe since 2005, and today runs seven offices across the continent — including London, Dublin, Rome, and Milan, which opened in 2025. Its EU-regulated subsidiary, StepStone Group Europe Alternative Investment Limited (SGEAIL), is authorized by the Central Bank of Ireland and manages €29.1 billion in AUM on behalf of European institutional clients, up from €20.6 billion in December 2022. The Dublin office alone employs 110 people — roughly 10% of the firm’s global workforce — and has doubled its headcount since 2021.

That footprint matters in the context of the secondaries pipeline described on the earnings call. When StepStone activates its flagship PE secondaries fund and its GP-led secondaries vehicle over the coming two quarters, SGEAIL will be among the entities through which European pension funds, insurance companies, and family offices gain exposure to those programs. European LPs are not just passive observers of this fundraising cycle — they are a core part of the capital base being assembled.

The Milan expansion is also a signal worth noting. Italy has become an increasingly active market for private markets distribution, particularly among private banks and family offices, and StepStone’s decision to establish a second Italian office alongside its Rome presence reflects a deliberate effort to deepen local relationships ahead of what the firm clearly expects to be sustained demand growth. Head of Europe David Jeffrey described it as part of a broader strategy of strengthening presence in Europe’s key financial hubs.

For European secondaries managers and LPs, the trajectory is legible: the largest global platforms are building permanent, regulated infrastructure on the continent, not simply parachuting in for fundraising cycles. The competitive and co-investment landscape in European secondaries will increasingly be shaped by firms operating at this scale.

StepStone’s results suggest the largest global platforms are navigating a difficult macro environment with notable confidence — and are actively expanding the European infrastructure to sustain that growth. The secondaries pipeline it is bringing to market — across PE, GP-led, infrastructure, and venture — represents one of the broadest and most capitalized programs globally. For European managers and LPs, the message is clear: the global secondaries market is entering a deployment cycle, and its gravitational pull will be felt on this side of the Atlantic.

| A guest post by

|